January 31, 2013 — drsubrotoroy

1. “What was relatively weak at LSE was general economic theory. We were good at deriving the Best Linear Unbiased Estimator but left unsatisfied with our grasp of the theory of value that constituted the roots of our discipline. I managed a First and was admitted to Cambridge as a Research Student in 1976, where fortune had Frank Hahn choose me as a student. That at the outset was protection from the communist cabal that ran “development economics” with whom almost all the Indians ended up. I was wholly impecunious in my first year as a Research Student, and had to, for example, proof-read Arrow and Hahn’s General Competitive Analysis for its second edition to receive 50 pounds sterling from Hahn which kept me going for a short time. My exposure to Hahn’s subtle, refined and depthless thought as an economist of the first rank led to fascination and wonderment, and I read and re-read his “On the notion of equilibrium in economics”, “On the foundations of monetary theory”, “Keynesian economics and general equilibrium theory” and other clear-headed attempts to integrate the theory of value with the theory of money — a project Wicksell and Marshall had (perhaps wisely) not attempted and Keynes, Hicks and Patinkin had failed at.

Hahn insisted a central question was to ask how money, which is intrinsically worthless, can have any value, why anyone should want to hold it. The practical relevance of this question is manifest. India today in 2007 has an inconvertible currency, vast and growing public debt financed by money-creation, and more than two dozen fiscally irresponsible State governments without money-creating powers. While pondering, over the last decade, whether India’s governance could be made more responsible if States were given money-creating powers, I have constantly had Hahn’s seemingly abstruse question from decades ago in mind, as to why anyone will want to hold State currencies in India, as to whether the equilibrium price of those monies would be positive. (Lerner in fact gave an answer in 1945 when he suggested that any money would have value if its issuer agreed to collect liabilities in it — as a State collects taxes – and that may be the simplest road that bridges the real/monetary divide.)

Though we were never personal friends and I did not ingratiate myself with Hahn as did many others, my respect for him only grew when I saw how he had protected my inchoate classical liberal arguments for India from the most vicious attacks that they were open to from the communists. My doctoral thesis, initially titled “A monetary theory for India”, had to be altered due to paucity of monetary data at the time, as well as the fact India’s problems of political economy and allocation of real resources were more pressing, and so the thesis became “On liberty and economic growth: preface to a philosophy for India”. When no internal examiner could be found, the University of Cambridge, at Hahn’s insistence, showed its greatness by appointing two externals: C. J. Bliss at Oxford and T. W. Hutchison at Birmingham, former students of Hahn and Joan Robinson respectively. My thesis received the most rigorous and fairest imaginable evaluation from them…”

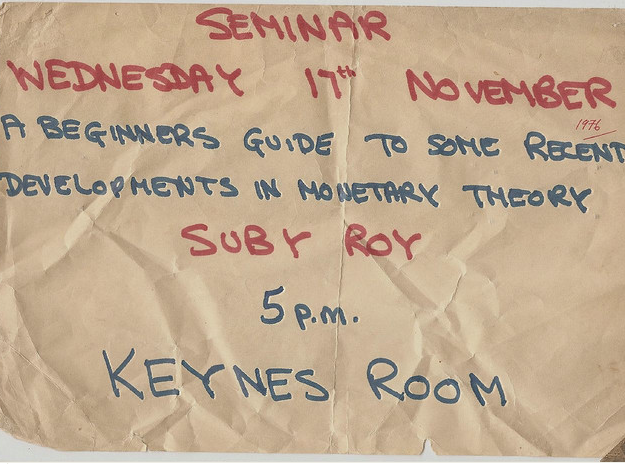

I was petrified but somehow managed to give a half-decent lecture before a standing-room only audience in what used to be called the “Keynes Room” in the Cambridge Economics Department. (It helped that a few months earlier, as a final year undergraduate at the LSE, I had been required to give a lecture at ACL Day’s Seminar on international monetary economics. It is a practice I came to follow with my students in due course, as there may be no substitute in learning how to think while standing up.) I shall try to publish exactly what I said at my Hahn-seminar when I find the document; broadly, it had to do with the crucial problem Hahn had identified a dozen years earlier in Patinkin’s work by asking what was required for the price of money to be positive in a general equilibrium, i.e. why do people everywhere hold and use money when it is intrinsically worthless. Patinkin’s utility function had real money balances appearing along with other goods; Hahn’s “On Some Problems of Proving the Existence of an Equilibrium in a Monetary Economy” in Theory of Interest Rates (1965), was the decisive criticism of this, where he showed that Patinkin’s formulation could not ensure a non-zero price for money in equilibrium. Hence Patinkin’s was a model in which money might not be held and therefore failed a vital requirement of a monetary economy. The announcement of my seminar was scribbled by a young Cambridge lecturer named Oliver Hart, later a distinguished member of MIT and Harvard University.”

