from World Economy & Central Banking Seminar at Facebook

Professor Rajan’s statement “I determine the monetary policy. I say what it is….ultimately the interest rate that is set is set by me” equates Indian monetary policy with the money interest rate; but monetary policy in India has always involved far more than that, namely, the bulk of Indian banking and insurance has been in government hands for decades, all these institutions have been willy-nilly compelled to hold vast stocks of government debt, both Union and State, on their asset-sides…and unlimited unending deficit finance has led to vast expansion of money supply, making it all rather fragile. My “India’s Money” in 2012 might be found useful. http://tinyurl.com/o9dhe8d

11 April 2014

from World Economy & Central Banking Seminar at Facebook

I have to wonder, What is Professor Rajan on about? Growth in an individual country is affected by the world monetary system? Everyone for almost a century has seen it being a real phenomenon affected by other real factors like savings propensities, capital accumulation, learning and productivity changes, innovation, and, broadly, technological progress… A “source country” needs to consult “recipient” countries before it starts or stops Quantitative Easing? Since when? The latter can always match policy such as to be more or less unaffected… unless of course it wants to ride along for free when the going is good and complain loudly when it is not…. Monetary policy may affect the real economy but as a general rule we may expect growth (a real phenomenon) to be affected by other real factors like savings propensities, capital accumulation, learning and productivity changes, innovation, and, broadly, technological progress..

22 September 2013

“Let us remember that the postponement of tapering is only that, a postponement. We must use this time to create a bullet proof national balance sheet and growth agenda, which creates confidence in citizens and investors alike…”

“Rajan has apparently said, “We do not have a magic wand to make the problems disappear instantaneously, but I have absolutely no doubt we will deal with them.” Of course there are no magic wands but there is a scientific path forward. It involves system-wide improvements in public finance and accounting using modern information technology to comprehend government liabilities and expenditures and raise their productivity. It also involves institutional changes in public decision-making like separating banking and central banking from the treasury while making the planning function serve the treasury function rather than pretend to be above it. It is a road long and arduous but at its end both corruption and inflation will have been reduced to minimal levels. The rupee will have acquired sufficient integrity to become a hard currency of the world in the sense the average resident of, say, rural Madhya Pradesh or Mizoram may freely convert rupees and hold or trade foreign currencies or precious metals as he/she pleases. India signed the treaty of Versailles as a victor and was an original member of the League of Nations, the United Nations and the IMF. Yet sovereign India has failed to develop a currency universally acceptable as freely convertible world money. It is necessary and possible for India to aim to do so because without such a national aim, the integrity of the currency continues to be damaged regularly by governmental abuse. An RBI governor’s single overriding goal should be to try to bring a semblance of integrity to India’s money both domestically and worldwide.”

No magic wand, Professor Rajan? Oh but there is… read up all this over some hours and you will find it… (Of course it’s not from magic really, just hard economic science & politics)

Professor Raghuram Govind Rajan of the University of Chicago Business School deserves everyone’s congratulations on his elevation to the Reserve Bank of India’s Governorship. But I am afraid I cannot share the wild optimism in India’s business media over this. Of course there are several positives to the appointment. First, having a genuine PhD and that too from a top school is a rarity among India’s policy-makers; Rajan earned a 1991 PhD in finance at MIT’s management school for a thesis titled “Essays on banking” (having to do we are told “with the downside to cozy bank-firm relationships”). Secondly, and related, he has not been a career bureaucrat as almost all RBI Governors have been in recent decades. Thirdly, he has been President of the American Finance Association, he won the first Fischer Black prize in finance of that Association, and during Anne Krueger’s 2001-2006 reign as First Deputy MD at the IMF, he was given the research role made well-known by the late Michael Mussa, that of “Economic Counselor” of the IMF.

Hence, altogether, Professor Rajan has come to be well-known over the last decade in the West’s financial media. Given the dismal state of India’s credit in world capital markets, that is an asset for a new RBI Governor to have.

On the negatives, first and foremost, if Professor Rajan has renounced at any time his Indian nationality, surrendered his Indian passport and sworn the naturalization oath of the USA, then he is a US citizen with a US passport and loyalty owed to that country, and by US law he will have to enter the USA using that and no other nationality. If that happens to be the factual case, it will be something that comes out in India’s political cauldron for sure, and there will arise legal issues and court orders barring him from heading the RBI or representing India officially, e.g. when standing in for India’s Finance Minister at the IMF in Washington or the BIS in Basle etc. Was he an Indian national as Economic Counselor at the IMF? The IMF has a tradition of only European MDs and at least one American First Deputy MD. The Economic Counselor was always American too; did Rajan break that by having remained Indian, or conform to it by having become American? It is a simple question of fact which needs to come out clearly. Even if Rajan is an American, he and the Government of India could perhaps try to cite to the Indian courts the new precedent set by the venerable Bank of England which recently appointed a Canadian as Governor.

