May 11, 2011 — drsubrotoroy

Govt. of W. Bengal’s Finances 2003-2004

Rs Billion (Hundred Crore)

EXPENDITURE ACTIVITIES:

government & local government 8.68 1.68%

judiciary 1.27 0.25%

police (including home guard etc.) 13.47 2.61%

prisons 0.62 0.12%

bureaucracy 5.69 1.10%

collecting land revenue & taxes 4.32 0.84%

government employee pensions 26.11 5.05%

schools, colleges, universities, institutes 45.06 8.72%

health, nutrition & family welfare 14.70 2.84%

water supply & sanitation 3.53 0.68%

roads, bridges, transport, etc. 8.29 1.60%

electricity (mostly loans to power sector) 31.18 6.03%

irrigation, flood control, environment, ecology 10.78 2.09%

agricultural subsidies, rural development, etc. 7.97 1.54%

industrial subsidies 2.56 0.50%

capital city development 7.29 1.41%

social security, SC, ST, OBC, labour welfare 9.87 1.91%

tourism 0.09 0.02%

arts, archaeology, libraries, museums 0.16 0.03%

miscellaneous 0.52 0.10%

debt amortization & debt servicing 314.77 60.89%

total expenditure 516.92

INCOME SOURCES:

tax revenue 141.10

operational income 6.06

grants from Union 18.93

loans recovered 0.91

total income 167.00

GOVT. BORROWING REQUIREMENT

(total expenditure minus total income ) 349.93

financed by:

new public debt issued 339.48

use of Trust Funds etc 10.45

349.93

https://independentindian.com/2007/02/25/bengals-finances/

From the author’s research 2007 and based on latest available data published by the Comptroller & Auditor General of India

May 21, 2009 — drsubrotoroy

“May 21 2009 It is wonderful to hear from you and I am honoured to find myself, perhaps accidentally, on the same list as so many of your distinguished colleagues among Government economists.

Your essay is most engaging. I am afraid I disagree with your assessment that the current problems “did not originate in the real sector of the economy” but were “triggered by the excesses of the financial system”. I have said to the contrary “There is no clear path to solving the great (alleged) economic and financial crisis because no one wants to admit its roots were the overvaluation (over decades) of American real-estate, and hence American assets in general.”

There is no more real sector than real-estate itself and American real-estate has tended to be overvalued as a result of government policy since the Carter Administration; the accumulated dangers along that path came to explode in the sub-prime crisis. Here as elsewhere in economics, the financial tail has not wagged the non-financial dog but vice versa.

I have also said “(i) foreign central banks might have been left holding more bad US debt than might be remembered, and dollar depreciation and an American inflation seem to be inevitable over the next several years; (ii) all those bad mortgages and foreclosures could vanish within a year or two by playing the demographic card and inviting in a few million new immigrants into the United States; restoring a worldwide idea of an American dream fueled by mass immigration may be the surest way for the American economy to restore itself.”