3. Then there was Sraffa…I saw him many a time, in the Marshall Library… He would smile very broadly at me and without saying anything indicate with his hand to invite me to his office.. I fled in some fear… It was very stupid of me of course… Joan Robinson cornered me once and took me into the office she shared with EAG… She came at me for an hour or so wishing to supervise me, I kept declining politely… saying I was with Frank Hahn and wished to work on money… “What does Frankie know about India?” she said… I said I did not know but he did know about monetary theory and that was what I needed for India; I also said I did not think much about the Indian Marxists she had supervised… and mentioned a prominent name… she said about him, “Yes most of what he does can go straight into the dustbin”…

4. “I had been attracted to Cambridge partly by its old reputation for philosophy, especially that of Wittgenstein. But I met no worthwhile philosophers there until a few months before I was to leave for the United States in 1980, when I chanced upon the work of Renford Bambrough. Hahn had challenged me with the question, “how are you so sure your value judgements promoting liberty blah-blah are better than those of Chenery and the development economists?” It was a question that led inevitably to ethics and its epistemology — when I chanced upon Bambrough’s work, and that of his philosophical master, John Wisdom, the immense expanse of metaphysics (or ontology) opened up as well. “Then felt I like some watcher of the skies, When a new planet swims into his ken; Or like stout Cortez when with eagle eyes, He star’d at the Pacific…””

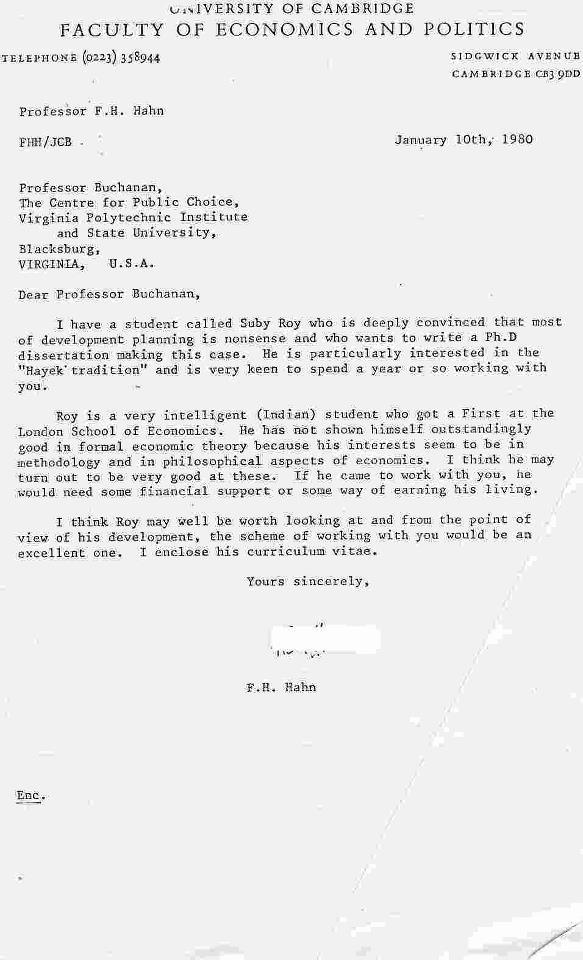

5. “I went to Virginia because James M. Buchanan was there, and he, along with FA Hayek, were whom Hahn decided to write on my behalf. Hayek said he was too old to accept me but wrote me kind and generous letters praising and hence encouraging my inchoate liberal thoughts and arguments. Buchanan was welcoming and I learnt much from him and his colleagues about the realities of public finance and democratic politics, which I quickly applied in my work on India…” Hahn told me he did not know Buchanan but he did know Hayek well and that his wife Dorothy had been an original member of the Mont Pelerin Society in 1947 or 1948. Hence I am amused reading a prominent NYU “American Austrian” say about Frank’s passing “I do think economics would have been better off if the Arrow-Debreu-Hahn approach had not been taken so seriously by the profession. I think it turned out to be an intellectual straight-jacket that prevented the discussion of valuable outside-the-box ideas”, and am tempted to paraphrase the closing lines of Tractatus — “Whereof one cannot speak, thereof one must be silent/About what one can not speak, one must remain silent” — to read “Of that of which we are ignorant, we should at least try not to gas about…” Hahn and Hayek were friends, from when Hayek taught at the London School of Economics in Robbins’ seminar, and Hahn was Robbins’ doctoral student.

