7 January 2016

3 June 2014

from World Economy & Central Banking Seminar at Facebook

Professor Rajan’s statement “I determine the monetary policy. I say what it is….ultimately the interest rate that is set is set by me” equates Indian monetary policy with the money interest rate; but monetary policy in India has always involved far more than that, namely, the bulk of Indian banking and insurance has been in government hands for decades, all these institutions have been willy-nilly compelled to hold vast stocks of government debt, both Union and State, on their asset-sides…and unlimited unending deficit finance has led to vast expansion of money supply, making it all rather fragile. My “India’s Money” in 2012 might be found useful. http://tinyurl.com/o9dhe8d

11 April 2014

from World Economy & Central Banking Seminar at Facebook

I have to wonder, What is Professor Rajan on about? Growth in an individual country is affected by the world monetary system? Everyone for almost a century has seen it being a real phenomenon affected by other real factors like savings propensities, capital accumulation, learning and productivity changes, innovation, and, broadly, technological progress… A “source country” needs to consult “recipient” countries before it starts or stops Quantitative Easing? Since when? The latter can always match policy such as to be more or less unaffected… unless of course it wants to ride along for free when the going is good and complain loudly when it is not…. Monetary policy may affect the real economy but as a general rule we may expect growth (a real phenomenon) to be affected by other real factors like savings propensities, capital accumulation, learning and productivity changes, innovation, and, broadly, technological progress..

22 September 2013

“Let us remember that the postponement of tapering is only that, a postponement. We must use this time to create a bullet proof national balance sheet and growth agenda, which creates confidence in citizens and investors alike…”

I will say the statement above is the first sensible thing I have heard Dr Rajan utter anywhere, cutting through all the hype…I should also think he may be underestimating the task at hand, so here’s some help as to what needs to be done from my 19 Aug 2013 Mint article “A wand for Raghuram Rajan” and my 3 Dec 2012 Delhi lecture:

