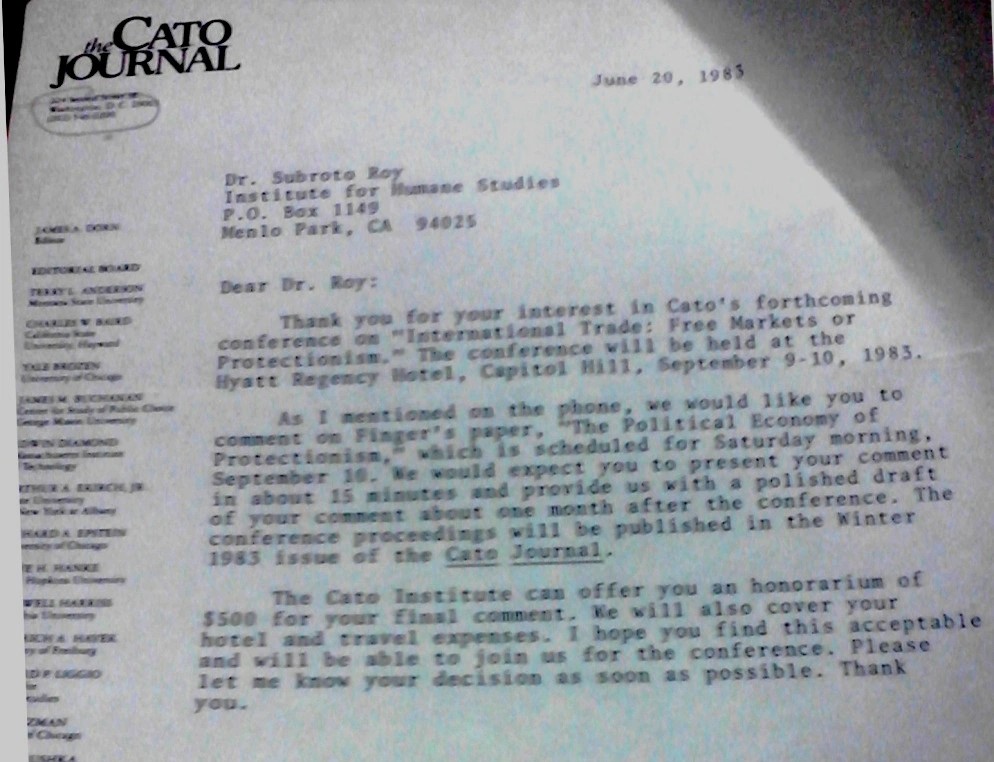

In the summer of 1983 Dr James Dorn of Cato Institute invited me (then in Menlo Park) to comment on the influential papers being given by the prominent trade economist Dr J Michael Finger.

I think I might have said I hadn’t worked on trade since LSE days a decade earlier but Jim said something sweetly persuasive like “We want to put you in the limelight” — and limelight there was, a full house in Washington (the Capitol Hill Hyatt Regency), with the bright camera lights of C-Span and local television.

I do not recall what current trade issues dominated the agenda, certainly it was years before NAFTA or China were being discussed, perhaps tariff removal on US textiles, probably Japanese auto-imports: Michael Finger certainly gave a devastating example of the difficulty US beef exporters had entering Japan’s beef market at the time.

But whatever I said, as a 28 year old Indian from Cambridge and India, was very well received by that packed Washington audience. And I did not say much more than offer a Hahnian-Keynesian scepticism about textbook economic theory being divorced from ground realities.

