Delhi can never be improved — until the rest of India improves!

February 13, 2015 — drsubrotoroyThe fascist solution that was, as I recall, suggested momentarily by a former Congress CM of Delhi, would be to forcibly prevent people from coming in from the outside. Apparently the PRC as a totalitarian regime has some kind of system of internal passports which restricts citizens from travelling into metros on their own free will. That cannot work in free India, where the Constitution would

Some of My Works, Interviews etc on India’s Money, Public Finance, Banking, Trade, BoP, Land, etc (an incomplete list)

November 23, 2013 — drsubrotoroy

My “Critique of Monetary Ideas of Manmohan & Modi: the Roy Model explaining to Bimal Jalan, Nirmala Sitharaman, RBI etc what it is they are doing” of 2019 is here.

Foundations of India’s Political Economy: Towards an Agenda for the 1990s edited by Subroto Roy & William E James, 1986-1992… pdf copy uploaded 2021

Pricing, Planning & Politics: A Study of Economic Distortions in India 1984, uploaded as pdf 2021

My Sep 2019 recommendation PM address each State Legislature, get all India Govt Accounting & Public Decision Making to have integrity; 16 May 2014 Advice scrap “Planning Commission”,integrate its assets with the Treasury, get the nationalised banks & RBI out of the Treasury

My critical assessment dated 23 August 2013 of Professors Jagdish Bhagwati & Amartya Sen and Dr Manmohan Singh is here…

My critique of PM Modi’s 8 November 2016 statement began on Twitter immediately, and is summarized here “Modi & Monetary Theory: Economic Consequences of the Prime Minister of India”

My critical assessment dated 19 August 2013 of Professor Raghuram Rajan is here and here.

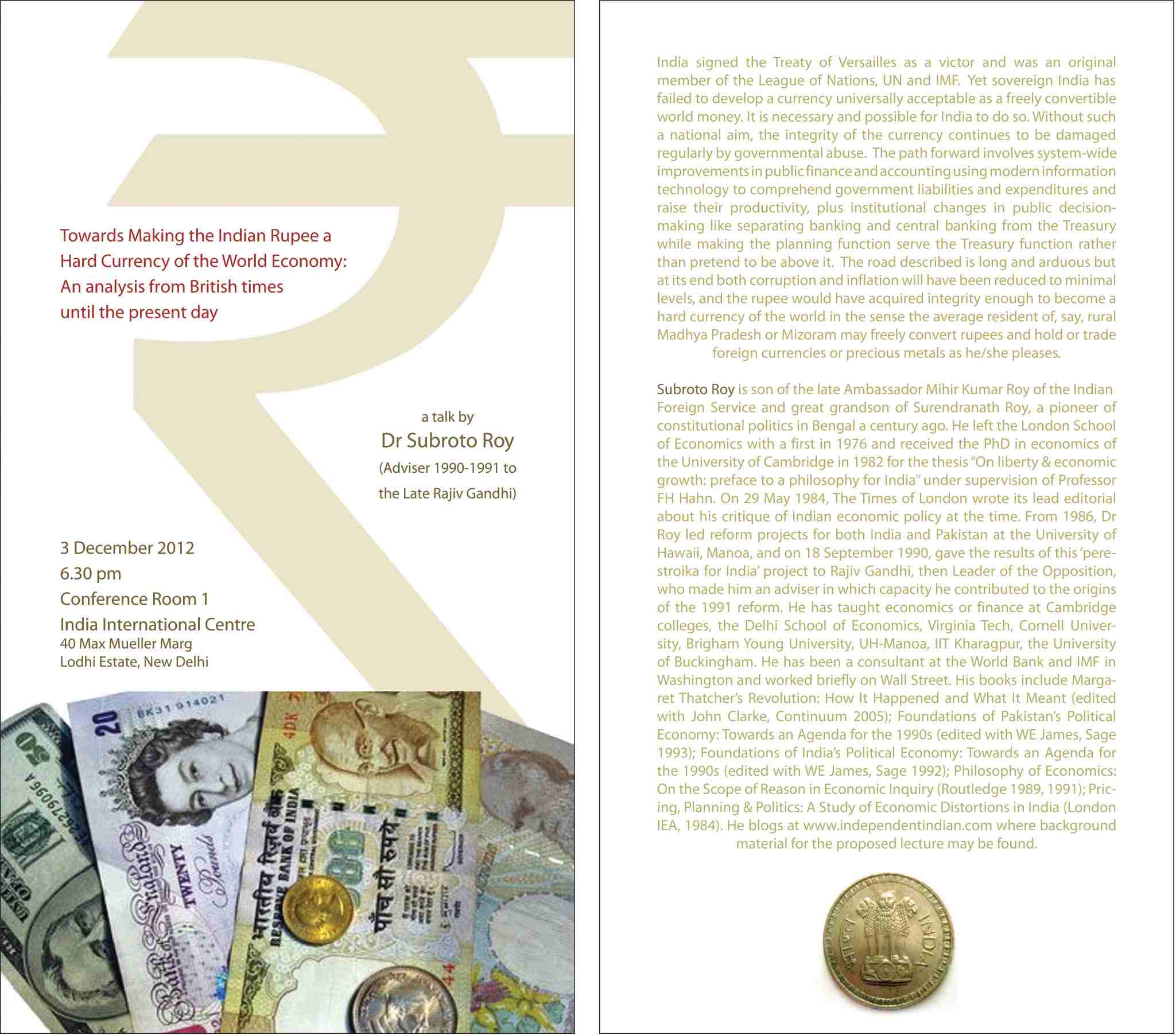

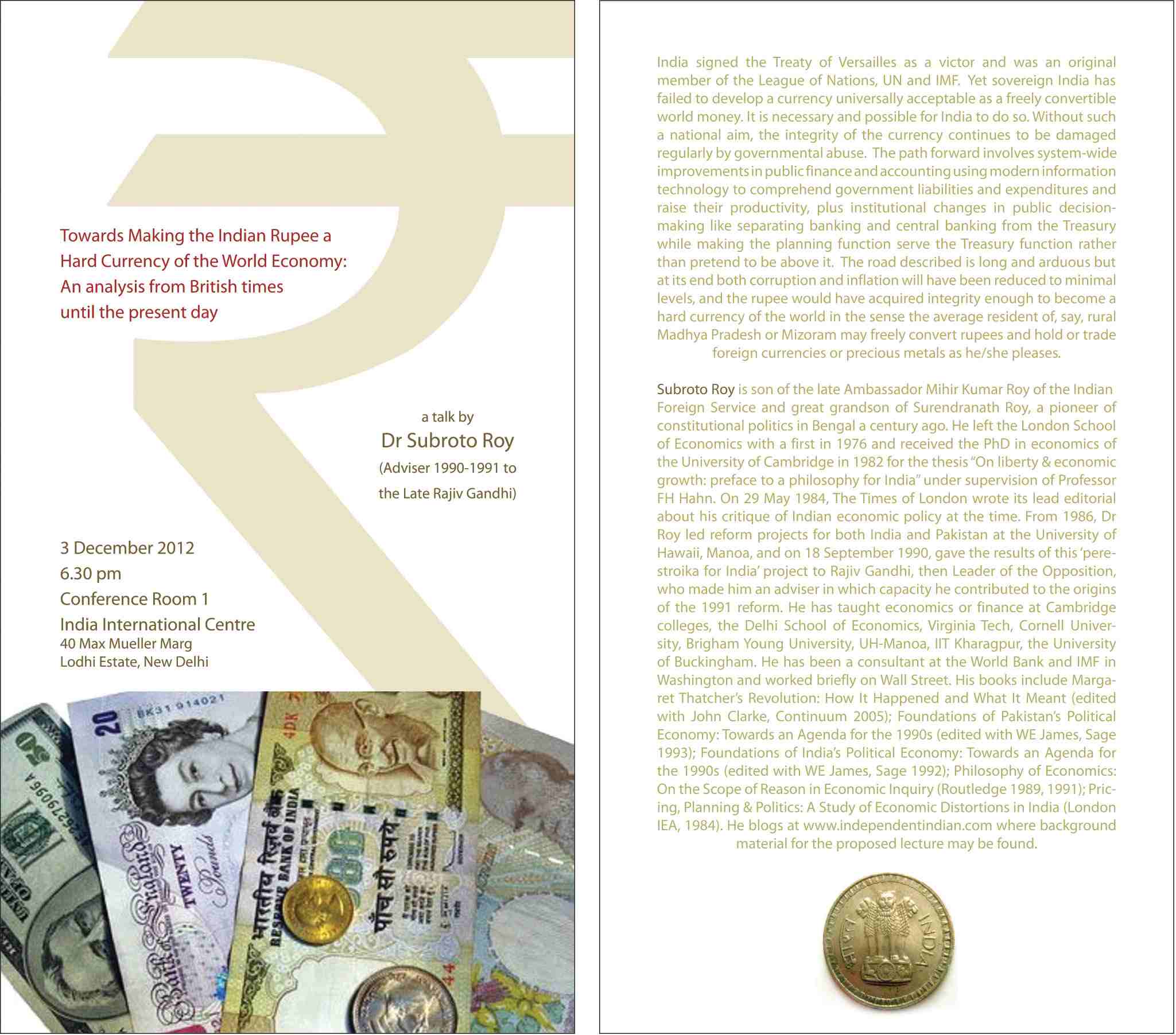

My 3 Dec 2012 Delhi talk on India’s Money is now available at You-Tube in an audio version here.

My July 2012 article “India’s Money” in the Caymans Financial Review is here and here https://independentindian.com/2012/07/21/my-article-indias-money-in-the-cayman-financial-review-july-2012/

My 5 December 2012 interview by Mr Paranjoy Guha Thakurta, on Lok Sabha TV, the channel of India’s Lower House of Parliament, broadcast for the first time on 9 December 2012 on Lok Sabha TV, is here and here in two parts.