Re the comparison with the Great Depression, I believe

“there are overriding differences. Most important, the American economy and the world economy are both incomparably larger today in the value of their capital stock, and there has also been enormous technological progress over eight decades. Accordingly, it would take a much vaster event than the present turbulence — say, something like an exchange of multiple nuclear warheads with Russia causing Manhattan and the City of London to be destroyed — before there was a return to something comparable to the 1929 Crash and the Great Depression that followed. Besides, the roots of the crises are different. What happened back then? In 1922, the Genoa Currency Conference wanted to correct the main defect of the pre-1914 gold standard, which was freezing the price of gold while failing to stabilise the purchasing power of money. From 1922 until about 1927, Benjamin Strong of the Federal Reserve Bank of New York adopted price-stabilisation as the new American policy-objective. Britain was off the gold standard and the USA remained on it. The USA, as a major creditor nation, saw massive gold inflows which, by traditional gold standard principles, would have caused a massive inflation. Governor Strong invented the process of “sterilisation” of those gold inflows instead and thwarted the rise in domestic dollar prices of goods and services. Strong’s death in 1928 threw the Federal Reserve System into conflict and intellectual confusion. Dollar stabilisation ended as a policy. Surplus bank money was created on the release of gold that had been previously sterilised. The traditional balance between bulls and bears in the stock-market was upset. Normally, every seller of stock is a bear and every buyer a bull. Now, amateur investors appeared as bulls attracted by the sudden stock price rises, while bears, who sold securities, failed to place their money into deposit and were instead lured into lending it as call money to brokerages who then fuelled these speculative bulls. As of October 22, 1929 about $4 billion was the extent of such speculative lending when Chase National Bank’s customers called in their money. Chase National had to follow their instructions, as did other New York banks. New York’s Stock Exchange could hardly respond to a demand for $4 billion at a short notice and collapsed. Within a year, production had fallen by 26 per cent, prices by 14 per cent, personal income by 14 per cent, and the Greatest Depression of recorded history was in progress — involuntary unemployment levels in America reaching 25 per cent. That is not, by any reading, what we have today. Yes, there has been plenty of bad lending, plenty of duping shareholders and workers and plenty of excessive managerial payoffs. It will all take a large toll, and affect markets across the world. But it will be a toll relative to our plush comfortable modern standards, not those of 1929-1933. In fact, modern decision-makers have the obvious advantage that they can look back at history and know what is not to be done. The US and the world economy are resilient enough to ride over even the extra uncertainty arising from the ongoing presidential campaign, and then some.”

These quotes are from recent publications and may be found most easily under “America’s financial crises” at my site http://www.independentindian.com.

What may be of interest to the Government of India’s economists also may be a sample of my recent short articles on India’s monetary and fiscal economics based on my research beginning with my doctoral work under Frank Hahn at Cambridge in the 1970s and followed by my work with James Buchanan and Milton Friedman in America in the 1980s and 1990s and later. One of these is even named “The Rangarajan Effect” which I first defined at a seminar invited by Dr Jadav at the RBI in May 2005!

“Rangarajan Effect”

Monetary Integrity and the Rupee (2008)

India’s Macroeconomics (2007)

Fiscal Instability

https://independentindian.com/2008/07/16/india-in-world-trade-payments/

Fallacious Finance: Congress, BJP, CPI-M et al may be leading India to hyperinflation (2007)

Our Policy Process: Self-Styled “Planners” Have Controlled India’s Paper Money For Decades

