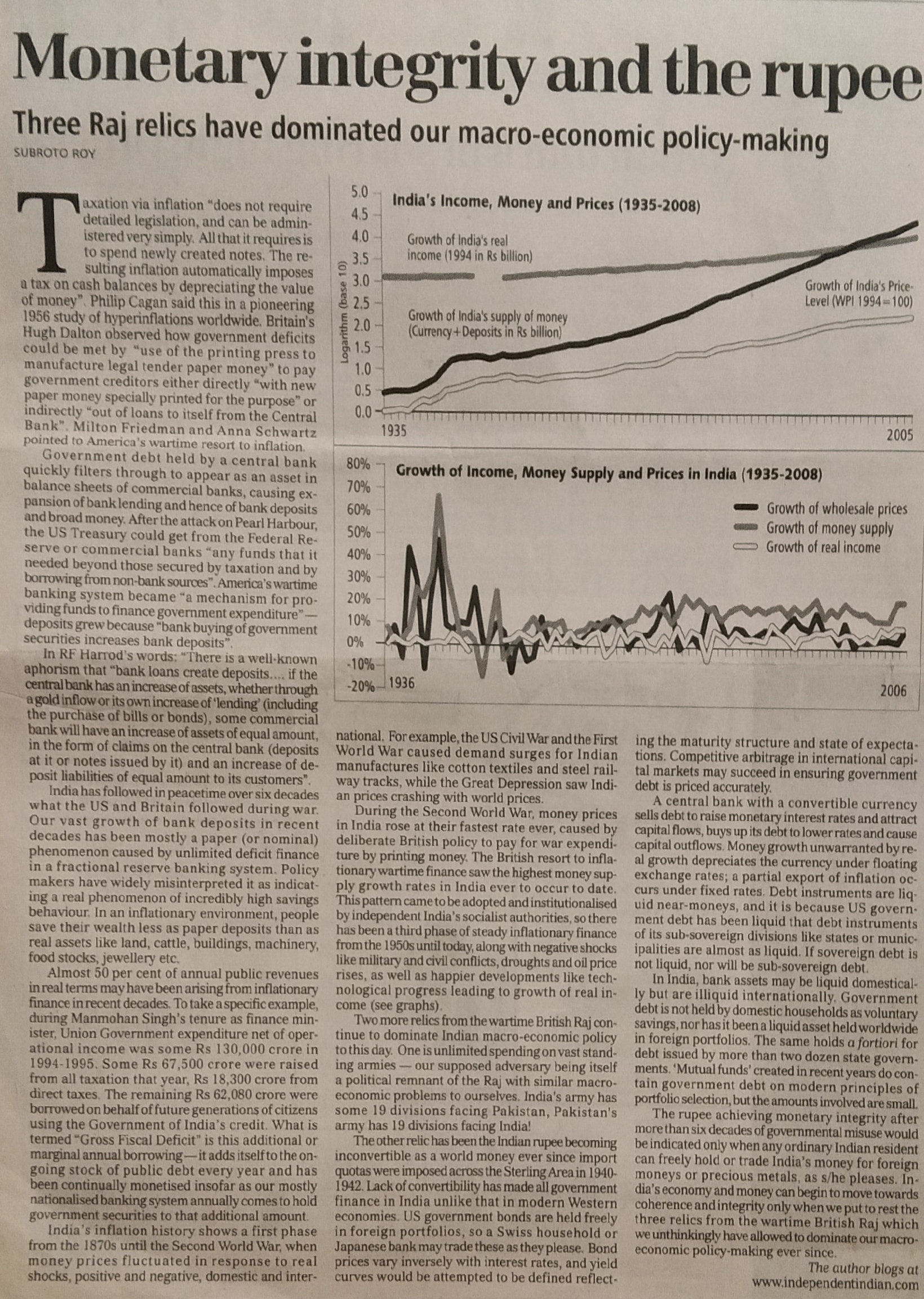

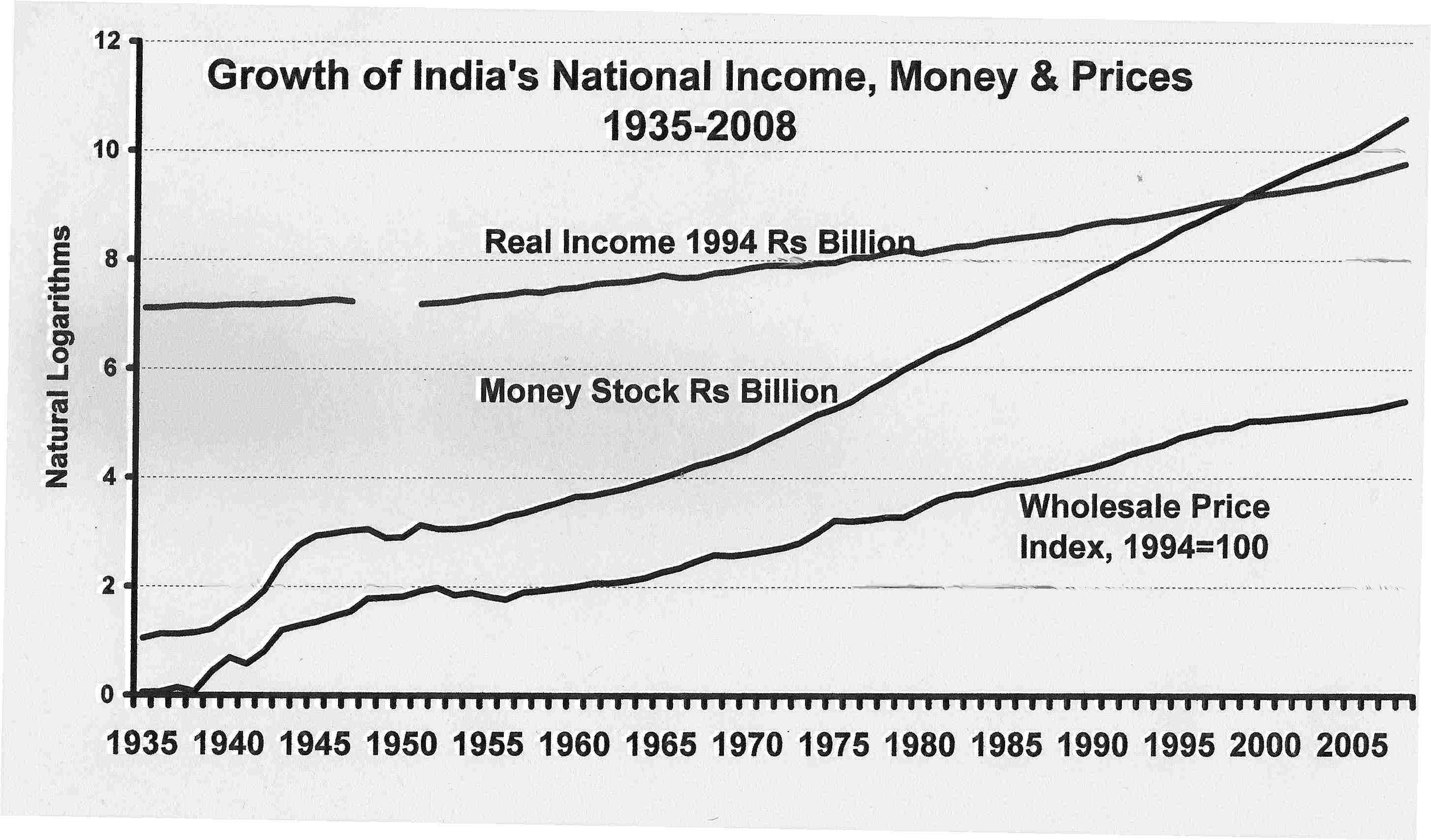

BENGAL’S FINANCES

First published in The Sunday Statesman February 25 2007, Editorial Page Special Article, www.thestatesman.net

There is urgent need for calm, sober thought, not self-delusion. Foreign trade, world politics are not what State Governments are constitutionally permitted to do.

By SUBROTO ROY

Mr Buddhadeb Bhattacharjee is fond of saying his hoped for industrialization plans will lead to jobs for “thousands” of unemployed young men and women emerging from West Bengal’s many schools, colleges and universities.

Now ever since JM Keynes’s time, economists have understood the phenomenon of unemployment quite well. Some unemployment is voluntary: where someone declines to accept a job at the prevailing wage or chooses leisure instead, e.g. withdraws from the labour-force in order to go to college or care for children or family or be involved in search for a better job. Some unemployment is seasonal, as in agriculture ~ where there often is “overfull” employment at harvest-time. Some unemployment may be frictional or structural, depending on dynamic unpredictable industrial or technological changes. In none of these cases is any large role defined for government investment using public resources, though there can be smaller roles like providing job-information, advice and training.

Keynes himself was concerned with systematic “involuntary” unemployment, where masses of people are willing but unable to find work at the going wage because there has been a general collapse of the market economy, as arguably happened in the 1930s in the Western countries. There has been no such situation in independent India.