My interview by GDI Impuls banking quarterly of Zürich published on 6 Dec 2012 is here.

My interview by Ragini Bhuyan of Delhi’s Sunday Guardian published on 16 Dec 2012 is here.

“Monetary Integrity and the Rupee” (2008)

https://independentindian.com/2008/09/28/monetary-integrity-and-the-rupee/

“India’s Macroeconomics” (2007)

“Fiscal Instability” (2007)

“Fallacious Finance” (2007)

https://independentindian.com/2007/03/05/fallacious-finance-the-congress-bjp-cpi-m-et-al-may-be-leading-india-to-hyperinflation/

https://independentindian.com/2021/12/01/on-the-simplest-smallest-most-universal-direct-flattax-of-500-rupees-per-annum-for-india-accruing-to-the-states-with-a-bpl-exemption-too/

Budgets & Financial Positions of Three of India’s Most Populous States (combined population c.300 million)…Brought to you especially by Dr Subroto Roy… Feel free to use (with acknowledgment)…

“Growth and Government Delusion” (2008)

https://independentindian.com/2008/02/22/growth-government-delusion/

“Distribution of Govt of India Expenditure (Net of Operational Income) 1995”

https://independentindian.com/2008/07/27/distribution-of-govt-of-india-expenditure-net-of-operational-income-1995/

“India in World Trade & Payments” (2007)

https://independentindian.com/2007/02/12/india-in-world-trade-payments/

“Path of the Indian Rupee 1947-1993″ (1993)

https://independentindian.com/1993/06/01/path-of-the-indian-rupee-1947-1993/

“Our Policy Process” (2007)

https://independentindian.com/2007/02/20/our-policy-process-self-styled-planners-have-controlled-indias-paper-money-for-decades/

“Indian Money and Credit” (2006)

https://independentindian.com/2006/08/06/indian-money-and-credit/

“Indian Money and Banking” (2006)

https://independentindian.com/2006/04/23/indian-money-and-banking/

“Indian Inflation” (2008)

https://independentindian.com/2008/04/16/indian-inflation-upside-down-economics-from-new-delhis-establishment/

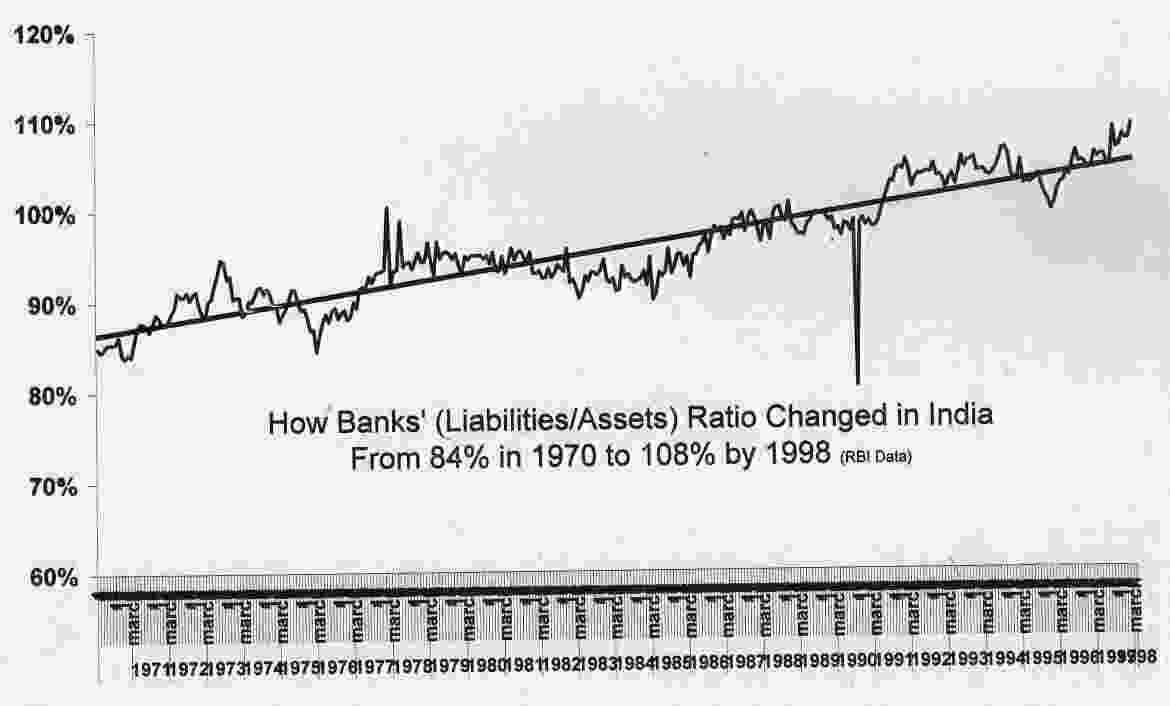

How the Liabilities/Assets Ratio of Indian Banks Changed from 84% in 1970 to 108% in 1998 https://independentindian.com/2008/10/20/how-the-liabilitiesassets-ratio-of-indian-banks-changed-from-84-in-1970-to-108-in-1998/

“Growth of Real Income, Money & Prices in India 1869-2004” (2005)

https://independentindian.com/2008/07/28/growth-of-real-income-money-prices-in-india-1869-2004/

“How to Budget” (2008)

https://independentindian.com/2008/02/26/how-to-budget-thrift-not-theft-should-guide-our-public-finances/

“Waffle but No Models of Monetary Policy: The RBI and Financial Repression (2005)”

https://independentindian.com/2005/10/27/waffle-but-no-models-of-monetary-policy-the-rbi-and-financial-repression/

“The Dream Team: A Critique” (2006)

https://independentindian.com/2006/01/08/the-dream-team-a-critique/

“Against Quackery” (2007)

https://independentindian.com/2007/09/24/against-quackery/

“Mistaken Macroeconomics” (2009)

https://independentindian.com/2009/06/12/mistaken-macroeconomics-an-open-letter-to-prime-minister-dr-manmohan-singh/

Towards a Highly Transparent Fiscal & Monetary Framework for India’s Union & State Governments (RBI lecture 29 April 2000)

https://independentindian.com/2000/04/29/towards-a-highly-transparent-fiscal-monetary-framework-for-india%E2%80%99s-union-state-governments/

“The Indian Revolution (2008)”

https://independentindian.com/2008/12/08/the-indian-revolution/

Can India Become an Economic Superpower or Will There Be a Monetary Meltdown? (2005)

https://independentindian.com/2005/05/05/can-india-become-an-economic-superpower-or-will-there-be-a-monetary-meltdown-2005/

Memo to Kaushik Basu, 2010

Land, Liberty, & Value, 2006

https://independentindian.com/2006/12/31/land-liberty-value/

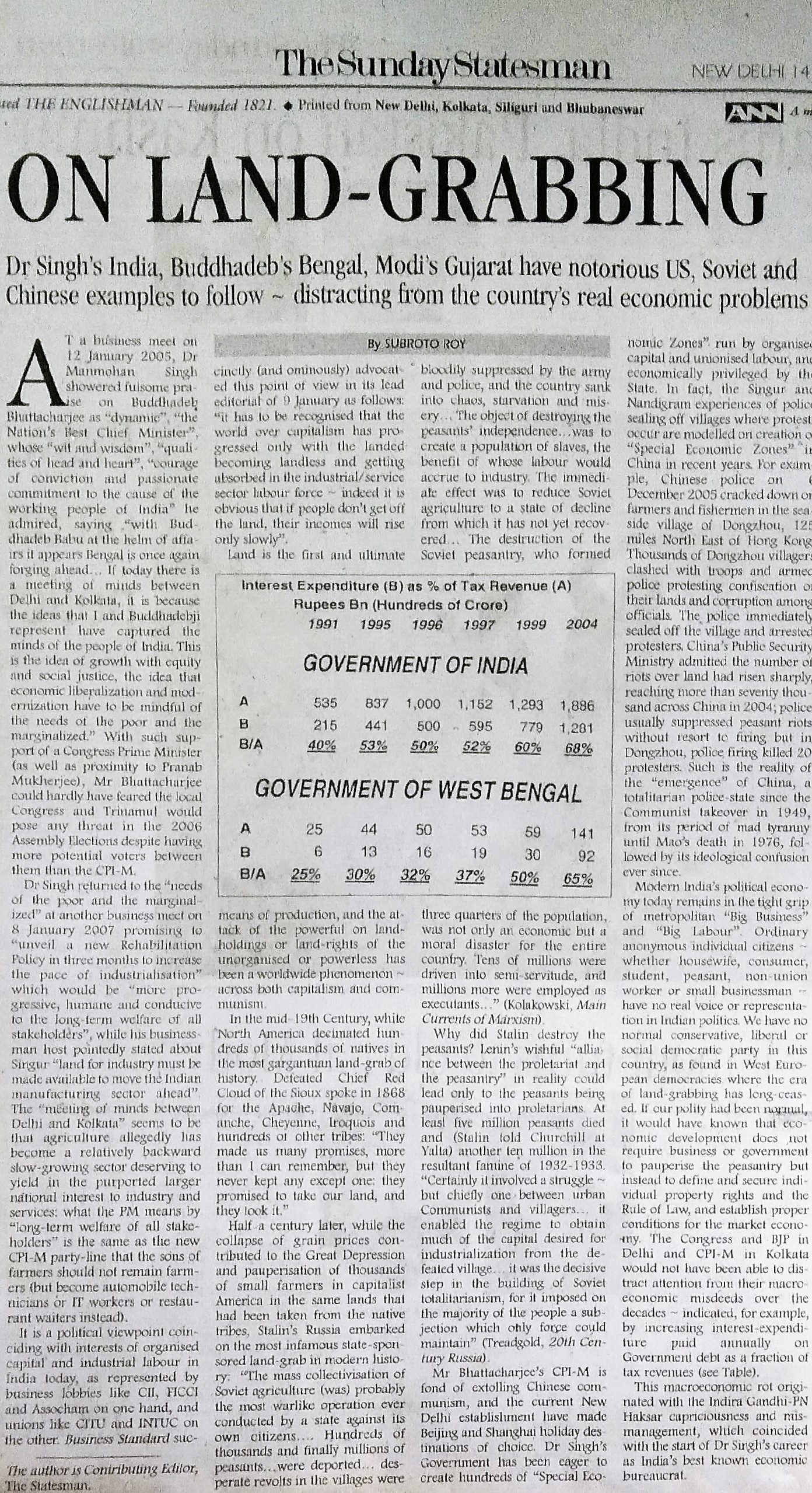

On Land-Grabbing, 2007

https://independentindian.com/2007/01/14/on-land-grabbing/

No Marxist MBAs? An amicus curiae brief for the Honourable High Court

https://independentindian.com/2007/08/29/no-marxist-mbasan-amicus-curae-brief-for-the-honourable-high-court/

Coverage in The *Asian Age*/*Deccan Herald* of 4 Dec 2012.