Let me take two examples. Does Rajan realise how the important Bottomley-Chandavarkar debates of the 1960s about India’s rural credit markets influenced George Akerlof’s “Market for Lemons” theory and prompted much work on “asymmetric information”, signalling etc in credit-markets, insurance-markets, labour-markets and markets in general, as acknowledged in the awards of several Bank of Sweden prizes? Or will he need a tutorial on the facts of rural India’s financial and credit markets, and their relationship with the formal sector? What the Bottomley-Chandavarkar debate referred to half a century ago still continues in rural India insofar as large arbitrage profits are still made by trading across the artificially low rates of money interest caused by financial repression of India’s “formal” monetised sector with its soft inconvertible currency against the very high real rates of return on capital in the “informal” sector. It is obvious to the naked eye that India is a relatively labour-abundant country. It follows the relative price of labour will be low and relative price of capital high compared to, e.g. the Western or Middle Eastern economies, with mobile factors of production like labour and capital expected to flow accordingly across national boundaries. Indian nominal interest-rates in organized credit markets have been for decades tightly controlled, making it necessary to go back to Irving Fisher’s data to obtain benchmark interest-rates, which, as expected, are at least 2%-3% higher in India than in Western capital markets. Joan Robinson once explained “the difference between 30% in an Indian village and 3% in London” saying “side by side with the industrial revolution went great technical progress in the provision of credit and the reduction of lender’s risk.”

What is logically certain is no country can have both relatively low world prices for labour and relatively low world prices for capital! Yet that impossibility seems to have been what India’s purported economic “planners” have planned to engineer! The effect of financial repression over decades may have been to artificially “reverse” or “switch” the risk-premium — making it lucrative for there to be capital flight out of India, with real rates of return on capital within India being made artificially lower than those in world markets! Just as enough export subsidies and tariffs can make a country artificially “reverse” its comparative advantage with its structure of exports and imports becoming inverted, so a labour-rich capital-scarce country may, with enough financial repression, end up causing a capital flight. The Indian elite’s capital flight out of India exporting their adult children and savings overseas may be explained as having been induced by government policy itself.

Secondly, Professor Rajan as a finance and banking specialist, will see at once the import of this graph above that has never been produced let aside comprehended by the RBI, yet which uses the purest RBI data. It shows India’s mostly nationalised banks have decade after decade gotten weaker and weaker financially, being kept afloat by continually pumping in of new “capital” via “recapitalisation” from the government that owns them, using more and more of the soft inconvertible currency that has been debauched merrily by government planners. The nationalised banks with their powerful pampered employee unions, like other powerful pampered employee unions in the government sector, have been the bane of India, where a mere 30 million privileged people in a vast population work with either the government or the organised private sector. The RBI’s own workforce at last count was perhaps 75,000… the largest central bank staff in the world by far!

Will Rajan know how to bring some system out of the institutional chaos that prevails in Indian banking and central banking? If not, he should start with the work of James Hanson “Indian Banking: Market Liberalization and the Pressures for Institutional and Market Framework Reform”, contained in the book created by Anne Krueger who brought him into the IMF, and mentioned in my 2012 article “India’s Money” linked below.

The central question for any 21st century RBI Governor worth the name really becomes whether he or she can stand up to the Finance Ministry and insist that the RBI stop being a mere department of it — even perhaps insisting on constitutional status for its head to fulfill the one over-riding aim of trying to bring a semblance of integrity to India’s currency both domestically and worldwide. Instead it is the so-called “Planning Commission” which has been dominating the Treasury that needs to be made a mere department of the Finance Ministry, while the RBI comes to be hived off to independence!

The path forward involves system-wide improvements in public finance and accounting using modern information technology to comprehend government liabilities and expenditures and raise their productivity, plus institutional changes in public decision-making like separating banking and central banking from the Treasury while making the planning function serve the Treasury function rather than pretend to be above it. The road described is long and arduous but at its end both corruption and inflation will have been reduced to minimal levels, and the rupee would have acquired integrity enough to become a hard currency of the world in the sense the average resident of, say, rural Madhya Pradesh or Mizoram may freely convert rupees and hold or trade foreign currencies or precious metals as he/she pleases.

India signed the Treaty of Versailles as a victor and was an original member of the League of Nations, UN and IMF. Yet sovereign India has failed to develop a currency universally acceptable as a freely convertible world money. It is necessary and possible for India to do so. Without such a national aim, the integrity of the currency continues to be damaged regularly by governmental abuse.

Professor Rajan will not want to be merely an adornment for the GoI in world capital markets for a few years, waiting to get back to his American career and life and perhaps to the IMF again. As RBI Governor, he can find his magic wand if he reads and reflects hard enough using his undoubted academic acumen, and then acts to lead India accordingly. Here is the basic reading list:

“On the blissful innocence of the RBI” (2009) From Facebook:

Subroto Roy can only sigh at the fact that while he has had to struggle for 35 years trying to grasp and then apply serious monetary economics to India’s circumstances, the RBI Governor & his four Deputy Governors appear blissfully innocent of all Hicks, Tobin, Friedman, Cagan et al yet exude confidence enough to “Waffle Away!”