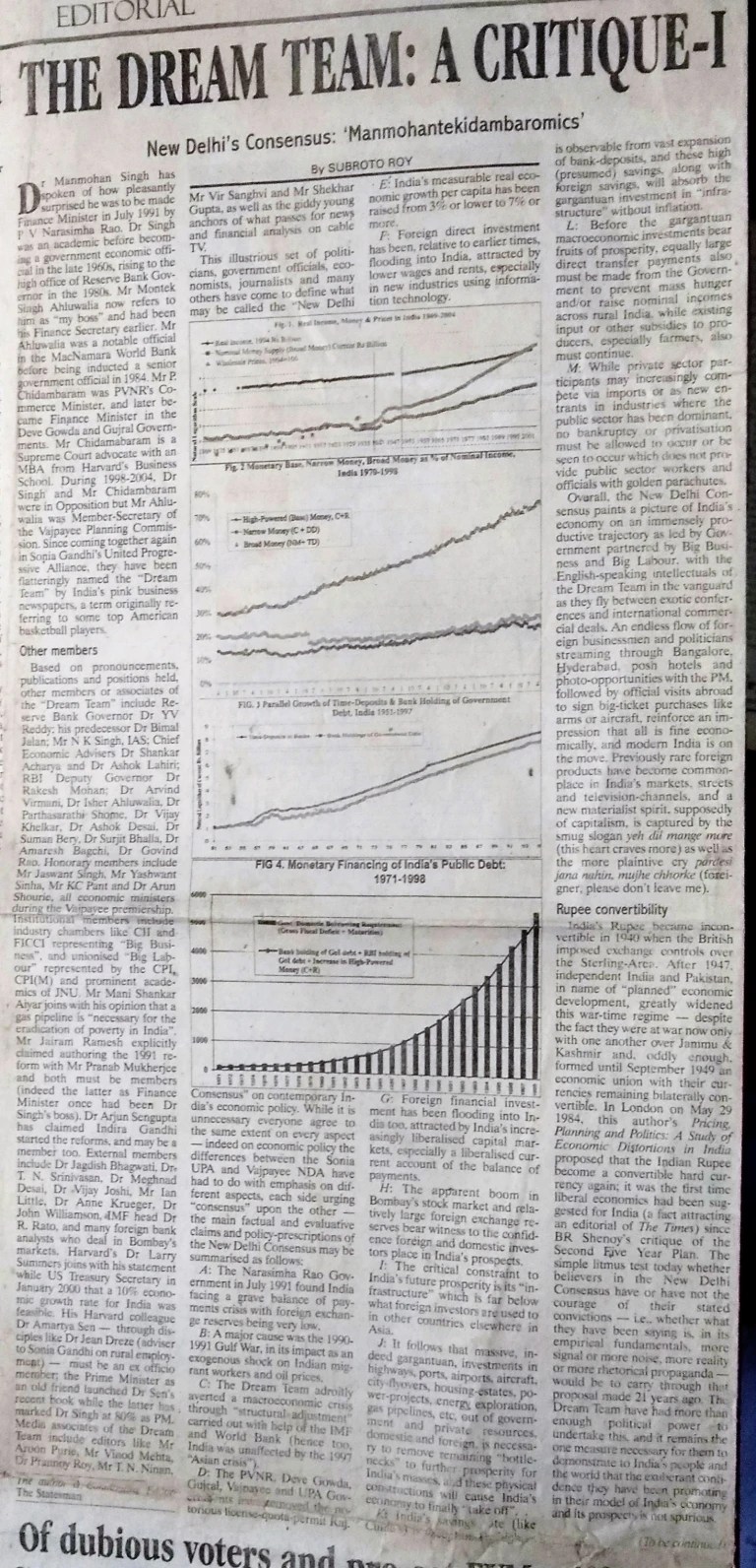

Growth of Real Income, Money & Prices in India 1869-2008

https://independentindian.com/2008/07/17/growth-government-delusion/

https://independentindian.com/2008/07/09/indian-inflation-upside-down-economics-from-new-delhis-establishment/

How to Budget: Thrift, Not Theft, Needs to Guide Our Public Finances

A Note on the Indian Policy Process

With warm regards,

Cordially,

Subroto Roy, PhD (Cantab.), BScEcon(London)

Sometime Adviser to the Late Rajiv Gandhi, 1990-1991

January 31, 1998 — drsubrotoroy

Transparency and Economic Policy-Making

An address by Professor Subroto Roy to the Asia-Pacific Public Relations Conference, (panel on Transparency chaired by C. R. Irani) January 30 1998.

This talk is dedicated to the memory of my sister Suchandra Bhattacharjee (14.02.1943-10.01.1998).

1. I would like to talk about transparency and economic policy-making in our country. For something to be transparent is, in plain language, for it to be able to be openly seen through, for it to not to be opaque, obscure or muddy, for it to be clear to the naked eye or to the reasonable mind. A clear glass of water is a transparent glass of water. Similarly, an open and easily comprehensible set of economic policies is a transparent set of economic policies.

The philosopher Karl Popper wrote a famous book after the Second World War titled The Open Society and its Enemies. It contained a passionate defence of liberal institutions and democratic freedoms and a bitter attack on totalitarian doctrines of all kinds. It generated a lot of controversy, especially over its likely misreading of the best known work of political philosophy since the 4th Century BC, namely, Plato’s Republic .[1] I shall borrow Popper’s terms ‘open society’ and ‘closed society’ and will first try to make this a useful distinction for modern times, and then apply it to the process of economic policy-making in India today.