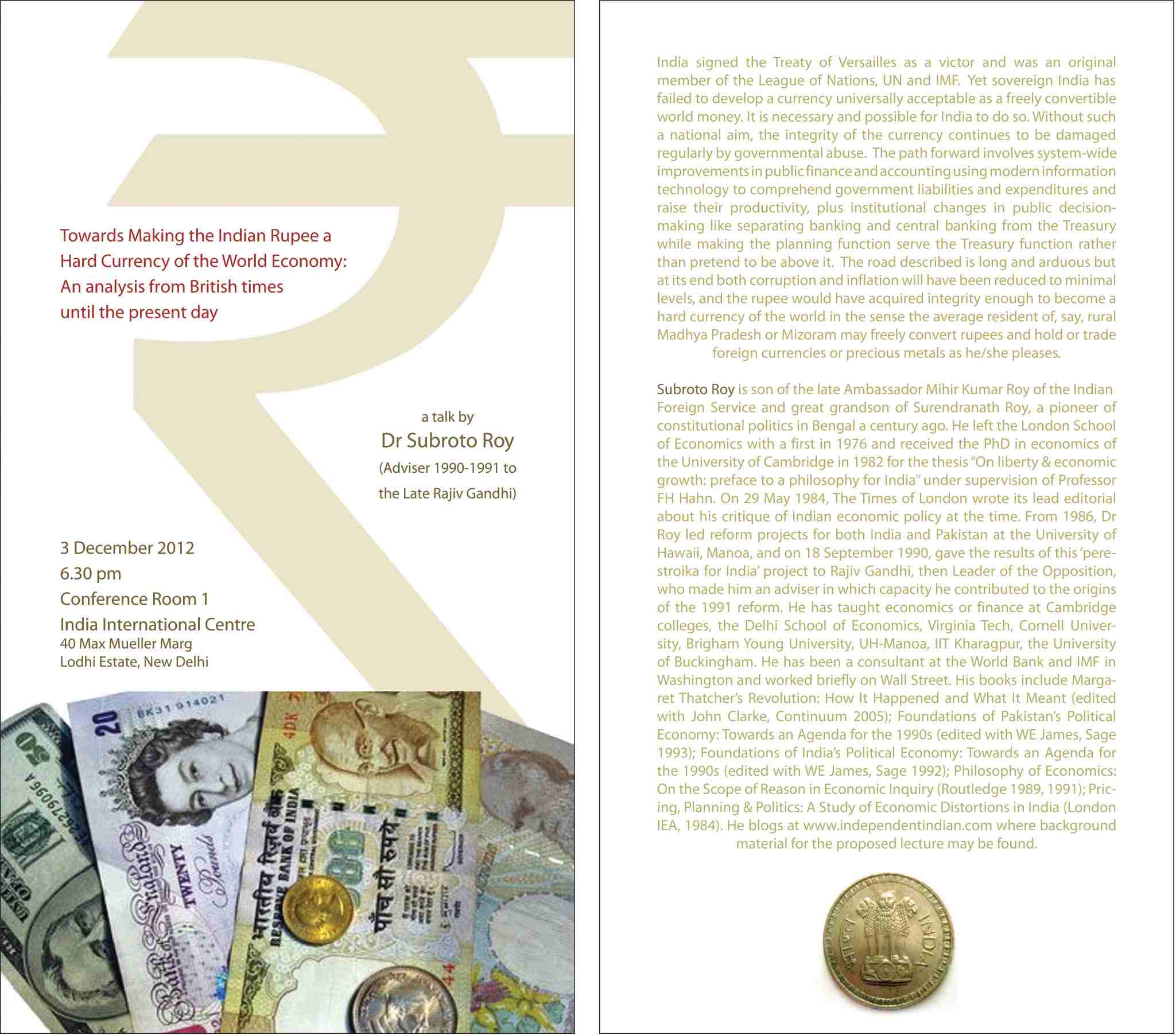

“Rajan has apparently said, “We do not have a magic wand to make the problems disappear instantaneously, but I have absolutely no doubt we will deal with them.” Of course there are no magic wands but there is a scientific path forward. It involves system-wide improvements in public finance and accounting using modern information technology to comprehend government liabilities and expenditures and raise their productivity. It also involves institutional changes in public decision-making like separating banking and central banking from the treasury while making the planning function serve the treasury function rather than pretend to be above it. It is a road long and arduous but at its end both corruption and inflation will have been reduced to minimal levels. The rupee will have acquired sufficient integrity to become a hard currency of the world in the sense the average resident of, say, rural Madhya Pradesh or Mizoram may freely convert rupees and hold or trade foreign currencies or precious metals as he/she pleases. India signed the treaty of Versailles as a victor and was an original member of the League of Nations, the United Nations and the IMF. Yet sovereign India has failed to develop a currency universally acceptable as freely convertible world money. It is necessary and possible for India to aim to do so because without such a national aim, the integrity of the currency continues to be damaged regularly by governmental abuse. An RBI governor’s single overriding goal should be to try to bring a semblance of integrity to India’s money both domestically and worldwide.”

19 August 2013

A wand for Raghuram Rajan

9 August 2013

No magic wand, Professor Rajan? Oh but there is… read up all this over some hours and you will find it… (Of course it’s not from magic really, just hard economic science & politics)

Professor Raghuram Govind Rajan of the University of Chicago Business School deserves everyone’s congratulations on his elevation to the Reserve Bank of India’s Governorship. But I am afraid I cannot share the wild optimism in India’s business media over this. Of course there are several positives to the appointment. First, having a genuine PhD and that too from a top school is a rarity among India’s policy-makers; Rajan earned a 1991 PhD in finance at MIT’s management school for a thesis titled “Essays on banking” (having to do we are told “with the downside to cozy bank-firm relationships”). Secondly, and related, he has not been a career bureaucrat as almost all RBI Governors have been in recent decades. Thirdly, he has been President of the American Finance Association, he won the first Fischer Black prize in finance of that Association, and during Anne Krueger’s 2001-2006 reign as First Deputy MD at the IMF, he was given the research role made well-known by the late Michael Mussa, that of “Economic Counselor” of the IMF.