7. “I have a student called Suby Roy…” Frank sends me to America in 1980 to work with Jim Buchanan… One letter from him was all it took…

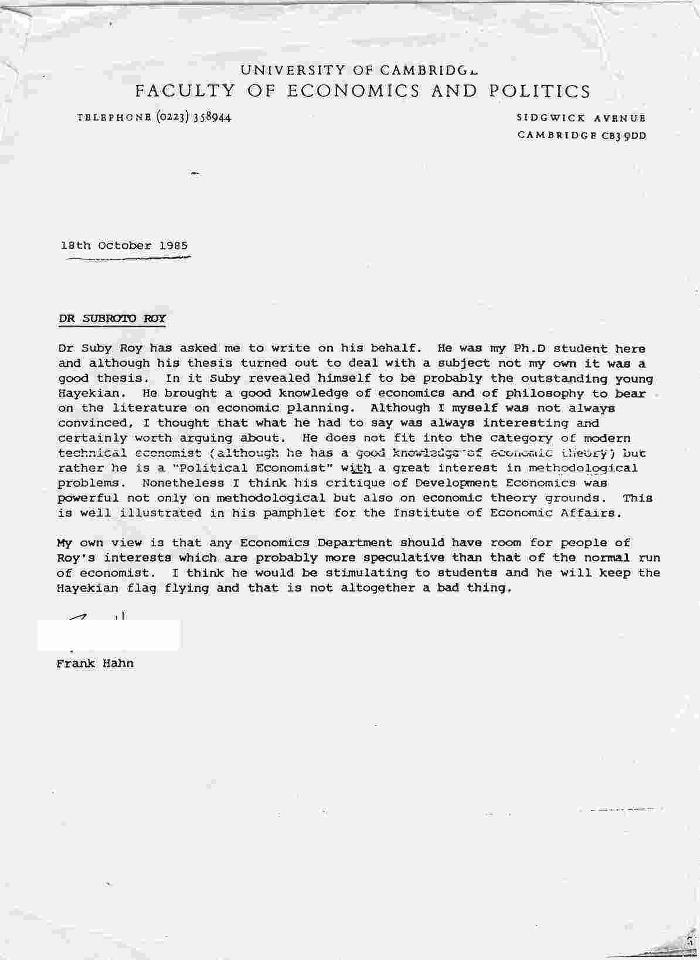

And then five years later in 1985 he calls me “probably the outstanding young Hayekian”, says I had brought “a good knowledge of economics and of philosophy to bear on the literature on economic planning”, had “a good knowledge of economic theory” and that my “critique of Development Economics was powerful not only on methodological but also on economic theory grounds” — all that to me has been a special source of delight.

We did not meet often after I left Cambridge but he wrote very kindly always, and finally said, hearing of my travails and troubles and adventures, “well you are having an interesting life…”…

In America, I once met Robert M Solow in a hotel elevator as we were on a panel at a conference together; I introduced myself as Hahn’s student… “Aren’t you lucky?” said Solow with a smile…and he was right… I was lucky…

I said of Milton Friedman that he had been “the greatest economist after John Maynard Keynes”; Milton’s critic, Frank Hahn, may have been the greatest economic theorist of modern times.

Frank Hahn (1925-2013)

December 11, 2009 — drsubrotoroy

“On the blissful innocence of the RBI” (2009) From Facebook:

Subroto Roy can only sigh at the fact that while he has had to struggle for 35 years trying to grasp and then apply serious monetary economics to India’s circumstances, the RBI Governor & his four Deputy Governors appear blissfully innocent of all Hicks, Tobin, Friedman, Cagan et al yet exude confidence enough to “Waffle Away!”

A Small Challenge to the RBI’s Governor Subbarao

April 21, 2010

The Hon’ble Gov of the Reserve Bank of India Shri D Subbarao

Dear Governor Subbarao,

You said yesterday, April 20 2010, that the Reserve Bank of India has a macroeconomic model which it uses but which you had personally not seen.

I have given two lectures at your august offices, one by invitation of Governor Jalan and Deputy Governor Reddy on April 29, 2000 to address the Conference of State Finance Secretaries, the other on May 5, 2005 to address the Chief Economist’s Monetary Economics Seminar. On both occasions, I had inquired of the RBI’s own models by which I could contrast my own but came to understand there were none.

If since then the RBI has now constructed a macroeconomic model of India’s economy, it is splendid news.