And it is important to remember our labour markets are mostly unrestricted by State boundaries: unlike totalitarian China, we do not have internal passports in the country, and Indians are mostly free to work anywhere they wish to. Talk from CPI-M, Congress, BJP or other politicians of alleged Keynesian “multiplier” effects arising from government expenditure is mostly talk. And as for Sonia Gandhi’s “National Rural Employment Guarantee”, to the extent it was argued for at all by Amartya Sen’s disciples like Jean Drèze, the argument was not on Keynesian grounds but of a purportedly more equitable distribution of government expenditure.

What then is the Bhattacharjee Government supposed to be doing?

Chandrababu Naidu started a trend among Chief Ministers flying off to exotic foreign vistas, addressing international conferences and signing memoranda with foreign businessmen. But world politics, international relations and foreign trade are not what Indian State Governments are permitted by our Constitution to be engaged in doing. Nelson Mandela is a great man of history but Jyoti Basu’s Government had no constitutional right or business to gift him five million American dollars of West Bengal public money after he was released from jail in South Africa in 1990 by De Klerk.

Our Constitution is crystal clear that the legitimate agenda of India’s State Governments is something very mundane and wholly unglamorous: State Governments are supposed to be managing Courts of Law; the Police, Civil Order, Prisons; Water, Sanitation, Health; State Debt Service; Intra-State Infrastructure & Communications; Local Government; Liquor & Other Public Sector Industry; Trade, Local Banking & Finance; Land, Agriculture, Animal Husbandry; Libraries, Museums, Monuments; State Civil Service & Administration. In addition, “concurrent” with the Union Government are Criminal, Civil & Family Law, Contracts & Torts; Forests & Environmental Protection; Unemployment & Refugee Relief; Electricity; Education. It is relative to that explicit agenda that State Government performances around the country must be evaluated.

The finances of the West Bengal Government and those of every other State of the Union appear in a condition of Byzantine confusion. Even so, it is not impossible for any citizen to understand them with a little serious effort. The State receives tax revenues, income from State operations (like bus fares, lottery tickets etc), and grants transferred from the Union. Of the State’s total revenues, more than 80% arise from taxation. Of those taxes, about 30% is collected by the Union on behalf of the State in accordance with the Finance Commission’s formulae; 70% is collected by the State itself, and about 60% of whhat the State collects is Sales Tax. On the expenditure side, more than 60% goes in repaying the State’s debts as well as interest owed on that debt. The remainder gets distributed as summarily shown in the table. (What would be revealed at a higher level of detail is that e.g. Rs. 2.63 Bn is spent in collecting Rs. 9.93 Bn of land revenue!) The wide difference between the State’s income from all sources and its expenditures implies the State must then issue new public debt. That typically has been a larger and larger sum every year, greater than the amount of maturing debt being amortised or extinguished. The potentially grave consequence of this will be obvious to any householder, and makes it imperative that calm, sober thought and objective analysis occur about the State’s financial condition and budget constraint. There is no room for self-delusion, especially on the part of the Bhattacharjee Government. We are still paying interest on the money we borrowed to make Nelson Mandela a gift seventeen years ago.

Govt. of W. Bengal’s Finances 2003-2004

Rs Billion (Hundred Crore)

EXPENDITURE ACTIVITIES:

government & local government 8.68 1.68%

judiciary 1.27 0.25%

police (including home guard etc.) 13.47 2.61%

prisons 0.62 0.12%

bureaucracy 5.69 1.10%

collecting land revenue & taxes 4.32 0.84%

government employee pensions 26.11 5.05%

schools, colleges, universities, institutes 45.06 8.72%

health, nutrition & family welfare 14.70 2.84%

water supply & sanitation 3.53 0.68%

roads, bridges, transport, etc. 8.29 1.60%

electricity (mostly loans to power sector) 31.18 6.03%

irrigation, flood control, environment, ecology 10.78 2.09%

agricultural subsidies, rural development, etc. 7.97 1.54%

industrial subsidies 2.56 0.50%

capital city development 7.29 1.41%

social security, SC, ST, OBC, labour welfare 9.87 1.91%

tourism 0.09 0.02%

arts, archaeology, libraries, museums 0.16 0.03%

miscellaneous 0.52 0.10%

debt amortization & debt servicing 314.77 60.89%

total expenditure 516.92

tax revenue 141.10

operational income 6.06

grants from Union 18.93

loans recovered 0.91

total income 167.00

INCOME SOURCES:

GOVT. BORROWING REQUIREMENT

(total expenditure

minus total income ) 349.93

financed by:

new public debt issued 339.48

use of Trust Funds etc 10.45

349.93

From the author’s research and based on latest available data published by the Comptroller & Auditor General of India

")