Hence, altogether, Professor Rajan has come to be well-known over the last decade in the West’s financial media. Given the dismal state of India’s credit in world capital markets, that is an asset for a new RBI Governor to have.

On the negatives, first and foremost, if Professor Rajan has renounced at any time his Indian nationality, surrendered his Indian passport and sworn the naturalization oath of the USA, then he is a US citizen with a US passport and loyalty owed to that country, and by US law he will have to enter the USA using that and no other nationality. If that happens to be the factual case, it will be something that comes out in India’s political cauldron for sure, and there will arise legal issues and court orders barring him from heading the RBI or representing India officially, e.g. when standing in for India’s Finance Minister at the IMF in Washington or the BIS in Basle etc. Was he an Indian national as Economic Counselor at the IMF? The IMF has a tradition of only European MDs and at least one American First Deputy MD. The Economic Counselor was always American too; did Rajan break that by having remained Indian, or conform to it by having become American? It is a simple question of fact which needs to come out clearly. Even if Rajan is an American, he and the Government of India could perhaps try to cite to the Indian courts the new precedent set by the venerable Bank of England which recently appointed a Canadian as Governor.

Secondly, does Professor Rajan know enough (or “have enough domain knowledge” in the modern term) to comprehend let aside confront India’s myriad monetary and public finance problems? Much of his academic experience in the USA and his approach to Western financial markets may be quite simply divorced from the reality of Indian credit markets and India’s peculiar monetary and banking system as these have evolved over decades and centuries. Mathematical finance is a relatively new, small specialised American sub-field of economic theory, and not a part of general economics. Rajan’s academic path of engineering and management in India followed by a finance thesis in the management department of a US engineering school may have exposed him to relatively little formal textbook micro- and macroeconomics, monetary economics, public finance, international economics, economic development etc, especially as these relate to Indian circumstances “Growing up in India, I had seen poverty all around me. I had read about John Maynard Keynes and thought, wow, here’s a guy who managed to have an enormous influence on the world. Economics must be very important.”… He ran across Robert Merton’s paper on rational option pricing, and something clicked that set him on his own intellectual path. “It all came together. You didn’t have these touchy-feely ways of describing human behavior; there were neat arbitrage ways of pricing things. It just seemed so clever and sophisticated,” he said. “And I could use the math skills that I fancied I had, so I decided to get my PhD.”