2. An open society is one in which the ordinary citizen has reasonably easy access to any and all information relating to the public or social interest — whether the information is directly available to the citizen himself or herself, or is indirectly available to his or her elected representatives like MP’s and MLA’s. Different citizens will respond to the same factual information in different ways, and conflict and debate about the common good will result. But that would be part of the democratic process.

The assessment that any public makes about the government of the day depends on both good and bad news about the fate of the country at any given time. In an open society, both good news and bad news is out there in the pubic domain — open to be assessed, debated, rejoiced over, or wept about. If we win a cricket match or send a woman into space we rejoice. If we lose a child in a manhole or a busload of children in a river, we weep. If some tremendous fraud on the public exchequer comes to be exposed, we are appalled. And so on.

It is the hallmark of an open society that its citizens are mature enough to cope with both the good and the bad news about their country that comes to be daily placed before them. Or, perhaps more accurately, the experience of having to handle both good and bad news daily about their world causes the citizens in an open society to undergo a process of social maturation in formulating their understanding of the common good as well as their responses to problems or crises that the community may come to face. They might be thereby thought of as improving their civic capacities, as becoming better-informed and more discerning voters and decision-makers, and so becoming better citizens of the country in which they live.

The opposite of an open society is a closed society — one in which a ruling political party or a self-styled elite or nomenclatura keep publicly important information to themselves, and do not allow the ordinary citizen easy or reasonably free access to it. The reason may be merely that they are intent on accumulating assets for themselves as quickly as they can while in office, or that they are afraid of public anger and want to save their own skins from demands for accountability. Or it may be that they have the impression that the public is better off kept in the dark — that only the elite nomenclatura is in position to use the information to serve the national interest.

In a closed society it is inevitable that bad news comes to be censored or suppressed by the nomenclatura, and so the good news gets exaggerated in significance. News of economic disasters, military defeats or domestic uprisings gets suppressed. News of victories or achievements or heroics gets exaggerated. If there are no real victories, achievements or heroics, fake ones have to be invented by government hacks — although the suppressed bad news tends to silently whisper all the way through the public consciousness in any case.

Such is the way of government propaganda in almost every country, even those that pride themselves on being free and democratic societies. Dostoevsky’s cardinal advice in Brothers Karamasov was: “Above all, never lie to yourself”. Yet people in power tend to become so adept at propaganda that they start to deceive themselves and forget what is true and what is false, or worse still, cannot remember how to distinguish between true and false in the first place. In an essay thirty years ago titled Truth and Politics, the American scholar Hannah Arendt put it like this:

“Insofar as man carries within himself a partner from whom he can never win release, he will be better off not to live with a murderer or a liar; or: since thought is the silent dialogue carried out between me and myself, I must be careful to keep the integrity of this partner intact, for otherwise I shall surely lose the capacity for thought altogether.”[2]

3. Closed societies may have been the rule and open societies the exception for most of human history. The good news at the end of the 20th Century is surely that since November 7 1989, when the Berlin Wall fell, the closed society has officially ceased to be a respectable form of human social organization. The age of mass access to television and telecommunications at the end of the 20th Century may be spelling the permanent end of totalitarianism and closed societies in general. The Berlin Wall was perhaps doomed to fall the first day East Germans were able to watch West German television programs.

Other than our large and powerful neighbour China, plus perhaps North Korea, Myanmar, and some Islamic countries, declared closed societies are becoming hard to find, and China remains in two minds whether to be open or closed. No longer is Russia or Romania or Albania or South Africa closed in the way each once was for many years. There may be all sorts of problems and confusions in these countries but they are or trying to become open societies.

Under the glare of TV cameras in the 21st Century, horrors like the Holocaust or the Gulag or even an atrocity like Jalianwalla Bag or the Mai Lai massacre will simply not be able to take place anywhere in the world. Such things are not going to happen, or if they do happen, it will be random terrorism and not systematic, large scale genocide of the sort the 20th Century has experienced. The good news is that somehow, through the growth of human ingenuity that we call technical progress, we may have made some moral progress as a species as well.