A Small Challenge to the RBI’s Governor Subbarao April 21, 2010

The Hon’ble Gov of the Reserve Bank of India Shri D Subbarao

Dear Governor Subbarao,

You said yesterday, April 20 2010, that the Reserve Bank of India has a macroeconomic model which it uses but which you had personally not seen.

I have given two lectures at your august offices, one by invitation of Governor Jalan and Deputy Governor Reddy on April 29, 2000 to address the Conference of State Finance Secretaries, the other on May 5, 2005 to address the Chief Economist’s Monetary Economics Seminar. On both occasions, I had inquired of the RBI’s own models by which I could contrast my own but came to understand there were none.

If since then the RBI has now constructed a macroeconomic model of India’s economy, it is splendid news.

May I request the model be released publicly on the Internet at once, so its specifications of endogenous and exogenous variables, assumed coefficients, and sources of time-series data all may be seen by everyone in the country and abroad? Scientific scrutiny and replication of results would thus come to be permitted.

I would be especially interested to know the demand for money function that you have used. I well remember my meeting with the late great Sukhamoy Chakravarty on July 14 1987 at his Planning Commission offices, when he signed and gifted me his last personal copy of the famous Reserve Bank report by the committee he had chaired and of which he told me personally Dr Rangarajan had been the key author – that report may have contained the first official discussion of the demand for money function in India.