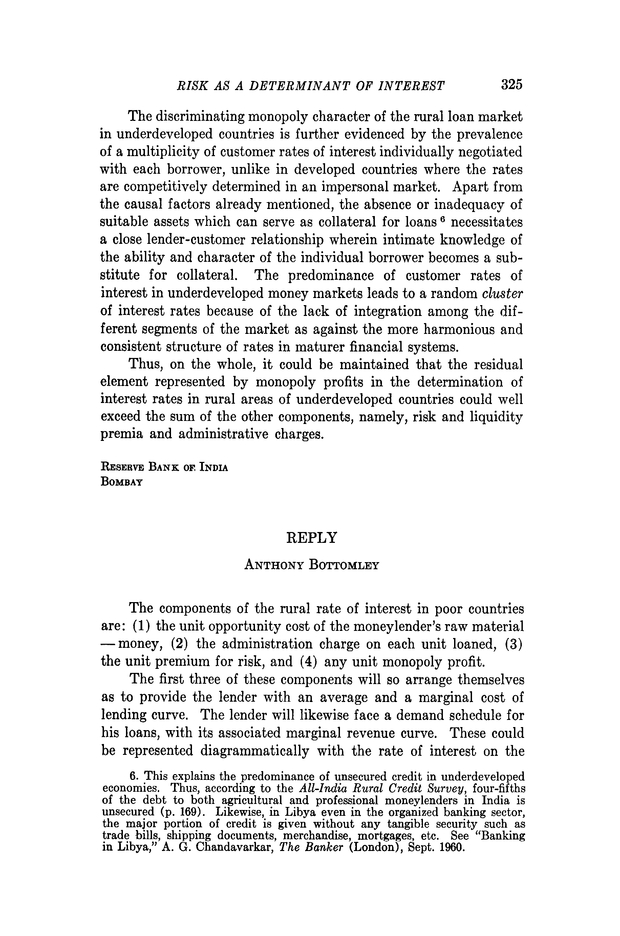

Let me take two examples. Does Rajan realise how the important Bottomley-Chandavarkar debates of the 1960s about India’s rural credit markets influenced George Akerlof’s “Market for Lemons” theory and prompted much work on “asymmetric information”,  signalling etc in credit-markets, insurance-markets, labour-markets and markets in general, as acknowledged in the awards of several Bank of Sweden prizes? Or will he need a tutorial on the facts of rural India’s financial and credit markets, and their relationship with the formal sector? What the Bottomley-Chandavarkar debate referred to half a century ago still continues in rural India insofar as large arbitrage profits are still made by trading across the artificially low rates of money interest caused by financial repression of India’s “formal” monetised sector with its soft inconvertible currency against the very high real rates of return on capital in the “informal” sector. It is obvious to the naked eye that India is a relatively labour-abundant country. It follows the relative price of labour will be low and relative price of capital high compared to, e.g. the Western or Middle Eastern economies, with mobile factors of production like labour and capital expected to flow accordingly across national boundaries. Indian nominal interest-rates in organized credit markets have been for decades tightly controlled, making it necessary to go back to Irving Fisher’s data to obtain benchmark interest-rates, which, as expected, are at least 2%-3% higher in India than in Western capital markets. Joan Robinson once explained “the difference between 30% in an Indian village and 3% in London” saying “side by side with the industrial revolution went great technical progress in the provision of credit and the reduction of lender’s risk.”

signalling etc in credit-markets, insurance-markets, labour-markets and markets in general, as acknowledged in the awards of several Bank of Sweden prizes? Or will he need a tutorial on the facts of rural India’s financial and credit markets, and their relationship with the formal sector? What the Bottomley-Chandavarkar debate referred to half a century ago still continues in rural India insofar as large arbitrage profits are still made by trading across the artificially low rates of money interest caused by financial repression of India’s “formal” monetised sector with its soft inconvertible currency against the very high real rates of return on capital in the “informal” sector. It is obvious to the naked eye that India is a relatively labour-abundant country. It follows the relative price of labour will be low and relative price of capital high compared to, e.g. the Western or Middle Eastern economies, with mobile factors of production like labour and capital expected to flow accordingly across national boundaries. Indian nominal interest-rates in organized credit markets have been for decades tightly controlled, making it necessary to go back to Irving Fisher’s data to obtain benchmark interest-rates, which, as expected, are at least 2%-3% higher in India than in Western capital markets. Joan Robinson once explained “the difference between 30% in an Indian village and 3% in London” saying “side by side with the industrial revolution went great technical progress in the provision of credit and the reduction of lender’s risk.”

What is logically certain is no country can have both relatively low world prices for labour and relatively low world prices for capital! Yet that impossibility seems to have been what India’s purported economic “planners” have planned to engineer! The effect of financial repression over decades may have been to artificially “reverse” or “switch” the risk-premium — making it lucrative for there to be capital flight out of India, with real rates of return on capital within India being made artificially lower than those in world markets! Just as enough export subsidies and tariffs can make a country artificially “reverse” its comparative advantage with its structure of exports and imports becoming inverted, so a labour-rich capital-scarce country may, with enough financial repression, end up causing a capital flight. The Indian elite’s capital flight out of India exporting their adult children and savings overseas may be explained as having been induced by government policy itself.