.

Has business-cycle theory become easy for the dimwitted?

November 13, 2009 — drsubrotoroyFrom Facebook:

Subroto Roy is amazed that business-cycle theory and history — always a most difficult, subtle and confusing part of economics — has now become child’s play for everyone except himself, and even the most dimwitted commentator claims to know that China and India were down last month but now seem up and similar profound truths….

My Ten Articles on China, Tibet, Xinjiang, Taiwan in relation to India (2007-2009)

September 19, 2009 — drsubrotoroy

I have had a close interest in China ever since the “Peking Spring” more than thirty years ago (if not from when I gave all my saved pocket money to Nehru in 1962 to fight the Chinese aggression) but I had not published anything relating to China until 2007-2008 when I published the ten articles listed below:

“Understanding China”, The Statesman Oct 22 2007

“India-US interests: Elements of a serious Indian foreign policy”, The Statesman Oct 30 2007

“China’s India Aggression”, The Statesman, Nov 5 2007,

“Surrender or Fight? War is not a cricket match or Bollywood movie. Can India fight China if it must? “ The Statesman, Dec 4 2007

“China’s Commonwealth: Freedom is the Road to Resolving Taiwan, Tibet, Sinkiang” The Statesman, December 17, 2007

“Nixon & Mao vs India: How American foreign policy did a U-turn about Communist China’s India aggression”. The Statesman, January 7 2008.

“Lessons from the 1962 War: there are distinct Tibetan, Chinese and Indian points of view that need to be mutually comprehended,” The Statesman, January 15, 2008

“China’s India Example: Tibet, Xinjiang May Not Be Assimilated Like Inner Mongolia, Manchuria”, The Statesman, March 25, 2008

“China’s force and diplomacy: The need for realism in India”, The Statesman, May 31, 2008

“Transparency and history” (with Claude Arpi), Business Standard, Dec 31 2008

With new tensions on the Tibet-India border apparently being caused by the Chinese military, these may be helpful for India to determine a Plan B, or even a Plan A, in its dealings with Communist China.

See also https://independentindian.com/1990/09/18/my-meeting-jawaharlal-nehru-2/

Mistaken Macroeconomics: An Open Letter to Prime Minister Dr Manmohan Singh 12 June 2009

June 12, 2009 — drsubrotoroy12 June 2009

The Hon’ble Dr Manmohan Singh, MP, Rajya Sabha

Prime Minister of India

Respected Pradhan Mantriji:

In September 1993 at the residence of the Indian Ambassador to Washington, I had the privilege of being introduced to you by our Ambassador the Hon’ble Siddhartha Shankar Ray, Bar-at-Law. Ambassador Ray was kind enough to introduce me saying the 1991 “Congress manifesto had been written on (my laptop) computer” – a reference to my work as adviser on economic and other policy to the late Rajiv Gandhi in his last months. I presented you a book Foundations of India’s Political Economy: Towards an Agenda for the 1990s created and edited by myself and WE James at the University of Hawaii since 1986 — the unpublished manuscript of that book had reached Rajivji by my hand when he and I first met on September 18 1990. Tragically, my pleadings in subsequent months to those around him that he seemed to my layman’s eyes vulnerable to the assassin went unheeded.

When you and I met in 1993, we had both forgotten another meeting twenty years earlier in Paris. My father had been a long-time friend of the late Brahma Kaul, ICS, and the late MG Kaul, ICS, who knew you in your early days in the Government of India. In the late summer of 1973, you had acceded to my father’s request to advise me about economics before I embarked for the London School of Economics as a freshman undergraduate. You visited our then-home in Paris for about 40 minutes despite your busy schedule as part of an Indian delegation to the Aid-India Consortium. We ended up having a tense debate about the merits (as you saw them) and demerits (as I saw them) of the Soviet influence on Indian economic “planning”. You had not expected such controversy from a lad of 18 but you were kindly disposed and offered when departing to write a letter of introduction to Amartya Sen, then teaching at the LSE, which you later sent me and which I was delighted to carry to Professor Sen.

I may add my father, back in 1973 in Paris, had predicted to me that you would become Prime Minister of India one day, and he, now in his 90s, is joined by myself in sending our warm congratulations at the start of your second term in that high office.

The controversy though that you and I had entered that Paris day in 1973 about scientific economics as applied to India, must be renewed afresh!

This is because of your categorical statement on June 9 2009 to the new 15th Lok Sabha:

“I am convinced, since our savings rate is as high as 35%, given the collective will, if all of us work together, we can achieve a growth-rate of 8%-9%, even if the world economy does not do well.” (Statement of Dr Manmohan Singh to the Lok Sabha, June 9 2009)

I am afraid there may be multiple reasons why such a statement is gravely and incorrigibly in error within scientific economics. From your high office as Prime Minister in a second term, faced perhaps with no significant opposition from either within or without your party, it is possible the effects of such an error may spell macroeconomic catastrophe for India.

As it happens, the British Labour Party politician Dr Meghnad Desai made an analogous statement to yours about India when he claimed in 2006 that China

“now has 10.4% growth on a 44 % savings rate… ”

Indeed the idea that China and India have had extremely high economic growth-rates based on purportedly astronomical savings rates has become a commonplace in recent years, repeated endlessly in international and domestic policy circles though perhaps without adequate basis.

1. Germany & Japan

What, at the outset, is supposed to be measured when we speak of “growth”? Indian businessmen and their media friends seem to think “growth” refers to something like nominal earnings before tax for the organised corporate sector, or any unspecified number that can be sold to visiting foreigners to induce them to park their funds in India: “You will get a 10% return if you invest in India” to which the visitor says “Oh that must mean India has 10% growth going on”. Of such nonsense are expensive international conferences in Davos and Delhi often made.

You will doubtless agree the economist at least must define economic growth properly and with care — what is referred to must be annual growth of per capita inflation-adjusted Gross Domestic Product. (Per capita National Income or Net National Product would be even better if available).

West Germany and Japan had the highest annual per capita real GDP growth-rates in the world economy starting from devastated post-World War II initial conditions. What were their measured rates?

West Germany: 6.6% in 1950-1960, falling to 3.5% by 1960-1970 falling to 2.4% by 1970-1978.

Japan: 6.8 % in 1952-1960 rising to 9.4% in 1960-1970 falling to 3.8 % in 1970-1978.

Thus in recent decadesonly Japan measured a spike in the 1960s of more than 9% annual growth of real per capita GDP. Now India and China are said to be achieving 8%-10 % and more year after year routinely!

Perhaps we are observing an incredible phenomenon of world economic history. Or perhaps it is just something incredible, something false and misleading, like a mirage in the desert.

You may agree that processes of measurement of real income in India both at federal and provincial levels, still remain well short of the world standards described by the UN’s System of National Accounts 1993. The actuality of our real GDP growth may be better than what is being measured or it may be worse than what is being measured – from the point of view of public decision-making we at present simply do not know which it is, and to overly rely on such numbers in national decisions may be unwise. In any event, India’s population is growing at near 2% so even if your Government’s measured number of 8% or 9% is taken at face-value, we have to subtract 2% population growth to get per capita figures.

2. Growth of the aam admi’s consumption-basket

The late Professor Milton Friedman had been an invited adviser in 1955 to the Government of India during the Second Five Year Plan’s formulation. The Government of India suppressed what he had to say and I had to publish it 34 years later in May 1989 during the 1986-1992 perestroika-for-India project that I led at the University of Hawaii in the United States. His November 1955 Memorandum to the Government of India is a chapter in the book Foundations of India’s Political Economy: Towards an Agenda for the 1990s that I and WE James created.

At the 1989 project-conference itself, Professor Friedman made the following astute observation about all GNP, GDP etc growth-numbers that speaks for itself:

“I don’t believe the term GNP ought to be used unless it is supplemented by a different statistic: the rate of growth of the average consumption basket consumed by the ordinary individual in the country. I think GNP rates of growth can give very misleading information. For example, you have rapid rates of growth of GNP in the Soviet Union with a declining standard of life for the people. Because GNP includes monuments and includes also other things. I’m not saying that that is the case with India; I’m just saying I would like to see the two figures together.”

You may perhaps agree upon reflection that not only may our national income growth measurements be less robust than we want, it may be better to be measuring something else instead, or as well, as a measure of the economic welfare of India’s people, namely, “the rate of growth of the average consumption basket consumed by the ordinary individual in the country”, i.e., the rate of growth of the average consumption basket consumed by the aam admi.

It would be excellent indeed if you were to instruct your Government’s economists and other spokesmen to do so this as it may be something more reliable as an indicator of our economic realities than all the waffle generated by crude aggregate growth-rates.