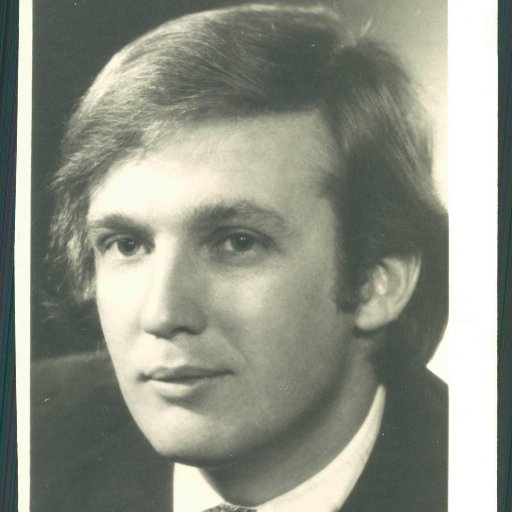

[Twitter 21.10.2016 et seq: I recollect three interactions after the talk, Donald J Trump or someone like him was seated midway in the hall in an aisle, introduced himself praised the talk to me, and may have said “Remember the name”! (He looked like a “preppie”, like myself.) Bernie Sanders, or someone like him made a momentary comment as he charged by at speed; a third man said I “waxed eloquent”. Trump sat toffishly dressed in an aisle seat, congratulated me and introduced himself, Sanders charged out at speed after a momentary word…I recall three interactions after the talk, one each with Trump and Sanders, or someone like them.) I seemed to recall coming from Blacksburg by car to give the Washington talk, but the letter Jim Dorn sent was to Menlo Park, California, where I had been in the summer; and later in Fall 1983 I was visiting at Cornell; I have not yet been able to reconstruct how I travelled to Washington, I would be surprised if I drove from Ithaca and back but perhaps I did. (I had just driven from Blacksburg to California and back, then up to Ithaca).

[I apparently flew from Ithaca to Washington National, then stayed at the hotel for one night, and after my talk (and encounter with the future POTUS Trump), drove to Baltimore airport where I had to pick someone up and drove back to Ithaca in the rented car. The phone conversation about “limelight” must have been in the summer. Oddly enough, I was at Ithaca from Blacksburg teaching History of Economic Thought for a semester in the Economics Department because, from my point of view I could talk to Max Black in Philosophy, and from Cornell’s point of view, Ken Burdett the Economics chair told me, History Department students had demanded the course: those History Department students were led by Ms Ann Coulter, who became a quite quiet pupil in my class.]

Half a dozen years later at the University of Hawaii in March 1989 I amplified the argument a little bit as follows:

“Risk-aversion explains resistance to freer trade (and explains protectionism during a recession)

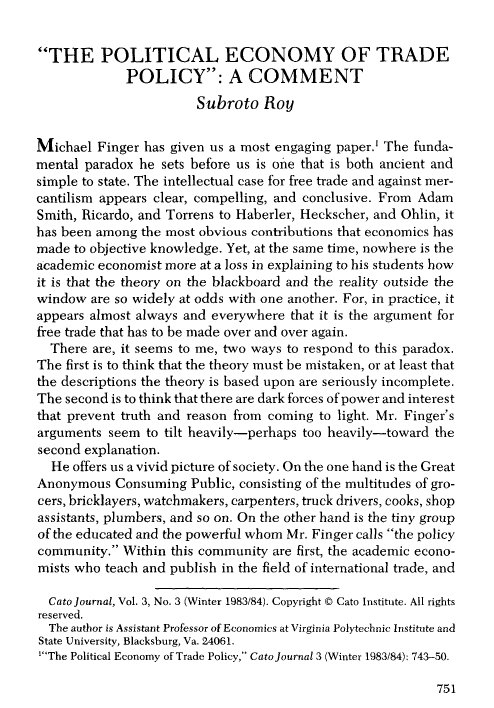

Textbook economics suggests world trade improves material welfare: consumers are better off when imports may compete freely in the home-market. Yet from Adam Smith’s critique of mercantilism to modern theories of rent-seeking, domestic producers in import-competing industries have been described as trying to restrict international trade by tariffs or other means. How is it producers so often succeed in persuading governments of the social costs of imports? Why are there not (or not as many, or not as powerful) consumer lobbies? Certainly there are high costs of organizing consumer lobbies relative to producer lobbies, but leaving that aside, is it possible consumers are ignorant and irrational? J. Michael Finger (1982, 1983/84) argued that in this respect consumers are in fact ignorant of their own best interests.

Roy (1983/84) suggested that a simple Keynesian observation offers a different explanation. A domestic household may be definitely better off by trade-liberalization on the expenditure side of its budget but the increased competitiveness of the economy accompanying liberalization may so decrease the expected value of its income that a risk-averse household would prefer the trade-protected status quo and have no incentive to lobby for trade-liberalization. Conversely, in a recession when the expected value of a household’s income declines, households have an incentive to lobby for trade-protection despite this worsening the expenditure side of their budgets.

The simplest of examples suffices to show all this. Let x1 be a non-traded domestic good, and x2 an imported good, and let a domestic household have preferences

U (x1, x2) = x1α . x2β

α + β < 1; 0 < α, β < 1 (1)

Let x1 be numeraire, p’ and p be the world and domestic prices of x2 respectively, and t be the tariff-rate on x2 such that p = (1 + t). p’. Let the household’s expected income be ya in the trade-protected state and yb in the trade-liberalized state, so its budget constraint is either

ya = x1 + (1 + t).p’. x2 in the trade-protected state (2a)

or

yb = x1 + p’. x2 in the trade-liberalized state (2b).