Secondly, Professor Rajan as a finance and banking specialist, will see at once the import of this graph above that has never been produced let aside comprehended by the RBI, yet which uses the purest RBI data. It shows India’s mostly nationalised banks have decade after decade gotten weaker and weaker financially, being kept afloat by continually pumping in of new “capital” via “recapitalisation” from the government that owns them, using more and more of the soft inconvertible currency that has been debauched merrily by government planners. The nationalised banks with their powerful pampered employee unions, like other powerful pampered employee unions in the government sector, have been the bane of India, where a mere 30 million privileged people in a vast population work with either the government or the organised private sector. The RBI’s own workforce at last count was perhaps 75,000… the largest central bank staff in the world by far!

Will Rajan know how to bring some system out of the institutional chaos that prevails in Indian banking and central banking? If not, he should start with the work of James Hanson “Indian Banking: Market Liberalization and the Pressures for Institutional and Market Framework Reform”, contained in the book created by Anne Krueger who brought him into the IMF, and mentioned in my 2012 article “India’s Money” linked below.

The central question for any 21st century RBI Governor worth the name really becomes whether he or she can stand up to the Finance Ministry and insist that the RBI stop being a mere department of it — even perhaps insisting on constitutional status for its head to fulfill the one over-riding aim of trying to bring a semblance of integrity to India’s currency both domestically and worldwide. Instead it is the so-called “Planning Commission” which has been dominating the Treasury that needs to be made a mere department of the Finance Ministry, while the RBI comes to be hived off to independence!

Professor Rajan has apparently said “We do not have a magic wand to make the problems disappear instantaneously, but I have absolutely no doubt we will deal with them.” Of course there are no magic wands but my 3 December 2012 talk in Delhi has described the right path forward, complex and difficult as this may be.

The path forward involves system-wide improvements in public finance and accounting using modern information technology to comprehend government liabilities and expenditures and raise their productivity, plus institutional changes in public decision-making like separating banking and central banking from the Treasury while making the planning function serve the Treasury function rather than pretend to be above it. The road described is long and arduous but at its end both corruption and inflation will have been reduced to minimal levels, and the rupee would have acquired integrity enough to become a hard currency of the world in the sense the average resident of, say, rural Madhya Pradesh or Mizoram may freely convert rupees and hold or trade foreign currencies or precious metals as he/she pleases.

India signed the Treaty of Versailles as a victor and was an original member of the League of Nations, UN and IMF. Yet sovereign India has failed to develop a currency universally acceptable as a freely convertible world money. It is necessary and possible for India to do so. Without such a national aim, the integrity of the currency continues to be damaged regularly by governmental abuse.

Professor Rajan will not want to be merely an adornment for the GoI in world capital markets for a few years, waiting to get back to his American career and life and perhaps to the IMF again. As RBI Governor, he can find his magic wand if he reads and reflects hard enough using his undoubted academic acumen, and then acts to lead India accordingly. Here is the basic reading list:

“India’s Money” (2012)

“Monetary Integrity and the Rupee” (2008)

“India’s Macroeconomics” (2007)

“Fiscal Instability” (2007)

“Fallacious Finance” (2007)

“Growth and Government Delusion” (2008)

“India in World Trade & Payments” (2007)

“Path of the Indian Rupee 1947-1993” (1993)

“Our Policy Process” (2007)

“Indian Money and Credit” (2006)

“Indian Money and Banking” (2006)

“Growth of Real Income, Money & Prices in India 1869-2004” (2005)

“How to Budget” (2008)

“Waffle but No Models of Monetary Policy: The RBI and Financial Repression (2005)”

“The Dream Team: A Critique” (2006)

“Against Quackery” (2007)

“Mistaken Macroeconomics” (2009)

“The Indian Revolution (2008)”

Some of My Works, Interviews etc on India’s Money, Public Finance, Banking, Trade, BoP, Land, etc (an incomplete list)