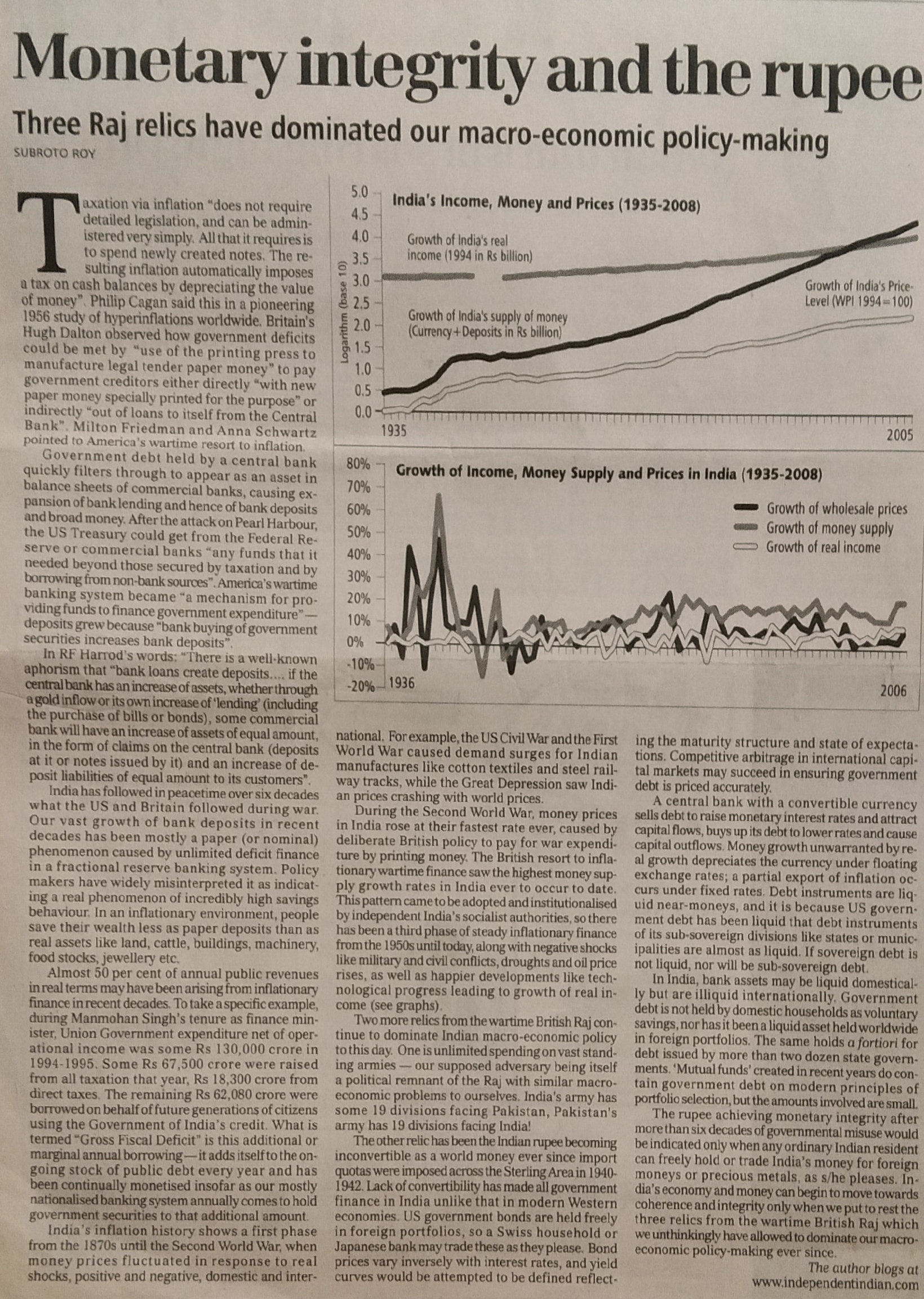

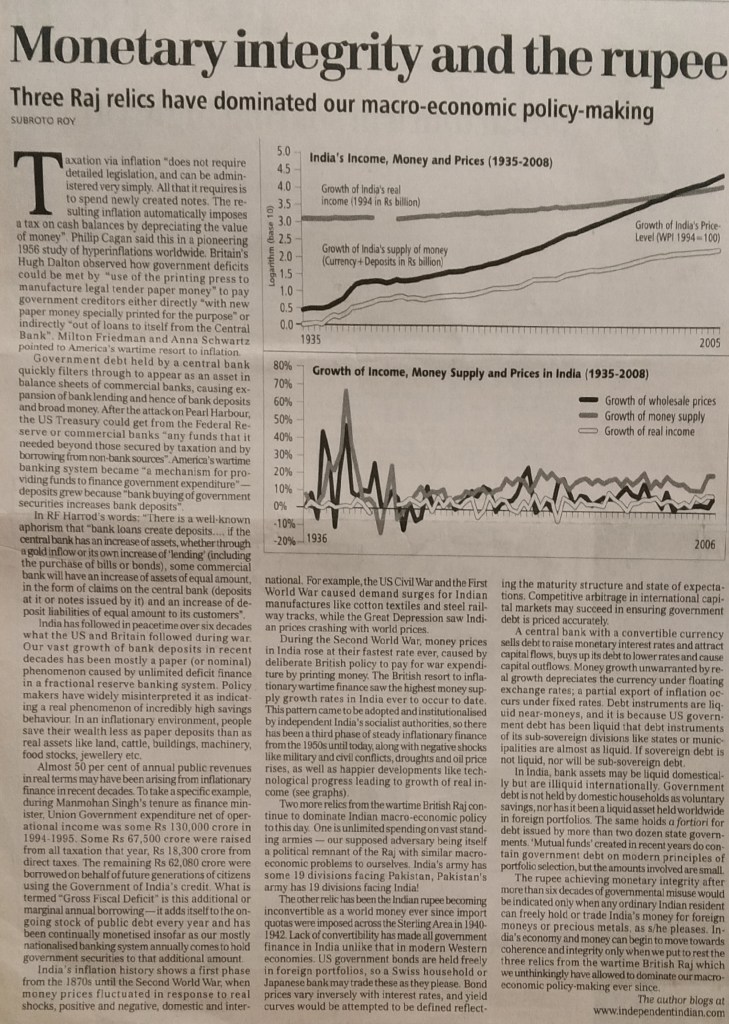

Taxation via inflation “does not require detailed legislation, and can be administered very simply. All that it requires is to spend newly created notes. The resulting inflation automatically imposes a tax on cash balances by depreciating the value of money”. Philip Cagan said this in a pioneering 1956 study of hyperinflations worldwide. Britain’s Hugh Dalton observed how government deficits could be met by “use of the printing press to manufacture legal tender paper money” to pay government creditors either directly “with new paper money specially printed for the purpose” or indirectly “out of loans to itself from the Central Bank”. Milton Friedman and Anna Schwartz pointed to America’s wartime resort to inflation.

Government debt held by a central bank quickly filters through to appear as an asset in balance-sheets of commercial banks, causing expansion of bank-lending and hence of bank-deposits and broad money. After the attack on Pearl Harbour, the US Treasury could get from the Federal Reserve or commercial banks “any funds that it needed beyond those secured by taxation and by borrowing from non-bank sources”. America’s wartime banking system became “a mechanism for providing funds to finance government expenditure” — deposits grew because “bank buying of government securities increases bank deposits”.

In RF Harrod’s words: “There is a well-known aphorism that ‘bank loans create deposits’…. if the central bank has an increase of assets, whether through a gold inflow or its own increase of ‘lending’ (including the purchase of bills or bonds), some commercial bank will have an increase of assets of equal amount, in the form of claims on the central bank (deposits at it or notes issued by it) and an increase of deposit liabilities of equal amount to its customers”.

India has followed in peacetime over six decades what the USA and Britain followed during war. Our vast growth of bank-deposits in recent decades has been mostly a paper (or nominal) phenomenon caused by unlimited deficit-finance in a fractional reserve banking system. Policy-makers have widely misinterpreted it as indicating a real phenomenon of incredibly high savings behaviour. In an inflationary environment, people save their wealth less as paper deposits than as real assets like land, cattle, buildings, machinery, food-stocks, jewellery etc.