May I request the model be released publicly on the Internet at once, so its specifications of endogenous and exogenous variables, assumed coefficients, and sources of time-series data all may be seen by everyone in the country and abroad? Scientific scrutiny and replication of results would thus come to be permitted.

I would be especially interested to know the demand for money function that you have used. I well remember my meeting with the late great Sukhamoy Chakravarty on July 14 1987 at his Planning Commission offices, when he signed and gifted me his last personal copy of the famous Reserve Bank report by the committee he had chaired and of which he told me personally Dr Rangarajan had been the key author – that report may have contained the first official discussion of the demand for money function in India.

With cordial regards

Subroto Roy

October 11, 2009 — drsubrotoroy

From Facebook:

Subroto Roy announces that if he was awarding the 2009 “Economics Nobel” it would go to Frank Horace Hahn and Anna Jacobson Schwartz: each for a lifetime of contributions to economic theory and monetary economics specifically relevant to the macroeconomic crises of recent years….Hahn’s Non-Walrasian theory provides a logic to what has happened; Schwartz predicted it and has diagnosed it better than anyone else.

Certainly the appalling state of academic economics is manifest in the self-written self-serving Wikipedia entries of the many Elmer & Mrs Fudd Professors of Gobbledygook at Ivy U…. all in the hope of getting noticed by the bookies in England quoting odds… and thereby considering themselves Nobel hopefuls…. (“has been mentioned as a possible winner…”)…

June 12, 2009 — drsubrotoroy

12 June 2009

The Hon’ble Dr Manmohan Singh, MP, Rajya Sabha

Prime Minister of India

Respected Pradhan Mantriji:

I may add my father, back in 1973 in Paris, had predicted to me that you would become Prime Minister of India one day, and he, now in his 90s, is joined by myself in sending our warm congratulations at the start of your second term in that high office.

The controversy though that you and I had entered that Paris day in 1973 about scientific economics as applied to India, must be renewed afresh!

This is because of your categorical statement on June 9 2009 to the new 15th Lok Sabha:

“I am convinced, since our savings rate is as high as 35%, given the collective will, if all of us work together, we can achieve a growth-rate of 8%-9%, even if the world economy does not do well.” (Statement of Dr Manmohan Singh to the Lok Sabha, June 9 2009)

I am afraid there may be multiple reasons why such a statement is gravely and incorrigibly in error within scientific economics. From your high office as Prime Minister in a second term, faced perhaps with no significant opposition from either within or without your party, it is possible the effects of such an error may spell macroeconomic catastrophe for India.

“now has 10.4% growth on a 44 % savings rate… ”

Indeed the idea that China and India have had extremely high economic growth-rates based on purportedly astronomical savings rates has become a commonplace in recent years, repeated endlessly in international and domestic policy circles though perhaps without adequate basis.

1. Germany & Japan

What, at the outset, is supposed to be measured when we speak of “growth”? Indian businessmen and their media friends seem to think “growth” refers to something like nominal earnings before tax for the organised corporate sector, or any unspecified number that can be sold to visiting foreigners to induce them to park their funds in India: “You will get a 10% return if you invest in India” to which the visitor says “Oh that must mean India has 10% growth going on”. Of such nonsense are expensive international conferences in Davos and Delhi often made.

You will doubtless agree the economist at least must define economic growth properly and with care — what is referred to must be annual growth of per capita inflation-adjusted Gross Domestic Product. (Per capita National Income or Net National Product would be even better if available).

West Germany and Japan had the highest annual per capita real GDP growth-rates in the world economy starting from devastated post-World War II initial conditions. What were their measured rates?

West Germany: 6.6% in 1950-1960, falling to 3.5% by 1960-1970 falling to 2.4% by 1970-1978.

Japan: 6.8 % in 1952-1960 rising to 9.4% in 1960-1970 falling to 3.8 % in 1970-1978.

Thus in recent decadesonly Japan measured a spike in the 1960s of more than 9% annual growth of real per capita GDP. Now India and China are said to be achieving 8%-10 % and more year after year routinely!

Perhaps we are observing an incredible phenomenon of world economic history. Or perhaps it is just something incredible, something false and misleading, like a mirage in the desert.

You may agree that processes of measurement of real income in India both at federal and provincial levels, still remain well short of the world standards described by the UN’s System of National Accounts 1993. The actuality of our real GDP growth may be better than what is being measured or it may be worse than what is being measured – from the point of view of public decision-making we at present simply do not know which it is, and to overly rely on such numbers in national decisions may be unwise. In any event, India’s population is growing at near 2% so even if your Government’s measured number of 8% or 9% is taken at face-value, we have to subtract 2% population growth to get per capita figures.