3. Logic of your model

Thirdly, the logic needs to be spelled out of the economic model that underlies such statements as yours or Meghnad Desai’s that seek to operationally relate savings rates to aggregate growth rates in India or China. This seems not to have been done publicly in living memory by the Planning Commission or other Government economists. I have had to refer, therefore, to pages 251-253 of my own Cambridge doctoral thesis under Professor Frank Hahn thirty years ago, titled “On liberty and economic growth: preface to a philosophy for India”, where the logic of such models as yours was spelled out briefly as follows:

Let

Kt be capital stock

Yt be national output

It be the level of real investment

St be the level of real savings

By definition

It = K t+1 – Kt

By assumption

Kt = k Yt 0 < k < 1

St = sYt 0 < s <1

In equilibrium ex ante investment equals ex ante savings

It = St

Hence in equilibrium

sYt = K t+1 – Kt

Or

s/k = g

where g is defined to be the rate of growth (Y t+1-Yt)/Yt .

The left hand side then defines the “warranted rate of growth” which must maintain the famous “knife-edge” with the right hand side “natural rate of growth”.

Your June 9 2009 Lok Sabha statement that a 35% rate of savings in India may lead to an 8%-9% rate of economic growth in India, or Meghnad Desai’s statement that a 44% rate of savings in China led to a 10.4% growth there, can only be made meaningful in the context of a logical economic model like the one I have given above.

[In the open-economy version of the model, let Mt be imports, Et be exports, Ft net capital inflows.

Assume

Mt = aIt + bYt 0 < a, b < 1

Et = E for all t

Balance of payments is

Bt = Mt – Et – Ft

In equilibrium It = St + Bt

Or

Ft = (s+b) Yt – (1-a) It – E is a kind of “warranted” level of net capital inflow.]

You may perhaps agree upon reflection that building the entire macroeconomic policy of the Government of India merely upon a piece of economic logic as simplistic as the

s/k = g

equation above, may spell an unacceptable risk to the future economic well-being of our vast population. An alternative procedural direction for macroeconomic policy, with more obviously positive and profound consequences, may have been that which I sought to persuade Rajiv Gandhi about with some success in 1990-1991. Namely, to systematically seek to improve towards normalcy the budgets, financial positions and decision-making capacities of the Union and all state and local governments as well as all public institutions, organisations, entities, and projects in general, with the aim of making our domestic money a genuine hard currency of the world again after seven decades, so that any ordinary resident of India may hold and trade precious metals and foreign exchange at his/her local bank just like all those glamorous privileged NRIs have been permitted to do. Such an alternative path has been described in “The Indian Revolution”, “Against Quackery”, “The Dream Team: A Critique”, “India’s Macroeconomics”, “Indian Inflation”, etc.

4. Gross exaggeration of real savings rate by misreading deposit multiplication

Specifically, I am afraid you may have been misled into thinking India’s real savings rate, s, is as high as 35% just as Meghnad Desai may have misled himself into thinking China’s real savings rate is as high as 44%.

Neither of you may have wanted to make such a claim if you had referred to the fact that over the last 25 years, the average savings rate across all OECD countries has been less than 10%. Economic theory always finds claims of discontinuous behaviour to be questionable. If the average OECD citizen has been trying to save 10% of disposable income at best, it appears prima facie odd that India’s PM claims a savings rate as high as 35% for India or a British politician has claimed a savings rate as high as 44% for China. Something may be wrong in the measurement of the allegedly astronomical savings rates of India and China. The late Professor Nicholas Kaldor himself, after all, suggested it was rich people who saved and poor people who did not for the simple reason the former had something left over to save which the latter did not!

And indeed something is wrong in the measurements. What has happened, I believe, is that there has been a misreading of the vast nominal expansion of bank deposits via deposit-multiplication in the Indian banking system, an expansion that has been caused by explosive deficit finance over the last four or five decades. That vast nominal expansion of bank-deposits has been misread as indicating growth of real savings behaviour instead. I have written and spoken about and shown this quite extensively in the last half dozen years since I first discovered it in the case of India. E.g., in a lecture titled “Can India become an economic superpower or will there be a monetary meltdown?” at Cardiff University’s Institute of Applied Macroeconomics and at London’s Institute of Economic Affairs in April 2005, as well as in May 2005 at a monetary economics seminar invited at the RBI by Dr Narendra Jadav. The same may be true of China though I have looked at it much less.

How I described this phenomenon in a 2007 article in The Statesman is this:

“Savings is indeed normally measured by adding financial and non-financial savings. Financial savings include bank-deposits. But India is not a normal country in this. Nor is China. Both have seen massive exponential growth of bank-deposits in the last few decades. Does this mean Indians and Chinese are saving phenomenally high fractions of their incomes by assiduously putting money away into their shaky nationalized banks? Sadly, it does not. What has happened is government deficit-financing has grown explosively in both countries over decades. In a “fractional reserve” banking system (i.e. a system where your bank does not keep the money you deposited there but lends out almost all of it immediately), government expenditure causes bank-lending, and bank-lending causes bank-deposits to expand. Yes there has been massive expansion of bank-deposits in India but it is a nominal paper phenomenon and does not signify superhuman savings behaviour. Indians keep their assets mostly in metals, land, property, cattle, etc., and as cash, not as bank deposits.”

An article of mine in 2008 in Business Standard put it like this:

“India has followed in peacetime over six decades what the US and Britain followed during war. Our vast growth of bank deposits in recent decades has been mostly a paper (or nominal) phenomenon caused by unlimited deficit finance in a fractional reserve banking system. Policy makers have widely misinterpreted it as indicating a real phenomenon of incredibly high savings behaviour. In an inflationary environment, people save their wealth less as paper deposits than as real assets like land, cattle, buildings, machinery, food stocks, jewellery etc.”

If you asked me “What then is India’s real savings rate?” I have little answer to give except to say I know what it is not – it is not what the Government of India says it is. It is certainly unlikely to be anywhere near the 35% you stated it to be in your June 9 2009 Lok Sabha statement. If the OECD’s real savings rate has been something like 10% out of disposable income, I might accept India’s is, say, 15% at a maximum when properly measured – far from the 35% being claimed. What I believe may have been mismeasured by you and Meghnad Desai and many others as indicating high real savings is actually the nominal or paper expansion of bank-deposits in a fractional reserve banking system induced by runaway government deficit-spending in both India and China over the last several decades.

5. Technological progress and the mainsprings of real economic growth

So much for the g and s variables in the s/k = g equation in your economic model. But the assumed constant k is a big problem too!

During the 1989 perestroika-for-India project-conference, Professor Friedman referred to his 1955 experience in India and said this about the assumption of a constant k:

“I think there was an enormously important point… That was the almost universal acceptance at that time of the view that there was a sort of technologically fixed capital output ratio. That if you wanted to develop, you just had to figure out how much capital you needed, used as a statistical technological capital output ratio, and by God the next day you could immediately tell what output you were going to achieve. That was a large part of the motivation behind some of the measures that were taken then.”

The crucial problem of the sort of growth-model from which your formulation relating savings to growth arises is that, with a constant k, you have necessarily neglected the real source of economic growth, which is technological progress!

I said in the 2007 article referred to above:

“Economic growth in India as elsewhere arises not because of what politicians and bureaucrats do in capital cities, but because of spontaneous technological progress, improved productivity and learning-by-doing on part of the general population. Technological progress is a very general notion, and applies to any and every production activity or commercial transaction that now can be accomplished more easily or using fewer inputs than before.”

In “Growth and Government Delusion” published in The Statesman last year, I described the growth process more fully like this:

“The mainsprings of real growth in the wealth of the individual, and so of the nation, are greater practical learning, increases in capital resources and improvements in technology. Deeper skills and improved dexterity cause output produced with fewer inputs than before, i.e. greater productivity. Adam Smith said there is “invention of a great number of machines which facilitate and abridge labour, and enable one man to do the work of many”. Consider a real life example. A fresh engineering graduate knows dynamometers are needed in testing and performance-certification of diesel engines. He strips open a meter, finds out how it works, asks engine manufacturers what design improvements they want to see, whether they will buy from him if he can make the improvement. He finds out prices and properties of machine tools needed and wages paid currently to skilled labour, calculates expected revenues and costs, and finally tries to persuade a bank of his production plans, promising to repay loans from his returns. Overcoming restrictions of religion or caste, the secular agent is spurred by expectation of future gains to approach various others with offers of contract, and so organize their efforts into one. If all his offers ~ to creditors, labour, suppliers ~ are accepted he is, for the moment, in business. He may not be for long ~ but if he succeeds his actions will have caused an improvement in design of dynamometers and a reduction in the cost of diesel engines, as well as an increase in the economy’s produced means of production (its capital stock) and in the value of contracts made. His creditors are more confident of his ability to repay, his buyers of his product quality, he himself knows more of his workers’ skills, etc. If these people enter a second and then a third and fourth set of contracts, the increase in mutual trust in coming to agreement will quickly decline in relation to the increased output of capital goods. The first source of increasing returns to scale in production, and hence the mainspring of real economic growth, arises from the successful completion of exchange. Transforming inputs into outputs necessarily takes time, and it is for that time the innovator or entrepreneur or “capitalist” or “adventurer” must persuade his creditors to trust him, whether bankers who have lent him capital or workers who have lent him labour. The essence of the enterprise (or “firm”) he tries to get underway consists of no more than the set of contracts he has entered into with the various others, his position being unique because he is the only one to know who all the others happen to be at the same time. In terms introduced by Professor Frank Hahn, the entrepreneur transforms himself from being “anonymous” to being “named” in the eyes of others, while also finding out qualities attaching to the names of those encountered in commerce. Profits earned are partly a measure of the entrepreneur’s success in this simultaneous process of discovery and advertisement. Another potential entrepreneur, fresh from engineering college, may soon pursue the pioneer’s success and start displacing his product in the market ~ eventually chasers become pioneers and then get chased themselves, and a process of dynamic competition would be underway. As it unfolds, anonymous and obscure graduates from engineering colleges become by dint of their efforts and a little luck, named and reputable firms and perhaps founders of industrial families. Multiply this simple story many times, with a few million different entrepreneurs and hundreds of thousands of different goods and services, and we shall be witnessing India’s actual Industrial Revolution, not the fake promise of it from self-seeking politicians and bureaucrats.”