Almost 50% of annual public revenues in real terms may have been arising from inflationary finance in recent decades. To take a specific example, during Dr Manmohan Singh’s tenure as Finance Minister, Union Government expenditure net of operational income was some Rs. 1.3 trillion (Rs 1.3 lakh crore) in 1994-1995. Some Rs. 675 billion (1 bn= 100 crore) was raised from all taxation that year, Rs 183 billion from direct taxes. The remaining Rs. 620.8 billion was borrowed on behalf of future generations of citizens using the Government of India’s credit. What is termed “Gross Fiscal Deficit” is this additional or marginal annual borrowing — it adds itself to the ongoing stock of public debt every year and has been continually monetised insofar as our mostly nationalized banking system annually comes to hold government securities to that additional amount.

India’s inflation-history shows a first phase from the 1870s until the Second World War when money prices fluctuated in response to real shocks, positive and negative, domestic and international. E.g., the US Civil War and First World War caused demand surges for Indian manufactures like cotton textiles and steel railway-tracks, while the Great Depression saw Indian prices crashing with world prices.

During the Second World War, money prices in India rose at their fastest rate ever, caused by deliberate British policy to pay for war expenditure by printing money. The British resort to inflationary wartime finance saw the highest money supply growth rates in India ever to occur to date. This pattern came to be adopted and institutionalised by independent India’s socialist authorities, so there has been a third phase of steady inflationary finance from the 1950s until today, along with negative shocks like military and civil conflicts, droughts and oil price-rises, as well as happier developments like technological progress leading to growth of real income (see graph).

Two more relics from the wartime British Raj continue to dominate Indian macroeconomic policy to this day. One is unlimited spending on vast standing armies — our supposed adversary itself being a political remnant of the Raj with similar macroeconomic problems to ourselves. India’s army has some 19 divisions facing Pakistan, Pakistan’s army has 19 divisions facing India!

The other relic has been the Indian rupee becoming inconvertible as a world money ever since import quotas were imposed across the Sterling Area in 1940-1942. Lack of convertibility has made all government finance in India unlike that in modern Western economies. US government bonds are held freely in foreign portfolios so a Swiss household or Japanese bank may trade these as they please. Bond prices vary inversely with interest-rates, and yield curves would be attempted to be defined reflecting the maturity-structure and state of expectations. Competitive arbitrage in international capital markets may succeed in ensuring government debt is priced accurately.

A central bank with a convertible currency sells debt to raise monetary interest rates and attract capital flows, buys up its debt to lower rates and cause capital outflows. Money growth unwarranted by real growth depreciates the currency under floating exchange rates; a partial export of inflation occurs under fixed-rates. Debt instruments are liquid near-moneys, and it is because US Government debt has been liquid that debt instruments of its sub-sovereign divisions like States or municipalities are almost as liquid. If sovereign debt is not liquid, nor will be sub-sovereign debt.

In India, bank assets may be liquid domestically but are illiquid internationally. Government debt is not held by domestic households as voluntary savings nor has it been a liquid asset held worldwide in foreign portfolios. The same holds *a fortiori* for debt issued by more than two dozen State Governments. “Mutual funds” created in recent years do contain government debt on modern principles of portfolio-selection but amounts involved are small. The Rupee achieving monetary integrity after more than six decades of governmental misuse would be indicated only when any ordinary Indian resident can freely hold or trade India’s money for foreign moneys or precious metals as he/she pleases. India’s economy and money can begin to move towards coherence and integrity only when we put to rest the three relics from the wartime British Raj which we unthinkingly have allowed to dominate our macroeconomic policy-making ever since.

The Excel graphs built on my data were made into a nice picture by Business Standard but seem to have been removed from their website, and hence are reproduced here now for the first time today, Oct 2, 2011:

Indian Money & Credit by

Subroto Roy

First published in The Sunday Statesman, August 6 2006, Editorial Page Special Article

One rural household may lend another rural household 10 kg or 100 kg of grain or seed for a short time. When it does, it expects to receive back a little more than the amount lent ~ even if that little amount is in services or in plain goodwill among friends or neighbours. That extra amount is “real interest”, and the percentage of its value relative to the whole is the “real rate of interest”. So if 10 kg of grain are lent for two weeks and 11 kg are returned, an implicit real rate of interest of 10 per cent has been paid over that short period. The future is always less valuable than the present in the sense that 10 kg of grain today is worth something more than the prospect of the same 10 kg of grain tomorrow.

But loans may be made in terms of money rather than real units of grain, thus the change in the value of money over the period of the loan becomes relevant. If a loan of Rs 100,000 is made by a bank to a borrower for one year at a simple interest rate of 13 per cent per annum, and the value of money then declines at 8 per cent over the year, the debtor is paying real interest of just about 13 per cent-8 per cent = 5 per cent. The Yale economist Irving Fisher described how this monetary rate of interest equals the real rate of interest plus the rate of monetary inflation, while the great Swedish economist Knut Wicksell predicted inflation if the monetary rate fell below the real rate, and vice versa.