2. Growth of the aam admi’s consumption-basket

The late Professor Milton Friedman had been an invited adviser in 1955 to the Government of India during the Second Five Year Plan’s formulation. The Government of India suppressed what he had to say and I had to publish it 34 years later in May 1989 during the 1986-1992 perestroika-for-India project that I led at the University of Hawaii in the United States. His November 1955 Memorandum to the Government of India is a chapter in the book Foundations of India’s Political Economy: Towards an Agenda for the 1990s that I and WE James created.

“I don’t believe the term GNP ought to be used unless it is supplemented by a different statistic: the rate of growth of the average consumption basket consumed by the ordinary individual in the country. I think GNP rates of growth can give very misleading information. For example, you have rapid rates of growth of GNP in the Soviet Union with a declining standard of life for the people. Because GNP includes monuments and includes also other things. I’m not saying that that is the case with India; I’m just saying I would like to see the two figures together.”

You may perhaps agree upon reflection that not only may our national income growth measurements be less robust than we want, it may be better to be measuring something else instead, or as well, as a measure of the economic welfare of India’s people, namely, “the rate of growth of the average consumption basket consumed by the ordinary individual in the country”, i.e., the rate of growth of the average consumption basket consumed by the aam admi.

It would be excellent indeed if you were to instruct your Government’s economists and other spokesmen to do so this as it may be something more reliable as an indicator of our economic realities than all the waffle generated by crude aggregate growth-rates.

3. Logic of your model

Thirdly, the logic needs to be spelled out of the economic model that underlies such statements as yours or Meghnad Desai’s that seek to operationally relate savings rates to aggregate growth rates in India or China. This seems not to have been done publicly in living memory by the Planning Commission or other Government economists. I have had to refer, therefore, to pages 251-253 of my own Cambridge doctoral thesis under Professor Frank Hahn thirty years ago, titled “On liberty and economic growth: preface to a philosophy for India”, where the logic of such models as yours was spelled out briefly as follows:

Let

Kt be capital stock

Yt be national output

It be the level of real investment

St be the level of real savings

By definition

It = K t+1 – Kt

By assumption

Kt = k Yt 0 < k < 1

St = sYt 0 < s <1

In equilibrium ex ante investment equals ex ante savings

It = St

Hence in equilibrium

sYt = K t+1 – Kt

Or

s/k = g

where g is defined to be the rate of growth (Y t+1-Yt)/Yt .

The left hand side then defines the “warranted rate of growth” which must maintain the famous “knife-edge” with the right hand side “natural rate of growth”.

Your June 9 2009 Lok Sabha statement that a 35% rate of savings in India may lead to an 8%-9% rate of economic growth in India, or Meghnad Desai’s statement that a 44% rate of savings in China led to a 10.4% growth there, can only be made meaningful in the context of a logical economic model like the one I have given above.

[In the open-economy version of the model, let Mt be imports, Et be exports, Ft net capital inflows.

Assume

Mt = aIt + bYt 0 < a, b < 1

Et = E for all t

Balance of payments is

Bt = Mt – Et – Ft

In equilibrium It = St + Bt

Or

Ft = (s+b) Yt – (1-a) It – E is a kind of “warranted” level of net capital inflow.]

You may perhaps agree upon reflection that building the entire macroeconomic policy of the Government of India merely upon a piece of economic logic as simplistic as the

s/k = g

equation above, may spell an unacceptable risk to the future economic well-being of our vast population. An alternative procedural direction for macroeconomic policy, with more obviously positive and profound consequences, may have been that which I sought to persuade Rajiv Gandhi about with some success in 1990-1991. Namely, to systematically seek to improve towards normalcy the budgets, financial positions and decision-making capacities of the Union and all state and local governments as well as all public institutions, organisations, entities, and projects in general, with the aim of making our domestic money a genuine hard currency of the world again after seven decades, so that any ordinary resident of India may hold and trade precious metals and foreign exchange at his/her local bank just like all those glamorous privileged NRIs have been permitted to do. Such an alternative path has been described in “The Indian Revolution”, “Against Quackery”, “The Dream Team: A Critique”, “India’s Macroeconomics”, “Indian Inflation”, etc.

4. Gross exaggeration of real savings rate by misreading deposit multiplication

Specifically, I am afraid you may have been misled into thinking India’s real savings rate, s, is as high as 35% just as Meghnad Desai may have misled himself into thinking China’s real savings rate is as high as 44%.