Maximizing (1) subject to (2a) gives a “final utility” in the trade-protected state, Ua*. Maximizing (1) subject to (2b) gives a “final utility” in the trade-liberalized state, Ub*.

Hence Ua* > Ub* as

[ya/yb] (α + β)/β > 1 + t where (α + β)/β > 1.

If income is certain in the trade-protected state but uncertain in the trade-liberalized state, a household’s risk-aversion will require loss in the expected utility of income in the trade-liberalized state to be offset by a gain in final utility that it receives as a consumer due to tariff-reduction.

E.g., let α = β = ½ and let the household have a certain income in the trade-protected state of $20,000; let it place a subjective probability of 1/4 on being unemployed with zero income in the trade-liberalized state, and 3/4 on maintaining the same income of $20,000.

Then Ua* > Ub* as [4/3]2 > 1 + t.

I.e., for any tariff-rate less than about 78% with these particular data, the household may rationally think itself better off in the trade-protected state than in the trade-liberalized state, and hence have no incentive to lobby for the latter.

Cooper (1987) remarked: “There should of course be a strong appeal to consumers of imported goods for removing restrictions. For a variety of reasons, political mobilization of consumers has been difficult in most countries. Many of these consumers also are employed in producing tradable goods, and they worry more about their jobs than about the purchasing power of a given wage. But most goods that move in international trade are not consumer goods. They are capital goods and intermediate products, and it should be easier to appeal to buyers of these intermediate products for import liberalization, because such buyers would enjoy a reduction in their costs.” The sentence italicized above may be consonant with the simple point made here.

References

Richard N. Cooper “Why liberalization meets resistance” in J. Michael Finger (ed.), The Uruguay Round, A Handbook on the Multilateral Trade Negotiations, World Bank, November 1987.

J. Michael Finger, “Incorporating the gains from trade into policy”, The World Economy, 5, December 1982, 367-78.

“The political economy of trade policy”, Cato Journal, 3, Winter 1983/84.

Subroto Roy, “The political economy of trade policy: comment”, Cato Journal, 3, Winter 1983/84″

I sent it to Economic Letters but the editor Professor Jerry Green rejected it, perhaps because it was too simple and unpretentious. And it remained unpublished until I put it on my blog in March 2009.

Yes it is relevant to the trade-problem America may face today, and yes perhaps both Mr Trump and Mr Sanders were in my audience at Cato, I do not know.

From Twitter 21.10.2016: I recollect three interactions after the talk, Donald J Trump or someone like him was seated midway in the hall in an aisle, praised the talk to me afterwards; he looked like a “preppie”, like myself. Bernie Sanders, or someone like him made a momentary comment as he charged by at speed; a third man (I think he was a Florida State professor who became a friend and later invited me there but I could not go) said I had “waxed eloquent”.

From Twitter 09.11.2016: Trump sat toffishly dressed in an aisle seat, congratulated me and introduced himself, Sanders charged out at speed after a momentary word…I recall three interactions after the talk, one each with Trump and Sanders, or someone like them

see too https://independentindian.com/2016/11/24/fixing-washington-on-improving-institutional-design-in-the-united-states/

from My American years

https://independentindian.com/thoughts-words-deeds-my-work-1973-2010/my-american-years-1980-96-battling-for-the-freedom-of-my-books/

I have put these documents here now in 2017 after recollecting in 2016 during the American election campaign that both Bernie Sanders and Donald J Trump had been present at that trade policy conference in Washington in September 1983 and both had interacted with me briefly! Mr Sanders had expressed a momentary word of praise and had charged out of the large crowd at speed with I think a small retinue of staff. (I asked someone who that had been, and recall Vermont being mentioned, and recall the spectacles and the fierce earnest expression.) Mr Trump had sat in an aisle seat in the middle and he had looked at me and I at him (we were both relatively young men in that middle aged milieu) as I had walked up to the podium. He was toffishly dressed, looking somewhat out of place in a nerdy conference of academics, journalists, politicians and policy wonks. As I had come down from the podium he had stood up and introduced himself as “Donald J Trump”, and said “Manhattan real estate” possibly upon my enquiry; he praised my talk quite profusely and might have said something like he was surprised that “coming from the part of the world” I did I had grasped what I had done about America.