And there is another consideration too. A new cycle-rickshaw costs about Rs 5,000. A rickshaw driver who does not own his own machine has to pay the owner of the rickshaw a fixed rental of about Rs 15 per day. Now a government policy may want to see more cycle-rickshaw drivers owning their own machines, and allocate bank-credit accordingly. But some fraction of the drivers are alcoholics and hence are bad credit-risks, while others are industrious, have strong family lives and are good credit-risks. If a creditor is unable to distinguish between who is an alcoholic and who is not, credit terms will tend towards subsidising the alcoholic and taxing the industrious.

On the other hand, a creditor who knows each debtor individually will also know their credit-risks, and price individual loans to them accordingly. India’s credit markets, both rural and urban, have been segmented always into “formal” and “informal”, and remain so despite (or perhaps because of) much government intervention in recent decades.

Banks and the Reserve Bank of India operate in formal financial markets, but the informal credit market is where the real action is. For example, a mosaic-machine used in the construction business costs Rs 15,000 brand new and gets to be rented out at the rate of Rs 150 per day.

Someone with access to formal sector bank loans at say 13 per cent per annum, might borrow the Rs 15,000, buy a machine, rent it out, break-even within a few months and make a whopping profit afterwards. Everyone would thus hunger after subsidised formal sector bank loans, and these would be rationed quickly and then come to be allocated to people known to bank officials (like their own friends and relatives).

Rates of return on capital, i.e. real profits, are and always have been massively high in India, and that is what is to be expected because capital, both machinery and finance, is relatively scarce as a factor of production. Rates of return on labour, i.e. real wages, are on the other hand relatively low in India thanks to our vast population. For these reasons we have had for three centuries foreigners coming to India to invest their capital in enterprise and make a profit, while Indians have emigrated all over the world from Fiji to Britain to America in search of higher wages.

Now all of this is very elementary reasoning well known to serious monetary economists, yet it seems to have always escaped India’s monetary and fiscal decision-makers. For example, just the other day, the Finance Minister said in Parliament that all rural banks had been instructed to lend farmers credit at a 7 per cent (monetary) rate of interest, and failure to do so would lead to punishment. By the rickshaw example (in fact many cycle-rickshaw drivers are also marginal farmers), the FM did not wish to, and of course cannot in practice, distinguish between good and bad credit-risks among the recipients of such loans. If the value of money is declining by, say, 8 per cent per annum, a 7 per cent monetary rate is equivalent to a minus 1 per cent real rate. i.e., the FM would have done some Humpty Dumpty economics and caused the future prospect of holding Rs 1,000 tomorrow to be more and not less valuable than the certainty of holding Rs 1,000 today. It is inevitable there will be credit-rationing when credit is so massively subsidised, so the typical borrowing farmer will get some little fraction of his credit-needs at the official government price of 7 per cent per annum and then have to get the bulk of his credit-needs fulfilled in the informal market ~ at a price perhaps of 1 per cent-5 per cent PER DAY! The FM promising in his Budget to subsidise farm credit sounds nice on TV but may be wholly futile as a way of stopping farmers’ suicides.

The same kind of Humpty Dumpty monetary economics has been religiously pursued by the Reserve Bank of India for decades upon directions from its owner and master, the Finance Ministry ~ which in turn has always meekly followed the dictates of India’s unreasonable politicians of all parties. Formal sector interest rates in India have been for decades so artificially lowered that even if we use official figures measuring inflation, this leads to real interest rates being lower in capital-scarce India than in the capital-rich West! (See graphs). Negative or near-zero real interest rates in India’s formal financial sector coexisting with massively high profit rates in informal credit markets point to continuous processes of low risk profits being made by arbitrage between the two. That is why the organised private and public sectors seem so pleased with official credit policies ~ while every borrower in the informal credit markets always has suicide not far from his/her mind.

Other than Dr Rangarajan who once mentioned it, we have never had an RBI Governor who has wished to see the Reserve Bank of India constitutionally independent of the Government of the day, and hence dedicated to restoring the integrity of India’s money. Playing with the repo rate or other short term monetary rates is fun and makes the RBI think it is doing something as important as the US or UK central banks. Certainly the upward trend in such short term rates over the last few months is better than the nonsensical flip-flops previously. But it is small potatoes compared to the really giant variables which are all fiscal and not monetary in India. For example, Sonia Gandhi (as advised by another naturalized Indian, Jean Drèze, disciple of the Non-Resident Amartya Sen) insisted on a massive “Rural Employment Guarantee”; Manmohan Singh and Pranab Mukherjee have insisted on massive foreign weapons’ purchases and government wage increases; Praful Patel on massive foreign aircraft purchases; Arjun Sengupta on Scandinavian welfare benefits; Montek Ahluwalia on nuclear reactor purchases (so South Delhi will be able at least to run its ACs in 20 years’ time). All this adds endlessly to the stock of government paper being held as bank-assets, while the currency remains inconvertible (See e.g. The Statesman 30 October 2005, 6-8 January, 23 April 2006).The RSS/BJP and JNU/Left have been equally bereft of serious thought.

Tell any suicidal farmer that the Government of India has been borrowing larger and larger amounts every year just to pay interest on previously incurred debts; it may make him realise there are famous and powerful people who are even more unwise than himself and amount to effective suicide-prevention therapy. But do not tell him that they unlike himself have been playing with public money ~ or you may have the opposite effect.