Technological progress in a myriad of ways and discovery of new resources are important factors contributing to India’s growth today. But while India’s “real” economy does well, the “nominal” paper-money economy controlled by Government does not. Continuous deficit financing for half a century has led to exponential growth of public debt and broad money, and, as noted, the vast growth of nominal bank-deposits has been misinterpreted as indicating unusually high real savings behaviour when it in fact may just signal vast amounts of government debt being held by our nationalised banks. These bank assets may be liquid domestically but are illiquid internationally since our government debt is not held by domestic households as voluntary savings nor has it been a liquid asset held worldwide in foreign portfolios.

What politicians of all parties, especially your own and the BJP and CPI-M since they are the three largest, have been presiding over is exponential growth of our paper money supply, which has even reached 22% per annum. Parliament and the Government should be taking honest responsibility for this because it may certainly portend double-digit inflation (i.e., decline in the value of paper-money) perhaps as high as 14%-15% per annum, something that is certain to affect the aam admi’s economic welfare adversely.

6. Selling Government assets to Big Business is a bad idea in a potentially hyperinflationary economy

Respected PradhanMantriji, the record would show that I, and really I alone, 25 years ago, may have been the first among Indian economists to advocate the privatisation of the public sector. (Viz, “Silver Jubilee of Pricing, Planning and Politics: A Study of Economic Distortions in India”.) In spite of this, I have to say clearly now that in present circumstances of a potentially hyperinflationary economy created by your Government and its predecessors, I believe your Government’s present plans to sell Government assets may be an exceptionally unwise and imprudent idea. The reasoning is very simple from within monetary economics.

Government every year has produced paper rupees and bank deposits in practically unlimited amounts to pay for its practically unlimited deficit financing, and it has behaved thus over decades. Such has been the nature of the macroeconomic process that all Indian political parties have been part of, whether they are aware of it or not.

Indian Big Business has an acute sense of this long-term nominal/paper expansion of India’s economy, and acts towards converting wherever possible its own hoards of paper rupees and rupee-denominated assets into more valuable portfolios for itself of real or durable assets, most conspicuously including hard-currency denominated assets, farm-land and urban real-estate, and, now, the physical assets of the Indian public sector. Such a path of trying to transform local domestic paper assets – produced unlimitedly by Government monetary and fiscal policy and naturally destined to depreciate — into real durable assets, is a privately rational course of action to follow in an inflationary economy. It is not rocket-science to realise the long-term path of rupee-denominated assets is downwards in comparison to the hard-currencies of the world – just compare our money supply growth and inflation rates with those of the rest of the world.

The Statesman of November 16 2006 had a lead editorial titled Government’s land-fraud: Cheating peasants in a hyperinflation-prone economy which said:

“There is something fundamentally dishonourable about the way the Centre, the state of West Bengal and other state governments are treating the issue of expropriating peasants, farm-workers, petty shop-keepers etc of their small plots of land in the interests of promoters, industrialists and other businessmen. Singur may be but one example of a phenomenon being seen all over the country: Hyderabad, Karnataka, Kerala, Haryana, everywhere. So-called “Special Economic Zones” will merely exacerbate the problem many times over. India and its governments do not belong only to business and industrial lobbies, and what is good for private industrialists may or may not be good for India’s people as a whole. Economic development does not necessarily come to be defined by a few factories or high-rise housing complexes being built here or there on land that has been taken over by the Government, paying paper-money compensation to existing stakeholders, and then resold to promoters or industrialists backed by powerful political interest-groups on a promise that a few thousand new jobs will be created. One fundamental problem has to do with inadequate systems of land-description and definition, implementation and recording of property rights. An equally fundamental problem has to do with fair valuation of land owned by peasants etc. in terms of an inconvertible paper-money. Every serious economist knows that “land” is defined as that specific factor of production and real asset whose supply is fixed and does not increase in response to its price. Every serious economist also knows that paper-money is that nominal asset whose price can be made to catastrophically decline by a massive increase in its supply, i.e. by Government printing more of the paper it holds a monopoly to print. For Government to compensate people with paper-money it prints itself by valuing their land on the basis of an average of the price of the last few years, is for Government to cheat them of the fair present-value of the land. That present-value of land must be calculated in the way the present-value of any asset comes to be calculated, namely, by summing the likely discounted cash-flows of future values. And those future values should account for the likelihood of a massive future inflation causing decline in the value of paper-money in view of the fact we in India have a domestic public debt of some Rs. 30 trillion (Rs. 30 lakh crore) and counting, and money supply growth rates averaging 16-17% per annum. In fact, a responsible Government would, given the inconvertible nature of the rupee, have used foreign exchange or gold as the unit of account in calculating future-values of the land. India’s peasants are probably being cheated by their Government of real assets whose value is expected to rise, receiving nominal paper assets in compensation whose value is expected to fall.”

Shortly afterwards the Hon’ble MP for Kolkata Dakshin, Km Mamata Banerjee, started her protest fast, riveting the nation’s attention in the winter of 2006-2007. What goes for government buying land on behalf of its businessman friends also goes, mutatis mutandis, for the public sector’s real assets being bought up by the private sector using domestic paper money in a potentially hyperinflationary economy. If your new Government wishes to see real assets of the public sector being sold for paper money, let it seek to value these assets not in inconvertible rupees that Government itself has been producing in unlimited quantities but perhaps in forex or gold-units instead!

In the 2004-2005 volume Margaret Thatcher’s Revolution: How it Happened and What it Meant, edited by myself and Professor John Clarke, there is a chapter by Professor Patrick Minford on Margaret Thatcher’s fiscal and monetary policy (macroeconomics) that was placed ahead of the chapter by Professor Martin Ricketts on Margaret Thatcher’s privatisation (microeconomics). India’s fiscal and monetary or macroeconomic problems are far worse today than Britain’s were when Margaret Thatcher came to power. We need to get our macroeconomic problems sorted before we attempt the microeconomic privatisation of public assets.

It is wonderful that your young party colleague, the Hon’ble MP from Amethi, Shri Rahul Gandhi, has declined to join the present Government and instead wishes to reflect further on the “common man” and “common woman” about whom I had described his late father talking to me on September 18 1990. Certainly the aam admi is not someone to be found among India’s lobbyists of organised Big Business or organised Big Labour who have tended to control government agendas from the big cities.

With my warmest personal regards and respect, I remain,

Cordially yours

Subroto Roy, PhD (Cantab.), BScEcon (London)

see also https://independentindian.com/thoughts-words-deeds-my-work-1973-2010/rajiv-gandhi-and-the-origins-of-indias-1991-economic-reform/did-jagdish-bhagwati-originate-pioneer-intellectually-father-indias-1991-economic-reform-did-manmohan-singh-or-did-i-through-my-e/

China’s India Example: Tibet, Xinjiang May Not Be Assimilated Like Inner Mongolia, Manchuria (2008)

March 25, 2008 — drsubrotoroyNote: My articles on related subjects recently published in The Statesman include “Understanding China”, “China’s India Aggression”, “China’s Commonwealth”, “Nixon & Mao vs India”, “Lessons from the 1962 War”, “China’s force & diplomacy” etc https://independentindian.com/2009/09/19/my-ten-articles-on-china-tibet-xinjiang-taiwan-in-relation-to-india/

China’s India Example: Tibet, Xinjiang May Not Be Assimilated Like Inner Mongolia And Manchuria

by

Subroto Roy

First published in The Statesman, Editorial Page Special Article March 25, 2008

Zhang Qingli, Tibet’s current Communist Party boss, reportedly said last year, “The Communist Party is like the parent (father and mother) of the Tibetans. The Party is the real boddhisatva of the Tibetans.” Before communism, China’s people followed three non-theistic religious cultures, Buddhism, Confucianism and Taoism, choosing whichever aspects of each they wished to see in their daily lives. Animosity towards the theism of Muslims and Christians predates the 1911 revolution. Count Witte, Russia’s top diplomatist in Czarist times, reported the wild contempt towards Islam and wholly unprovoked insult of the Emir of Bokhara by Li Hung Chang, Imperial China’s eminent Ambassador to Moscow, normally the epitome of civility and wisdom. In 1900 the slogan of the Boxer Revolts was “Protect the country, destroy the foreigner” and catholic churches and European settlers and priests were specifically targeted. The Communists have not discriminated in repression of religious belief and practice ~ monasteries, mosques, churches have all experienced desecration; monks, ulema, clergymen all expected to subserve the Party and the State.

Chinese nationalism

For Chinese officials to speak of “life and death” struggle against the Dalai Lama sitting in Dharamsala is astounding; if they are serious, it signals a deep long-term insecurity felt in Beijing. How can enormous, wealthy, strong China feel any existential threat at all from unarmed poor Tibetans riding on ponies? Is an Israeli tank-commander intimidated by stone-throwing Palestinian boys? How is it China (even a China where the Party assumes it always knows best), is psychologically defensive and unsure of itself at every turn?

The Chinese in their long history have not been a violent martial people ~ disorganized and apolitical traders and agriculturists and highly civilised artisans and scholars more than fierce warriors fighting from horseback. Like Hindus, they were far more numerous than their more aggressive warlike invading rulers. Before the 20th Century, China was dominated by Manchu Tartars and Mongol Tartars from the Northeast and Northwest ~ the Manchus forcing humiliation upon Chinese men by compelling shaved heads with pigtails. Similar Tartar hordes ruled Russia for centuries and Stalin himself, according to his biographer, might have felt Russia buffered Europe from the Tartars.