4. My hypothesis, then, is that while every country finds its place on a spectrum of openness and closedness with respect to its political institutions and availability of information, a broad and permanent drift has been taking place as the 20th Century comes to an end in the direction of openness.

With this greater openness we should expect bad news not to come to be suppressed or good news not to come to be exaggerated in the old ways of propaganda. Instead we should expect more objectively accurate information to come about in the public domain — i.e., better quality and more reliable information, in other words, more truthful information. This in turn commensurately requires more candour and maturity on the part of citizens in discussions about the national or social interest. Closed society totalitarianism permitted the general masses to remain docile and unthinking while the nomenclatura make the decisions. Dostoevsky’s Grand Inquisitor said that is all that can be expected of the masses. Open society transparency and democracy defines the concept of an ordinary citizen and requires from that citizen individual rationality and individual responsibility. It is the requirement Pericles made of the Athenians:

“Here each individual is interested not only in his own affairs but in the affairs of the state as well; even those who are mostly occupied with their own business are extremely well-informed on general politics – this is a peculiarity of ours: we do not say that a man who takes no interest in politics is a man who minds his own business; we say that he has no business here at all.”[3]

5. All this being said, I am at last in a position to turn to economic policy in India today. I am sorry to have been so long-winded and pedantic but now I can state my main substantive point bluntly: in India today, there is almost zero transparency in the information needed for effective macroeconomic policy-making whether at the Union or State levels. To illustrate by some examples.

(A) Macroeconomic policy-making in any large country requires the presence of half a dozen or a dozen well-defined competing models produced by the government and private agencies, specifying plausible causal links between major economic variables, and made testable against time-series data of reasonably long duration. In India we seem to have almost none. The University Economics Departments are all owned by some government or other and can hardly speak out with any academic freedom. When the Ministry of Finance or RBI or Planning Commission, or the India teams of the World Bank or IMF, make their periodic statements they do not appear to be based on any such models or any such data-base. If any such models exist, these need to be published and placed in the public domain for thorough discussion as to their specification and their data. Otherwise, whatever is being predicted cannot be assessed as being very much more reliable than the predictions obtained from the Finance Minister’s astrologer or palmist. (NB: Horse-Manure is a polite word used in the American South for what elsewhere goes by the initials of B. S.). Furthermore, there is no follow-up or critical review to see whether what the Government said was going to happen a year ago has in fact happened, and if not, why not.

(B) The Constitution of India defines many States yet no one seems to be quite certain how many States really constitute the Union of India at any given time. We began with a dozen. Some 565 petty monarchs were successfully integrated into a unitary Republic of India, and for some years we had sixteen States. But today, do we really have 26 States? Is Delhi a State? UP with 150 million people would be the fifth or sixth largest country in the world on its own; is it really merely one State of India? Are 11 Small States de facto Union Territories in view of their heavy dependence on the Union? Suppose we agreed there are fifteen Major States of India based on sheer population size: namely, Andhra, Assam, Bihar, Gujarat, Haryana, Karnataka, Kerala, MP, Maharashtra, Orissa, Punjab, Rajasthan, Tamil Nadu, UP and West Bengal. These States account for 93% of the population of India. The average population of these 15 Major States is 58 million people each. That is the size of a major country like France or Britain. In other words, the 870 million people in India’s Major States are numerically 15 Frances or 15 Britains put together.

Yet no reliable, uniformly collected GDP figures exist for these 15 States. The RBI has the best data, and these are at least two years old, and the RBI will tell you without further explanation that the data across States are not comparable. If that is the case at State-level, I do not see how the national-level Gross Domestic Product can possibly be estimated with any meaningfulness at all.