Neither of you may have wanted to make such a claim if you had referred to the fact that over the last 25 years, the average savings rate across all OECD countries has been less than 10%. Economic theory always finds claims of discontinuous behaviour to be questionable. If the average OECD citizen has been trying to save 10% of disposable income at best, it appears prima facie odd that India’s PM claims a savings rate as high as 35% for India or a British politician has claimed a savings rate as high as 44% for China. Something may be wrong in the measurement of the allegedly astronomical savings rates of India and China. The late Professor Nicholas Kaldor himself, after all, suggested it was rich people who saved and poor people who did not for the simple reason the former had something left over to save which the latter did not!

And indeed something is wrong in the measurements. What has happened, I believe, is that there has been a misreading of the vast nominal expansion of bank deposits via deposit-multiplication in the Indian banking system, an expansion that has been caused by explosive deficit finance over the last four or five decades. That vast nominal expansion of bank-deposits has been misread as indicating growth of real savings behaviour instead. I have written and spoken about and shown this quite extensively in the last half dozen years since I first discovered it in the case of India. E.g., in a lecture titled “Can India become an economic superpower or will there be a monetary meltdown?” at Cardiff University’s Institute of Applied Macroeconomics and at London’s Institute of Economic Affairs in April 2005, as well as in May 2005 at a monetary economics seminar invited at the RBI by Dr Narendra Jadav. The same may be true of China though I have looked at it much less.

“Savings is indeed normally measured by adding financial and non-financial savings. Financial savings include bank-deposits. But India is not a normal country in this. Nor is China. Both have seen massive exponential growth of bank-deposits in the last few decades. Does this mean Indians and Chinese are saving phenomenally high fractions of their incomes by assiduously putting money away into their shaky nationalized banks? Sadly, it does not. What has happened is government deficit-financing has grown explosively in both countries over decades. In a “fractional reserve” banking system (i.e. a system where your bank does not keep the money you deposited there but lends out almost all of it immediately), government expenditure causes bank-lending, and bank-lending causes bank-deposits to expand. Yes there has been massive expansion of bank-deposits in India but it is a nominal paper phenomenon and does not signify superhuman savings behaviour. Indians keep their assets mostly in metals, land, property, cattle, etc., and as cash, not as bank deposits.”

“India has followed in peacetime over six decades what the US and Britain followed during war. Our vast growth of bank deposits in recent decades has been mostly a paper (or nominal) phenomenon caused by unlimited deficit finance in a fractional reserve banking system. Policy makers have widely misinterpreted it as indicating a real phenomenon of incredibly high savings behaviour. In an inflationary environment, people save their wealth less as paper deposits than as real assets like land, cattle, buildings, machinery, food stocks, jewellery etc.”

If you asked me “What then is India’s real savings rate?” I have little answer to give except to say I know what it is not – it is not what the Government of India says it is. It is certainly unlikely to be anywhere near the 35% you stated it to be in your June 9 2009 Lok Sabha statement. If the OECD’s real savings rate has been something like 10% out of disposable income, I might accept India’s is, say, 15% at a maximum when properly measured – far from the 35% being claimed. What I believe may have been mismeasured by you and Meghnad Desai and many others as indicating high real savings is actually the nominal or paper expansion of bank-deposits in a fractional reserve banking system induced by runaway government deficit-spending in both India and China over the last several decades.

5. Technological progress and the mainsprings of real economic growth

So much for the g and s variables in the s/k = g equation in your economic model. But the assumed constant k is a big problem too!

During the 1989 perestroika-for-India project-conference, Professor Friedman referred to his 1955 experience in India and said this about the assumption of a constant k:

“I think there was an enormously important point… That was the almost universal acceptance at that time of the view that there was a sort of technologically fixed capital output ratio. That if you wanted to develop, you just had to figure out how much capital you needed, used as a statistical technological capital output ratio, and by God the next day you could immediately tell what output you were going to achieve. That was a large part of the motivation behind some of the measures that were taken then.”

The crucial problem of the sort of growth-model from which your formulation relating savings to growth arises is that, with a constant k, you have necessarily neglected the real source of economic growth, which is technological progress!

I said in the 2007 article referred to above:

“Economic growth in India as elsewhere arises not because of what politicians and bureaucrats do in capital cities, but because of spontaneous technological progress, improved productivity and learning-by-doing on part of the general population. Technological progress is a very general notion, and applies to any and every production activity or commercial transaction that now can be accomplished more easily or using fewer inputs than before.”