The RBI and Financial Repression (A Stock Market on Steroids)

by

Subroto Roy First published in The Statesman, Perspective Page, October 27 2005

If the average Indian citizen feels flummoxed at hearing all the fancy words from official spokesmen and the talking heads on TV and the expensive pink business newspapers — words like “credit offtake”, “liquidity”, “reverse repo rate” “medium term”, “inflation mandate” etc — there is help at hand. It is as likely as not that the purveyors are as flummoxed themselves even while they bandy these terms about in what has been passing for monetary policy in India in recent years. No one has any reliable economic models backed by time-series data to support all the waffle.

Here is an example.

The Government (and specifically the department of the Finance Ministry known as the RBI) will have us believe that the decline in the value of money that has been occurring in India has been at less than 5% per annum. According to official figures, the average Indian’s purchase of consumable goods and services (food, housing, clothing, transport etc) has been costing more every year by merely 5% at the very most. “What you can buy for Rs. 1000 in one year, you have to pay just Rs 1050 to buy the next year” is what the Government will have us believe. But is anyone’s personal experience of the diminishing value of the domestic currency in India consonant with what official spokesmen say inflation happens to be?

You may well reply that you cannot quite recall what Rs. 1000 bought for you last year. Precisely so. Nor really can anyone else — and that mutual collective loss of memory on the part of the public is something that India’s Government (like many other governments across time and space) has been literally banking on!

Consider a few very simple calculations. Suppose a citizen earns an annual income of Rs. 100,000, and an honest Government told him/her to pay total taxes (from both income and expenditure) of 10%. Clearly Rs. 90,000 would be left for the citizen to spend on his/her various choices of consumption or saving afterwards. If the citizen could assume the value of money was constant (inflation was 0%) then this Rs. 90,000 in one year would buy the same amount of goods and services the next year. But instead we may be living in a political system where the Government officially taxes very lightly, and then dishonestly taxes very heavily by reducing the value of money invisibly, i.e. by inflation. The Government may make the official tax-rate 8% and the actual inflation-rate 15%. The citizen who has Rs. 100,000 will then pay Rs. 8,000 in nominal taxes, but the Rs. 92,000 that is nominally left over for his own consumption and savings, will be made to decline by a further 15% every year.

I.e., a further value of Rs.13,800 (15% of Rs. 92,000) would effectively disappear as an invisible tax from the household budget due to the decline in the value of money, without the household being any wiser. In real terms, the household would have only Rs. 78,200 left.

Where would that extra value disappear to? Clearly, the beneficiary of this invisible extraction of real resources from household budgets would be the only entity that is able to compel the decline in the value of money, namely, the Government, which holds monopoly power to print the pieces of paper (at zero cost) that we call “money” and which we are forced by circumstances to use to expedite our real transactions of goods and services. Roughly speaking, that is how the Government’s own budget deficit gets financed in India.

I.e., the Government of India has its own (massive) expenditures — not merely on things like roads and bridges and military tanks and submarines, but also on ministers and bureaucrats’ wages etc., besides enormous interest payments on past debts incurred by the Government. If the expenditures exceed the visible revenues raised from taxation, as they have done by perhaps 40-50% or more every year for several decades, then the difference gets bridged by printing more paper money over which the Government has had a monopoly.

In India, a total of perhaps 18 million people work in all branches of government and a total of perhaps 12 million people work in the entire organised private sector. That makes 30 million people — with 4 dependants each, that accounts for perhaps 150 million people in the country. That leaves another 850 million people in our population of 1,000 million. Everyone, whether in the 150 million or the 850 million, rich and named or poor and anonymous, has had to use for his/her real transactions of goods and services the paper that the Government produces as money. By causing a decline in the value of this paper every year by x%, everyone who holds this paper, as well as assets denominated in this paper, suffers an invisible taxation of x% without quite realising it. The real revenue the Government of India extracts in this way is what has allowed it to balance its own books.

Furthermore, in the Indian case, what is said to be the inflation-rate and the actual inflation-rate experienced by ordinary people, may well be two different things. The wage-bill of those 18 million people employed by government agencies are linked directly to what official spokesmen say the inflation-rate is, so if the actual rate being experienced was higher and was announced as such, so would have to be that wage-bill and public expenditure! Official spokesmen may tell us the decline in the value of money has been merely 5% or less a year, so what cost Rs. 1000 last year costs Rs. 1050 this year, but as a matter of plain fact, the average citizen’s experience (and memory) may well tell him/her something different – e.g. that what cost Rs. 1000 last year, is in fact costing Rs. 1100 or Rs 1150 or Rs 1200 this year.

So much for the value of money. Now turn to interest-rates.