(C) Then we hear about the Government Budget deficit as a percentage of GDP. Now any national government is able to pay for its activities only by taxation or borrowing or by using its monopoly over the domestic medium of exchange to print new money. In India today, universal money-illusion seems to prevail. It would not be widely recognised by citizens, journalists or policy-makers that, say, 100,000 Rupees nominally taxed at 10% under 20% inflation leaves less real disposable income than the same taxed at 20% with 5% inflation. This is in part because inflation figures are unknown or suspect. There is no reliable all-India or State-level consumer price index. The wholesale price index on the basis of which the Government of India makes its inflation statements, may not accurately reflect the actual decline in the purchasing power of money, as measured, say, by rises in prices of alternative stores of value like land. The index includes artificially low administered or subsidized prices for petroleum, cereals, and electricity. To the extent these prices may be expected to move towards international equilibrium prices, the index contains a strong element of deferred inflation. One urgent task for all macroeconomic research in India is construction of reliable price-data indices at both Union and State levels, or at a minimum, the testing for reliability by international standards of series currently produced by Government agencies.

Without reliable macroeconomic information being spread widely through a reasonably well-informed electorate, the Government of India has been able to wash away fiscal budget constraints by monetization and inflation without significant response from voters. The routine method of meeting deficits has become “the use of the printing press to manufacture legal tender paper money”, either directly by paying Government creditors “with new paper money specially printed for the purpose” or indirectly by paying creditors “out of loans to itself from the Central Bank”, issuing paper money to that amount. Every Budget of the Government of India, including the most recent ones of 1996 and 1997, comes to be attended by detailed Press discussion with regard to the minutae of changes in tax rates or tax-collection — yet the enormous phenomena of the automatic monetization of the Government’s deficit is ill-understood and effectively ignored. Historically, a policy of monetization started with the British Government in India during the Second World War, with a more than five-fold increase in money supply occurring between 1939 and 1945. Inflation rates never seen in India before or since were the result (Charts 0000), attended by the Great Famine of 1942/43. Though these were brought down after succession of C. D. Deshmukh as Governor of the Reserve Bank, the policy of automatic monetization did not cease and continues until the present day. Inflation “sooner or later destroys the confidence, not only of businessmen, but of the whole community, in the future value of the currency. Then comes the stage known as “the flight from the currency.” Had the Rupee been convertible during the Bretton Woods period, depreciation would have signalled and helped to adjust for disequilibrium. But exchange-controls imposed during the War were enlarged by the new Governments of India and Pakistan after the British departure to exclude convertible Sterling Area currencies as well. With the Rupee no longer convertible, internal monetization of deficits could continue without commensurate exchange-rate depreciation.