Chinese nationalism arose only in the 20th Century, first under the Christian influence of Sun Yatsen and his brother-in-law Chiang Kaishek, later under the atheism of Mao Zedong and his admiring friends, most recently Deng Xiaoping and successors. “Socialism with Chinese characteristics” is the slogan of the present Communist Party but a more realistic slogan of what Mao and friends came to represent in their last decades may be “Chinese nationalism with socialist characteristics”. Taiwan and to lesser extent Singapore and Hong Kong represent “Chinese nationalism with capitalist characteristics”. Western observers, keen always to know the safety of their Chinese investments, have focused on China’s economics, whether the regime is capitalist or socialist and to what extent ~ Indians and other Asians may be keener to identify, and indeed help the Chinese themselves to identify better, the evolving nature of Chinese nationalism and the healthy or unhealthy courses this may now take.

Just as Czarist and Soviet Russia attempted Russification in Finland, the Baltics, Poland, Ukraine etc., Imperial and Maoist China attempted “Sinification” in Manchuria and Inner Mongolia as well as Tibet and Xinjiang (Sinkiang, East Turkestan). Russification succeeded partially but backfired in general. Similarly, Sinification succeeded naturally in Manchuria and without much difficulty in Inner Mongolia. But it has backfired and backfired very badly in Tibet and Xinjiang, and may be expected to do so always.

In India, our soft state and indolent corrupt apparatus of political parties constitute nothing like the organized aggressive war-machine that China has tried to make of its state apparatus, and we have much more freedom of all sorts. India does not prohibit or control peasant farmers or agricultural labourers from migrating to or visiting large metropolitan cities; villagers are as free as anyone else to clog up all city life in India with the occasional political rally ~ in fact India probably may not even know how to ban, suppress or repress most of the things Communist China does.

Hindu traditions were such that as long as you did not preach sedition against the king, you could believe anything ~ including saying, like the Carvaka, that hedonism and materialism were good, spiritualism was bunkum and the priestly class were a bunch of crooks and idiots. Muslim and British rulers in India were not too different ~ yes the Muslims did convert millions by offering the old choice of death or conversion to vanquished people, and there were evil rulers among them but also great and tolerant ones like Zainulabidin of Kashmir and Akbar who followed his example.

India’s basic political ethos has remained that unless you preach sedition, you can basically say or believe anything (no matter how irrational) and also pretty much do whatever you please without being bothered too much by government officials. Pakistan’s attempts to impose Urdu on Bengali-speakers led to civil war and secession; North India’s attempts to impose Hindi on the South led to some language riots and then the three-language formula ~ Hindi spreading across India through Bollywood movies instead.

China proudly says it is not as if there are no declared non-Communists living freely in Beijing, Shanghai etc, pointing out distinguished individual academics and other professionals including government ministers who are liberals, social democrats or even Kuomintang Nationalists. There are tiny state-approved non-Communist political parties in China, some of whose members even may be in positions of influence. It is just that such (token) parties must accept the monopoly and dictatorship of the Communists and are not entitled to take state power. The only religion you are freely allowed to indulge in is the ideology of the State, as that comes to be defined or mis-defined at any time by the Communist Party’s rather sclerotic leadership processes.

Chinese passports

During China’s Civil War, the Communists apparently had promised Tibet and Xinjiang a federation of republics ~ Mao later reneged on this and introduced his notion of “autonomous” regions, provinces and districts. The current crisis in Tibet reveals that the notion of autonomy has been a complete farce. Instead of condemning the Dalai Lama and repressing his followers, a modern self-confident China can so easily resolve matters by allowing a Dalai Lama political party to function freely and responsibly, first perhaps just for Lhasa’s municipal elections and gradually in all of Tibet. Such a party and the Tibet Communist Party would be adequate for a two-party system to arise. The Dalai Lama and other Tibetan exiles also have a natural right to be issued Chinese passports enabling them to return to Tibet~ and their right to return is surely as strong as that of any Han or Hui who have been induced to migrate to Tibet from Mainland China. Such could be the very simple model of genuine autonomy for Tibet and Xinjiang whose native people clearly do not wish to be assimilated in the same way as Inner Mongolia and Manchuria. India’s federal examples, including the three-language formula, may be helpful. Once Mainland China successfully allows genuine autonomy and free societies to arise in Tibet and Xinjiang, the road to reconciliation with Taiwan would also have been opened.

Growth & Government Delusion (2008)

February 22, 2008 — drsubrotoroyGrowth & Government Delusion:

Progress Comes From Learning, Enterprise, Exchange, Not The Parasitic State

By Subroto Roy

First published in The Statesman, Editorial Page Special Article,

February 22, 2008

P Chidambaram, Montek Ahluwalia and Manmohan Singh, like their BJP predecessors, delude themselves and the country as a whole when they claim responsibility for phenomenal economic growth taking place. “My goal is to continue to maintain growth but at the same time the government reserves the right to make rapid adjustments depending upon the evolving international situation” is a typical piece of nonsensical waffle.

Honest Finance Ministers in any country cannot take personal responsibility for rates of economic growth nor is any government in the world nimble, well-informed and intelligent enough to respond to exogenous shocks in a timely manner. The UPA and NDA blaming one another for low growth or taking credit for high growth merely reveal the crude mis-education of their pretentious TV economists. There are far too many measurement and data problems as well as lead-and-lag problems for any credibility to attach to what is said.

Per capita real GDP

Indian businessmen and their politician/ bureaucratic friends seem to think “growth” refers to nominal earnings before tax for the corporate sector, or some such number that can be sold to visiting foreigners to induce them to park their money in India: “You will get a 10 per cent return if you invest in India” to which the visitor says “Oh that must mean India has 10 per cent growth going on”. Of such nonsense are expensive Davos and Delhi conferences made.

What is supposed to be measured when we speak of economic growth? It is annual growth of per capita inflation-adjusted Gross Domestic Product (National Income or Net National Product would be better if available). West Germany and Japan had the highest annual per capita real GDP growth-rates in the world starting from devastated post-War initial conditions. What were their rates? West Germany: 6.6 per cent in 1950-1960, falling to 3.5 per cent by 1960-1970, and 2.4 per cent by 1970-1978. Japan: 6.8 per cent in 1952-1960; 9.4 per cent in 1960-1970, 3.8 per cent in 1970-1978. Thus, only Japan in the 1960s measured more than 9 per cent annual growth of real per capita GDP.

Now India and China are said to be achieving 9 per cent plus routinely. Perhaps we are observing an incredible phenomenon of world economic history. Or perhaps we are just being fed something incredible, some humbug. India’s population is growing at 2 per cent so even if the Government’s number of 9 per cent is taken at face-value, we have to subtract 2 per cent population growth to get per capita figures. Typical official fallacies include thinking clever bureaucratic use of astronomically high savings rates causes growth. For example, Meghnad Desai of Britain’s Labour Party says: “China now has 10.4 per cent growth on a 44 per cent savings rate… ” Indian savings have been alleged near 32 per cent. What has been mismeasured as high savings is actually paper expansion of bank-deposits in a fractional reserve banking system induced by runaway government deficit-spending in both countries.

Real economic growth arises from spontaneous technological progress, improved productivity and learning-by-doing of the general population. World economic history suggests growth occurs in spite of, rather than due to, behaviour of an often parasitic State. Technological progress in a myriad of ways and discovery of new resources are important factors contributing to India’s growth today. But while the “real” economy does well, the “nominal” paper-money economy controlled by Government does not.

Continuous deficit financing for half a century has led to exponential growth of public debt and broad money. The vast growth of bank-deposits has been misinterpreted as indicating unusual savings behaviour when it in fact signals vast government debt being held by nationalised banks. What Messrs Chidambaram, Ahluwalia,Manmohan Singh, the BJP et al have been presiding over is annual paper-money supply growth of 22 per cent! That is what they should be taking honest responsibility for because it certainly implies double-digit inflation (i.e. decline in the value of paper-money) perhaps as high as 14 or 15 per cent. If you believe Government numbers that inflationis near 5 per cent you may believe anything.

The mainsprings of real growth in the wealth of the individual, and so of the nation, are greater practical learning, increases in capital resources and improvements in technology. Deeper skills and improved dexterity cause output produced with fewer inputs than before, i.e. greater productivity. Adam Smith said there is “invention of a great number of machines which facilitate and abridge labour, and enable one man to do the work of many”.

Consider a real life example. A fresh engineering graduate knows dynamometers are needed in testing and performance-certification of diesel engines. He strips open a meter, finds out how it works, asks engine manufacturers what design improvements they want to see, whether they will buy from him if he can make the improvement. He finds out prices and properties of machine tools needed and wages paid currently to skilled labour, calculates expected revenues and costs, and finally tries to persuade a bank of his production plans, promising to repay loans from his returns.

Overcoming restrictions of religion or caste, the secular agent is spurred by expectation of future gains to approach various others with offers of contract, and so organize their efforts into one. If all his offers ~ to creditors, labour, suppliers ~ are accepted he is, for the moment, in business. He may not be for long ~ but if he succeeds his actions will have caused an improvement in design of dynamometers and a reduction in the cost of diesel engines, as well as an increase in the economy’s produced means of production (its capital stock) and in the value of contracts made. His creditors are more confident of his ability to repay, his buyers of his product quality, he himself knows more of his workers’ skills, etc. If these people enter a second and then a third and fourth set of contracts, the increase in mutual trust in coming to agreement will quickly decline in relation to the increased output of capital goods. The first source of increasing returns to scale in production, and hence the mainspring of real economic growth, arises from the successful completion of exchange.

Risk and enterprise

Transforming inputs into outputs necessarily takes time, and it is for that time the innovator or entrepreneur or “capitalist” or “adventurer” must persuade his creditors to trust him, whether bankers who have lent him capital or workers who have lent him labour. The essence of the enterprise (or “firm”) he tries to get underway consists of no more than the set of contracts he has entered into with the various others, his position being unique because he is the only one to know who all the others happen to be at the same time. In terms introduced by Professor Frank Hahn, the entrepreneur transforms himself from being “anonymous” to being “named” in the eyes of others, while also finding out qualities attaching to the names of those encountered in commerce.