“The mainsprings of real growth in the wealth of the individual, and so of the nation, are greater practical learning, increases in capital resources and improvements in technology. Deeper skills and improved dexterity cause output produced with fewer inputs than before, i.e. greater productivity. Adam Smith said there is “invention of a great number of machines which facilitate and abridge labour, and enable one man to do the work of many”. Consider a real life example. A fresh engineering graduate knows dynamometers are needed in testing and performance-certification of diesel engines. He strips open a meter, finds out how it works, asks engine manufacturers what design improvements they want to see, whether they will buy from him if he can make the improvement. He finds out prices and properties of machine tools needed and wages paid currently to skilled labour, calculates expected revenues and costs, and finally tries to persuade a bank of his production plans, promising to repay loans from his returns. Overcoming restrictions of religion or caste, the secular agent is spurred by expectation of future gains to approach various others with offers of contract, and so organize their efforts into one. If all his offers ~ to creditors, labour, suppliers ~ are accepted he is, for the moment, in business. He may not be for long ~ but if he succeeds his actions will have caused an improvement in design of dynamometers and a reduction in the cost of diesel engines, as well as an increase in the economy’s produced means of production (its capital stock) and in the value of contracts made. His creditors are more confident of his ability to repay, his buyers of his product quality, he himself knows more of his workers’ skills, etc. If these people enter a second and then a third and fourth set of contracts, the increase in mutual trust in coming to agreement will quickly decline in relation to the increased output of capital goods. The first source of increasing returns to scale in production, and hence the mainspring of real economic growth, arises from the successful completion of exchange. Transforming inputs into outputs necessarily takes time, and it is for that time the innovator or entrepreneur or “capitalist” or “adventurer” must persuade his creditors to trust him, whether bankers who have lent him capital or workers who have lent him labour. The essence of the enterprise (or “firm”) he tries to get underway consists of no more than the set of contracts he has entered into with the various others, his position being unique because he is the only one to know who all the others happen to be at the same time. In terms introduced by Professor Frank Hahn, the entrepreneur transforms himself from being “anonymous” to being “named” in the eyes of others, while also finding out qualities attaching to the names of those encountered in commerce. Profits earned are partly a measure of the entrepreneur’s success in this simultaneous process of discovery and advertisement. Another potential entrepreneur, fresh from engineering college, may soon pursue the pioneer’s success and start displacing his product in the market ~ eventually chasers become pioneers and then get chased themselves, and a process of dynamic competition would be underway. As it unfolds, anonymous and obscure graduates from engineering colleges become by dint of their efforts and a little luck, named and reputable firms and perhaps founders of industrial families. Multiply this simple story many times, with a few million different entrepreneurs and hundreds of thousands of different goods and services, and we shall be witnessing India’s actual Industrial Revolution, not the fake promise of it from self-seeking politicians and bureaucrats.”

Technological progress in a myriad of ways and discovery of new resources are important factors contributing to India’s growth today. But while India’s “real” economy does well, the “nominal” paper-money economy controlled by Government does not. Continuous deficit financing for half a century has led to exponential growth of public debt and broad money, and, as noted, the vast growth of nominal bank-deposits has been misinterpreted as indicating unusually high real savings behaviour when it in fact may just signal vast amounts of government debt being held by our nationalised banks. These bank assets may be liquid domestically but are illiquid internationally since our government debt is not held by domestic households as voluntary savings nor has it been a liquid asset held worldwide in foreign portfolios.

What politicians of all parties, especially your own and the BJP and CPI-M since they are the three largest, have been presiding over is exponential growth of our paper money supply, which has even reached 22% per annum. Parliament and the Government should be taking honest responsibility for this because it may certainly portend double-digit inflation (i.e., decline in the value of paper-money) perhaps as high as 14%-15% per annum, something that is certain to affect the aam admi’s economic welfare adversely.

6. Selling Government assets to Big Business is a bad idea in a potentially hyperinflationary economy

Respected PradhanMantriji, the record would show that I, and really I alone, 25 years ago, may have been the first among Indian economists to advocate the privatisation of the public sector. (Viz, “Silver Jubilee of Pricing, Planning and Politics: A Study of Economic Distortions in India”.) In spite of this, I have to say clearly now that in present circumstances of a potentially hyperinflationary economy created by your Government and its predecessors, I believe your Government’s present plans to sell Government assets may be an exceptionally unwise and imprudent idea. The reasoning is very simple from within monetary economics.

Government every year has produced paper rupees and bank deposits in practically unlimited amounts to pay for its practically unlimited deficit financing, and it has behaved thus over decades. Such has been the nature of the macroeconomic process that all Indian political parties have been part of, whether they are aware of it or not.