Here too, the average citizen need not be a rocket-scientist to know that relative to the Western countries, India is labour abundant and is capital scarce. Roughly speaking, that means we have relatively more people and fewer high-rise concrete buildings than the West does. Where then would you expect wages (the price of labour) to be higher, in the West or in India? Clearly in the place where labour is more scarce, namely, the West. And where would you expect interest-rates (the price of capital) to be higher? Clearly, where capital is relatively more scarce, namely India. Such was clearly the case between 1864 and 1926 (Fig. 1). Calcutta bank interest-rates were uniformly higher by about 2-3% than London bank interest-rates (in an era of zero inflation). But something wholly different occurred in the pseudo-socialist India after Independence. E.g., for the years 1975-1992 official Indian interest-rates (adjusted for inflation) were uniformly lower than those in world capital markets represented by the USA (Fig. 2). That remains true today. Not only have the higher wages of the West been attractive to Indians, so seems to be the higher real rates of return on capital! Hence everyone who could fled India – exporting their adult children and their savings abroad , leaving future generations of the anonymous masses with larger public debts to pay the bills in due course. There has been a flight of skilled labour and as well as capital flight from India — are foreigners going to come when they can see the Indian “elite” has fled? Official real interest-rates in India today may well be negative if inflation is properly measured, which would explain the Bombay stock-market boom the same way an athlete can perform better when on steroids.

Of course in the unorganised capital markets, actual real rates of return have always been higher in India than in the West and remain so. Just ask anyone in the unorganised capital markets how much he has to pay to rent machinery on a daily basis e.g. in the building or construction trade in an Indian city or small town or village. He will quote you rates of 2% or 5% or 10% — per day. Hence there is a massive distortion between what is happening in the unorganised capital markets all over the country and the official money markets the RBI believes itself to be presiding over in Bombay. Until the RBI starts to tell us frankly about this phenomenon, which is known to economists as “financial repression” and which has been caused by runaway Government spending programmes in India for decades, the average citizen may discount all the talk about a few basis points changing here and there on this or that nominal rate, in our pale imitation of what we think the US Fed or the European or British central banks do as policy. The truth is the RBI has never been allowed to model itself after those institutions. Instead, India has had nationalised commercial banking whose pampered inefficient management and staff have allowed the holding of massive amounts of government debt as assets in their balance-sheets, all denominated in an inconvertible controlled currency, and all presided over by a “one-tier” central bank patterned on the old Gosbank of the former Soviet Union, completely subservient to the dictates of the runaway spending that this or that particular set of politicians in power may demand. If there are dreams to be dreamt by honest economists in India, it would be for all that to be made to change.

The search engine above should locate any article by its title; the Index and Archives may be used as well.

Readers are welcome to quote from my work under the normal “fair use” rule, but please try to quote me by name and indicate the place of original publication in case of work being republished here. I am at Twitter @subyroy, see my latest tweets above

signalling etc in credit-markets, insurance-markets, labour-markets and markets in general, as acknowledged in the awards of several Bank of Sweden prizes? Or will he need a tutorial on the facts of rural India’s financial and credit markets, and their relationship with the formal sector? What the Bottomley-Chandavarkar debate referred to half a century ago still continues in rural India insofar as large arbitrage profits are still made by trading across the artificially low rates of money interest caused by financial repression of India’s “formal” monetised sector with its soft inconvertible currency against the very high real rates of return on capital in the “informal” sector. It is obvious to the naked eye that India is a relatively labour-abundant country. It follows the relative price of labour will be low and relative price of capital high compared to, e.g. the Western or Middle Eastern economies, with mobile factors of production like labour and capital expected to flow accordingly across national boundaries. Indian nominal interest-rates in organized credit markets have been for decades tightly controlled, making it necessary to go back to Irving Fisher’s data to obtain benchmark interest-rates, which, as expected, are at least 2%-3% higher in India than in Western capital markets. Joan Robinson once explained “the difference between 30% in an Indian village and 3% in London” saying “side by side with the industrial revolution went great technical progress in the provision of credit and the reduction of lender’s risk.”

signalling etc in credit-markets, insurance-markets, labour-markets and markets in general, as acknowledged in the awards of several Bank of Sweden prizes? Or will he need a tutorial on the facts of rural India’s financial and credit markets, and their relationship with the formal sector? What the Bottomley-Chandavarkar debate referred to half a century ago still continues in rural India insofar as large arbitrage profits are still made by trading across the artificially low rates of money interest caused by financial repression of India’s “formal” monetised sector with its soft inconvertible currency against the very high real rates of return on capital in the “informal” sector. It is obvious to the naked eye that India is a relatively labour-abundant country. It follows the relative price of labour will be low and relative price of capital high compared to, e.g. the Western or Middle Eastern economies, with mobile factors of production like labour and capital expected to flow accordingly across national boundaries. Indian nominal interest-rates in organized credit markets have been for decades tightly controlled, making it necessary to go back to Irving Fisher’s data to obtain benchmark interest-rates, which, as expected, are at least 2%-3% higher in India than in Western capital markets. Joan Robinson once explained “the difference between 30% in an Indian village and 3% in London” saying “side by side with the industrial revolution went great technical progress in the provision of credit and the reduction of lender’s risk.”

")