Profits earned are partly a measure of the entrepreneur’s success in this simultaneous process of discovery and advertisement. Another potential entrepreneur, fresh from engineering college, may soon pursue the pioneer’s success and start displacing his product in the market ~ eventually chasers become pioneers and then get chased themselves, and a process of dynamic competition would be underway. As it unfolds, anonymous and obscure graduates from engineering colleges become by dint of their efforts and a little luck, named and reputable firms and perhaps founders of industrial families. Multiply this simple story many times, with a few million different entrepreneurs and hundreds of thousands of different goods and services, and we shall be witnessing India’s actual Industrial Revolution, not the fake promise of it from self-seeking politicians and bureaucrats.

see also 12 June 2009

China’s Commonwealth: Freedom is the Road to Resolving Taiwan, Tibet, Sinkiang (2007) (plus a link to a Mandarin translation)

December 17, 2007 — drsubrotoroyChina’s Commonwealth

Freedom is the Road to Resolving Taiwan, Tibet, Sinkiang

by

Subroto Roy

First published in The Statesman, December 17, 2007

Editorial Page special article

Mandarin translation: https://twishort.com/Bd7nc

War between China and Taiwan would lead to nothing but disaster all around. Everyone recognises this yet China’s military and political establishment threaten it sporadically when provoked by Taiwan’s leaders, and both sides continue to arm heavily and plan for such a contingency. China’s military is mostly congregated in its North West, North, East and South East with between one third and one half of its total forces facing Taiwan alone in an aggressive posture for an amphibious invasion. Taiwan faces 900 Chinese missiles targeted at it. China’s South West has been left relatively unguarded as no threat has been perceived from India or the Tibetans in fifty years.

Cross-strait relations

The 23 million people of Taiwan have made themselves relatively secure across the 100 miles of sea that separate them from the Mainland. A sea-borne Communist invasion following a heavy missile barrage and blockade would undoubtedly leave the Taiwanese badly bruised and bleeding. But there is enough experience from World War II to suggest that trying to invade and occupy islands turns out as badly for the invader as it does for the defender. The Taiwanese military are confident they may be able to defeat an attempted invasion after two or three weeks of fierce fighting even if their promised American ally fails to materialize by their side.

In any case, for China to succeed in forcibly establishing its rule someday over Taiwan would be a pyrrhic victory, since it would lead to tremendous political and economic costs upon all Chinese people. Gaining control after a terrible war would rule out the Hong Kong “One Country Two Systems” model, with nominal Chinese sovereignty being established over an otherwise unchanged Taiwan. Instead the Chinese would have to institute a highly repressive political system, which will incorrigibly damage Taiwan’s flourishing technologically advanced economy, as well as lead to drastic irreparable political and economic retrogression on the Mainland.

Political repression will lead backwards again to the long-gone era of Mao-Zhou communism, displacing the glacial positive trends seen since Deng Xiaoping. Foreign confidence and investment would vanish, boycotts may cause China to lose lucrative and hard-earned new markets in the USA, Europe and Asia, as the world recoiled from the bloodshed to wait to see what the new repression led up to. The Chinese Communist Party (CPC), tiny as it is in size compared to China’s vast population, would become much weakened and lose whatever little confidence it has among an increasingly modern- minded and aware Chinese public. Occupying Taiwan in the 21st Century will not be a tea-party.

The alternative to war is “peaceful reunification” which is the official policy of the CPC, and which also has been a major plank of United States foreign policy since the time of George C Marshall. Unlike Britain, Japan, Russia, France, Germany, even Sweden and Belgium, the Americans were not among the 19th Century powers that exploited China, and that is something that has left some residual goodwill, implicit as it may be, since all Chinese despise the fact their country was humiliated by greedy foreign powers in the past. The USA has subscribed to “One China” and peaceful unification even after its cynical near-betrayal of Taiwan since 1972, having normal diplomatic and trade relations with Communist China while agreeing to help Taiwan if the Communists attempted a military invasion.

Communist China’s strategy towards peaceful reunification with Taiwan has been unlimited allurement: offer Taiwanese businessmen a free hand in investing in China, offer Taiwan students places in Mainland universities, offer Taiwanese airlines flying rights etc. The Taiwanese see their giant ominous neighbour offering such allurements on one hand and threatening a missile attack and invasion and occupation on the other, as if they are animals who will respond to the carrots and sticks of behaviourism.

Taiwan in recent decades has seen its own history and future much more clearly than it sees the Communists being able to see theirs. A marriage can hardly occur or be stable when the self-knowledge of one party greatly exceeds the self-knowledge of the other. It is thus no wonder that the Taiwan-China talks get stalled or retrogress, as the root problem has failed to be addressed which has to do with the political legitimacy of a combined regime.

Political China consisted historically of the agricultural plains and river-valleys of “China Proper” and the arid sparsely populated mountainous periphery of Inner Mongolia, Tibet and Sinkiang. The native people of Formosa (Taiwan) had their own unique character distinct from the Mainland until 1949 when Chiang Kaishek’s Kuomintang moved there after being defeated by Mao Zedong’s Communists.

Today the Hong Kong Model of “One Country Two Systems” can be generalized to “One Commonwealth/ Confederation of China, Six Systems”, whose constituents would be Mainland China, Chinese Taipei (Taiwan), Chinese Hong Kong, Tibet, Sinkiang and Inner Mongolia. A difference between a commonwealth and a confederation is that a commonwealth permits different heads of state whereas a confederation would have one head of state, who, in view of Mainland China’s predominance, could be agreed upon to be from there permanently.

Taiwan is the key to the peaceful creation of such a Chinese commonwealth or confederation, and Taiwan may certainly agree to “reunification” on such a pattern on one key condition ~ the abolition of totalitarian Communist one-party rule on the Mainland.

The CPC’s parent party was the Russian Social Democratic Labour Party which became the Bolshevik Party which became the All-Union Communist Party in 1925. This still exists today but to its great credit it agreed sixteen years ago, more or less voluntarily, to abandon totalitarian power and bring in constitutional democracy in the former USSR. East European Communist Parties did the same, mostly transforming themselves back to becoming Social Democrat or Labour Parties ~ so much so that Germany’s present elected head of government is a former East German.

Hearts and minds

Mainland China must follow a similar path if it wishes to win the hearts and minds and political loyalties of all Chinese people and form a genuine confederation ~ which means the CPC must lead the way towards its own peaceful dissolution and transformation.

Historically, China’s people followed an admixture of three non-theistic religious cultures, namely, Buddhism, Confucianism and Taoism, individually choosing whichever aspects of each that they wished to see in their daily lives. Lamaist Buddhism governed Tibet and Mongolia and deeply affected parts of Mainland China too. China’s theists include the Uighurs of Sinkiang who were and remain devout Muslims, as well as the many Catholics and other Christians since the first Jesuits arrived five hundred years ago. Sun Yatsen himself was a Christian. Marx, Engels, Stalin, Mao and even Deng have never really been able to substitute as a satisfactory new Chinese pantheon.

A free multi-party democracy in Mainland China, flying the Republican or some combined flag and tracing its origin to the 1911 Revolution, even one in which Communists won legitimate political power through free elections (as has been seen in India’s States), would earn the genuine respect of the world, and be able to confidently lead a new Chinese Confederation. The Chinese people who have been often forced against their will to resettle in Tibet and Sinkiang under the present totalitarian regime would be free to move or stay just as there are many Russians in Ukraine or Kazakhstan today. And of course the Dalai Lama would be able to return home in peace after half a century in exile. Freedom is the road to the peaceful resolution of China’s problems. Let freedom ring.

Hutton and Desai: United in Error

December 14, 2007 — drsubrotoroyHutton and Desai: United in Error

Subroto Roy

In an engaging debate in Prospect Magazine about a year ago, republished at China Digital Times, Will Hutton and Meghnad Desai have made the same cardinal error: they have assumed (like almost everyone else who has considered China’s or India’s recent macroeconomics) that savings rates are some astronomical figure.

Typical official fallacies in both countries include thinking that clever bureaucratic use of such high savings rates can and does cause high growth. In fact, real growth arises not because of what politicians and bureaucrats do but because of spontaneous technological progress, improved productivity and learning-by-doing of the general population ~ mostly despite not because of an exploitative parasitic State.

Here is Hutton on this issue: “China’s economic growth is based on the state channelling vast under-priced savings into huge investment … How much longer can China’s state-owned banks carry on directing billions of dollars of savings into investments that produce tiny or even negative returns…” (italics added)

Here is Desai: “China has achieved rapid growth with a policy of under-consumption and over-saving… China… now has 10.4 per cent growth on a 44 per cent savings rate….” (italics added)

What has been mismeasured as high savings in China and India is actually the expansion of bank-deposits in a fractional reserve banking system induced by runaway government deficit-spending.

On the basis of Indian evidence, I said this in public for the first time at Patrick Minford’s seminar on monetary economics at Cardiff and a week later at the IEA London in the spring of 2005 in a lecture titled “Can India become a superpower or will there be a monetary meltdown?” My recent general articles in The Statesman “The Dream Team: A Critique”, “Fallacious Finance”, “Against Quackery” etc speak a little more of this in the Indian case. What little I have seen of Chinese evidence indicates a similar phenomenon at work.

I said in 2005:”New technological progress in a myriad of ways, as well as the discovery of new resources… are all important factors contributing to real economic growth in India today. While the real side of the economy does well, the “nominal” economy, within the Government’s control, displays disconcerting trends. Continual deficit financing for half a century has led to exponential growth of public debt and broad money. The vast growth of time-deposits in banks may have been misinterpreted as indicating a real phenomenon such as unusual savings behaviour when it is more likely to be a nominal phenomenon resulting from increasing amounts of government debt being held by the largely nationalised banking sector. (The same may be true of China).”