Indian Big Business has an acute sense of this long-term nominal/paper expansion of India’s economy, and acts towards converting wherever possible its own hoards of paper rupees and rupee-denominated assets into more valuable portfolios for itself of real or durable assets, most conspicuously including hard-currency denominated assets, farm-land and urban real-estate, and, now, the physical assets of the Indian public sector. Such a path of trying to transform local domestic paper assets – produced unlimitedly by Government monetary and fiscal policy and naturally destined to depreciate — into real durable assets, is a privately rational course of action to follow in an inflationary economy. It is not rocket-science to realise the long-term path of rupee-denominated assets is downwards in comparison to the hard-currencies of the world – just compare our money supply growth and inflation rates with those of the rest of the world.

The Statesman of November 16 2006 had a lead editorial titled Government’s land-fraud: Cheating peasants in a hyperinflation-prone economy which said:

“There is something fundamentally dishonourable about the way the Centre, the state of West Bengal and other state governments are treating the issue of expropriating peasants, farm-workers, petty shop-keepers etc of their small plots of land in the interests of promoters, industrialists and other businessmen. Singur may be but one example of a phenomenon being seen all over the country: Hyderabad, Karnataka, Kerala, Haryana, everywhere. So-called “Special Economic Zones” will merely exacerbate the problem many times over. India and its governments do not belong only to business and industrial lobbies, and what is good for private industrialists may or may not be good for India’s people as a whole. Economic development does not necessarily come to be defined by a few factories or high-rise housing complexes being built here or there on land that has been taken over by the Government, paying paper-money compensation to existing stakeholders, and then resold to promoters or industrialists backed by powerful political interest-groups on a promise that a few thousand new jobs will be created. One fundamental problem has to do with inadequate systems of land-description and definition, implementation and recording of property rights. An equally fundamental problem has to do with fair valuation of land owned by peasants etc. in terms of an inconvertible paper-money. Every serious economist knows that “land” is defined as that specific factor of production and real asset whose supply is fixed and does not increase in response to its price. Every serious economist also knows that paper-money is that nominal asset whose price can be made to catastrophically decline by a massive increase in its supply, i.e. by Government printing more of the paper it holds a monopoly to print. For Government to compensate people with paper-money it prints itself by valuing their land on the basis of an average of the price of the last few years, is for Government to cheat them of the fair present-value of the land. That present-value of land must be calculated in the way the present-value of any asset comes to be calculated, namely, by summing the likely discounted cash-flows of future values. And those future values should account for the likelihood of a massive future inflation causing decline in the value of paper-money in view of the fact we in India have a domestic public debt of some Rs. 30 trillion (Rs. 30 lakh crore) and counting, and money supply growth rates averaging 16-17% per annum. In fact, a responsible Government would, given the inconvertible nature of the rupee, have used foreign exchange or gold as the unit of account in calculating future-values of the land. India’s peasants are probably being cheated by their Government of real assets whose value is expected to rise, receiving nominal paper assets in compensation whose value is expected to fall.”

Shortly afterwards the Hon’ble MP for Kolkata Dakshin, Km Mamata Banerjee, started her protest fast, riveting the nation’s attention in the winter of 2006-2007. What goes for government buying land on behalf of its businessman friends also goes, mutatis mutandis, for the public sector’s real assets being bought up by the private sector using domestic paper money in a potentially hyperinflationary economy. If your new Government wishes to see real assets of the public sector being sold for paper money, let it seek to value these assets not in inconvertible rupees that Government itself has been producing in unlimited quantities but perhaps in forex or gold-units instead!

In the 2004-2005 volume Margaret Thatcher’s Revolution: How it Happened and What it Meant, edited by myself and Professor John Clarke, there is a chapter by Professor Patrick Minford on Margaret Thatcher’s fiscal and monetary policy (macroeconomics) that was placed ahead of the chapter by Professor Martin Ricketts on Margaret Thatcher’s privatisation (microeconomics). India’s fiscal and monetary or macroeconomic problems are far worse today than Britain’s were when Margaret Thatcher came to power. We need to get our macroeconomic problems sorted before we attempt the microeconomic privatisation of public assets.

It is wonderful that your young party colleague, the Hon’ble MP from Amethi, Shri Rahul Gandhi, has declined to join the present Government and instead wishes to reflect further on the “common man” and “common woman” about whom I had described his late father talking to me on September 18 1990. Certainly the aam admi is not someone to be found among India’s lobbyists of organised Big Business or organised Big Labour who have tended to control government agendas from the big cities.

With my warmest personal regards and respect, I remain,

Cordially yours

Subroto Roy, PhD (Cantab.), BScEcon (London)