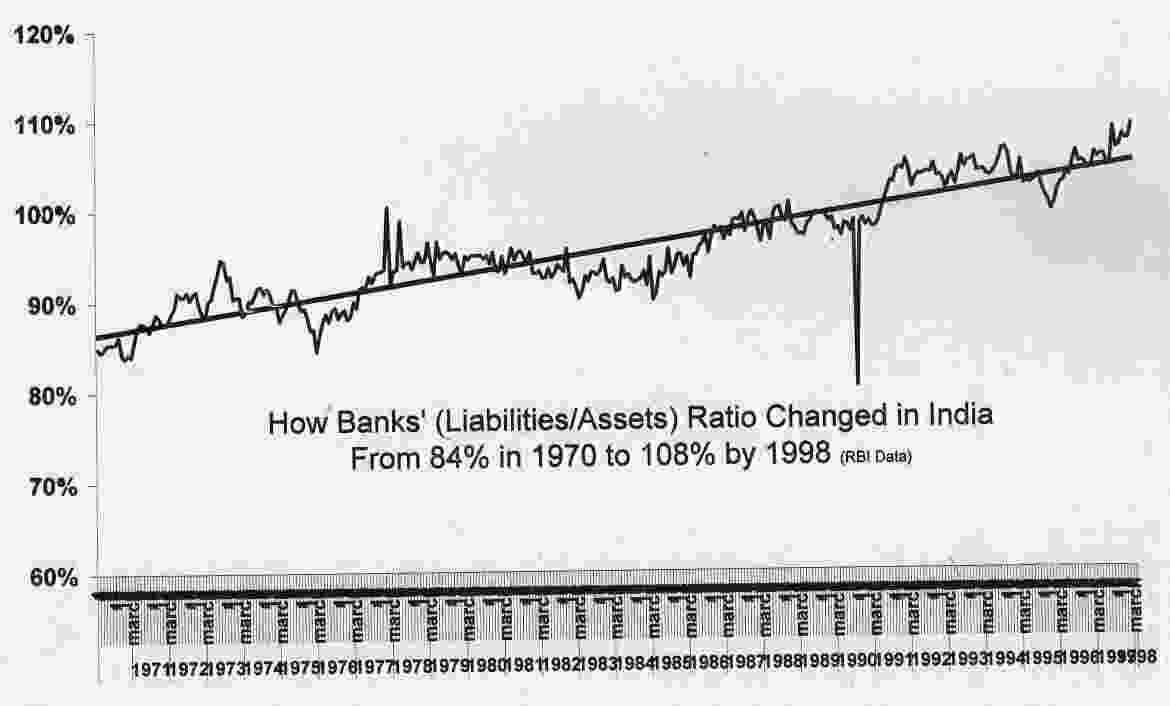

The Reserve Bank was originally supposed to be a monetary authority independent of the Government’s fiscal compulsions. It has been prevented from developing into anything more than a department of the Ministry of Finance, and as such, has become the captive creditor of the Government. The RBI in turn has utilized its supervisory role over banking to hold captive creditors, especially nationalized banks whose liabilities account for 90% of commercial bank deposits in the country. Also captive are nationalized insurance companies and pension funds. Government debt instruments show on the asset side of these balance-sheets. To the extent these may not have been held had banks been allowed to act in the interests of proper management of depositors’ liabilities and share-capital according to normal principles, these are pseudo-assets worth small fractions of their nominal values. Chart 0000 shows that in the last five years the average term structure of Government debt has been shortening rapidly, suggesting the Government is finding it increasingly difficult to find creditors, and portending higher interest rates.

General recognition of these business facts, as may be expected to come about with increasing transparency, would be a recipe for a crisis of confidence in the banking and financial system if appropriate policies were not in place beforehand.

(D) As two last examples, I offer two charts. The first shows the domestic interest burden of the Government of India growing at an alarming rate, even after it has been deflated to real terms. The second tries to show India’s foreign assets and liabilities together – we always come to know what is happening to the RBI’s reserve levels, what is less known or less understood is the structure of foreign liabilities being accumulated by the country. Very roughly speaking, in terms that everyone can understand, every man, woman and child in India today owes something like 100 US dollars to the outside world. The Ministry of Finance will tell you that this is not to be worried about because it is long-term debt and not short-term debt. Even if we take them at their word, interest payments still have to be paid on long-term debt, say at 3% per annum. That means for the stock of debt merely to be financed, every man, woman and child in India must be earning $3 every year in foreign exchange via the sale of real goods and services abroad. I.e., something like $3 billion must be newly earned every year in foreign exchange merely to finance the existing stock of debt. Quite clearly, that is not happening and it would stretch the imagination to see how it can be made to happen.

In sum, then, India, blessed with democratic political traditions which we had to take from the British against their will — remember Tilak, “Freedom is my birthright, and I shall have it” — may still be stuck with a closed society mentality when it comes to the all-important issue of economic policy. There is simply an absence in Indian public discourse of vigourous discussion of economic models and facts, whether at Union or State levels. A friendly foreign ambassador pointedly observed an absence in India of political philosophy. It may be more accurate to say that without adequate experience of a normal agenda of government being seen to be practised, widespread ignorance regarding fiscal and monetary causalities and inexperience of the technology of governance remains in the Indian electorate, as well as among public decision-makers at all levels. Our politicians seem to spend an inordinate amount of their time either garlanding one another with flowers or garlanding statues and photographs of the glorious dead. It is high time they stopped to think about the living and the future.

[1] Renford Bambrough (ed.) Plato, Popper and Politics: Some Contributions to a Modern Controversy, 1967.

[2] Philosophy, Politics and Society, 2nd Series, Peter Laslett & W. G. Runciman (eds.), 1967.

[3] Thucydides, History of the Pelopennesian War, II.40.