As for growth-rates, before anyone at all waffles on about China’s and India’s allegedly high growth-rates, it is best to bring to mind a little hard evidence from other countries eg Germany and Japan where growth was starting from devastated post-War initial conditions:

West Germany: 6.6% in 1950-1960, falling to 3.5% by 1960-1970, and 2.4% by 1970-1978. Japan: 6.8% in 1952-1960; 9.4% in 1960-1970, 3.8% in 1970-1978.

China and India sustaining 8%, 9%, 10% annual growth of per capita real GDP for years on end? Naaaaah. Or rather, if you believe that, you will believe anything.

see also https://independentindian.com/2009/06/12/mistaken-macroeconomics-an-open-letter-to-prime-minister-dr-manmohan-singh/

Mistaken Macroeconomics: An Open Letter to Prime Minister Dr Manmohan Singh 12 June 2009

Understanding China (2007)

October 22, 2007 — drsubrotoroyUnderstanding China

The World Needs to Ask China to Find Her True Higher Self

by Subroto Roy

First published in The Statesman, October 22, 2007, Editorial Page Special Article

The most important factors explaining China’s progress since the deaths of Mao Zedong and Zhou Enlai have been the spread and quick absorption of modern Western technology under conditions of relative peace and tranquillity. The “capitalist road” came to be taken after all and the once-denounced Liu Shaoqui was posthumously rehabilitated by his shrewd old friend Deng Xiaoping.

To be sure, the new technology itself has combined with democratic hatred felt by young Chinese against the corrupt elitist police-state gerontocracy, and this produced first a Wei Jingsheng and Democracy Wall and later the Tiananmen Square protests. There have been also in recent years many thousands of incidents of peasants resisting State-sponsored brutality, fighting to prevent their lands being stolen in the name of purported capitalist industrialisation, in an economy where, as in India, land is an appreciating asset and the paper-currency remains weak because inflation by money-printing is the basis of public finance. China’s multitudinous domestic tensions continue to boil over as if in a cauldron, and it seems inevitable Chinese Gorbachevs and Yeltsins will one day emerge from within the Communist Party to try to begin the long political march towards multiparty democracy and a free society ~ though of course they may fail too, and China will remain condemned to being a dictatorship of one sort or other for centuries more.

Absence of war

What has been seen in recent decades is the relative absence of war. The last military war the Chinese fought was a month-long battle against fellow-Communist Vietnamese in 1979, after Vietnam had run over and destroyed the Chinese (and Western) backed Khmer Rouge in Cambodia. Before that, fellow-Communists of the USSR were fought in a border war in 1969. Before that was the border-war with India in 1959-1963 and occupation of Tibet 1950-1959.

The really savage, fierce large-scale fighting in 20th Century Chinese history was seen in the Second Sino-Japanese War of 1937-1945, the Civil War of 1945-1949 and the Korean War of 1950-1953. The occupation of Tibet and fighting against India resulting from Tibet’s occupation were really, from a Chinese Communist point of view, merely light follow-ups to those major wars of the Mao-Zhou era, especially fighting the USA and UN in Korea. Peaceful Tibet and naïve non-violent India stood no chance against the aggressive highly experienced Mao-Zhou war-machine at the time.

It may even be that Mao could live only with incessant external tumult ~ after fighting military wars, he orchestrated domestic conflicts in the Little and Great Leap Forward of 1949-1963 and Great Proletarian Cultural Revolution of 1964-1969, all among the failures of a cruel ill-educated man who led his people into social, political and economic disaster from which trauma they have been slowly recovering over the last thirty years.

Today, Communist China’s military is geared to fight the non-Communist Chinese of Taiwan in a continuation of the Civil War. It seems unlikely there will be an actual invasion for the simple reason that Taiwan, though much smaller, may not suffer eventual defeat but instead inflict a mortal wound upon invading forces. Mao succeeded in driving Chiang Kaishek across the Taiwan Straits but it is post-Chiang Taiwan that displays the model of how strong, prosperous, democratic and self-confident Chinese people really can strive to be in the modern world. Everyone agrees Taiwan and China must one day unite ~ the interesting question is whether Taiwan will get absorbed into China or whether China shall take Taiwan as its new model! Just as Liu Shaoqi had the last word over Mao on the question of taking the capitalist road, Chiang Kaishek may yet have the last word over Mao on the best constitutional method for modern China’s governance.

Peculiarly enough, China’s Kuomintang and Communists were both allies of Russian Bolshevism (not unlike India’s Congress Party and Communists). Sun Yatsen’s collaboration with Comintern’s founders began as early as 1921. By 1923 there was a formal agreement and Stalin sent Gruzenberg (alias Borodin) to China as an adviser, while Sun sent many including Chiang to Russia on learning expeditions. “In reorganising the party, we have Soviet Russia as our model, hoping to achieve a real revolutionary success”, said Sun hopefully. But by March 1926, Sun’s successor Chiang, had begun purging Communists from the Kuomintang-Communist alliance; in July 1927 Borodin returned to Russia after failing at reconciliation; and by July 1928 Chiang had unified China under his own leadership, and Moscow had repudiated the Kuomintang and ordered Chinese Communists to revolt, starting the Civil War and instability that invited the vicious Japanese aggression and occupation.

China’s problems today with Taiwan and with Tibet (and hence with India) will not come to be resolved until China looks hard in the mirror and begins to resolve her problems with herself. No major country today possesses a more factually distorted image of its own history, politics and economics than does China since the Communist takeover of 1949. “Protect the country, destroy the foreigner” was the motto of the Boxer revolts in 1900, a natural defensive reaction to the depredations and humiliations that Manchu-dynasty China suffered at the hands of the British, French, Germans, Russians, Japanese etc for more than a century. The Boxer motto seemed to implicitly drive Mao, Deng and his modern successors too ~ hence the “One China” slogan, the condemnation of “splittism” etc. But the ideology that Mao, Liu, Deng et al developed out of Stalin, Lenin and Marx seems base and stupid when it is unsentimentally compared to the great political philosophy and ethics of ancient China, which emerged out of wise men like Mo Tzu, Meng Ko (Mencius) and the greatest genius of them all, K’ung Fu Tzu, Confucius himself, undoubtedly among the few greatest men of world history.

Tibet

India has not been wrong to acknowledge Outer Tibet as being under China’s legal suzerainty nor in encouraging endogenous political reform among our Tibetan cousins. The Anglo-Russian treaty of 1907 undertook that Tibet would not be dealt with except through China, and the Indian Republic has been the legal successor of British India. Lhasa may be legitimately under Beijing as far as international relations goes ~ the more profound question is whether Beijing’s Communists since 1949 have not been themselves less than legitimate, and if so whether they can now transform themselves in the post Mao-Zhou era through good deeds towards greater legitimacy.

The root problem between China and India has not been the Tibet-India border which was almost always a friendly one and never a problem even when it remained imprecise and undefined over centuries. The root problem has been the sheer greed and aggressiveness of Chinese Communists ~ who now demand not merely Aksai Chin but also a minimum of some 2000 sq km of Tawang and Takpa Shiri in Arunachal. The CIA’s 1959 map of the region, which would be acceptable to the USA, UK, Taiwan and the international community in general as depicting the lawful position, shows the Communist Chinese territorial claim to be baseless and Indian position to be justified.

Nehru’s India was naïve to approach the Mao-Zhou Communists with the attitude of ahimsa and a common Buddhism. But Mao-Zhou Communism is dead, and the Deng capitalist road itself has lost its ethical way. What India and the world need to do now is ask China or help guide China to find her true higher self. China’s Tibet problem and hence border-dispute with India would have been solved peacefully by application of the ways of great men like Confucius, Mencius and Mo Tzu, who are and will remain remembered by mankind long after petty cruel modern dictators like Mao, Zhou and Deng have been long forgotten. Why China’s Communist bosses despise Taiwan may be because Taiwan has sought to preserve that memory of China’s true higher self.

see also https://independentindian.com/2009/09/19/my-ten-articles-on-china-tibet-xinjiang-taiwan-in-relation-to-india/

https://www.youtube.com/watch?v=VHUhy9pJyys

Fallacious Finance: Congress, BJP, CPI-M et al may be leading India to hyperinflation (2007)

March 5, 2007 — drsubrotoroyFallacious Finance: Congress, BJP, CPI-M et al may be leading India to hyperinflation

by

Subroto Roy

first published in The Statesman, 5 March 2007

Editorial Page Special Article

It seems the Dream Team of the PM, Finance Minister, Mr. Montek Ahluwalia and their acolytes may take India on a magical mystery tour of economic hallucinations, fantasies and perhaps nightmares. I hasten to add the BJP and CPI-M have nothing better to say, and criticism of the Government or of Mr Chidambaram’s Budget does not at all imply any sympathy for their political adversaries.

It may be best to outline a few of the main fallacies permeating the entire Governing Class in Delhi, and their media and businessman friends:

1. “India’s Savings Rate is near 32%”. This is factual nonsense. Savings is indeed normally measured by adding financial and non-financial savings. Financial savings include bank-deposits. But India is not a normal country in this. Nor is China. Both have seen massive exponential growth of bank-deposits in the last few decades. Does this mean Indians and Chinese are saving phenomenally high fractions of their incomes by assiduously putting money away into their shaky nationalized banks? Sadly, it does not. What has happened is government deficit-financing has grown explosively in both countries over decades. In a “fractional reserve” banking system (i.e. a system where your bank does not keep the money you deposited there but lends out almost all of it immediately), government expenditure causes bank-lending, and bank-lending causes bank-deposits to expand. Yes there has been massive expansion of bank-deposits in India but it is a nominal paper phenomenon and does not signify superhuman savings behaviour. Indians keep their assets mostly in metals, land, property, cattle, etc., and as cash, not as bank deposits.