Notes on gold and central banks (3 Nov 2009)

November 3, 2009 — drsubrotoroyMy response: “Who will? Central Banks as per the old gold exchange standard? There are well-known problems with all fixed exchange rate systems.”

Monetary Integrity and the Rupee (2008)

September 28, 2008 — drsubrotoroyMonetary Integrity and the Rupee: Three British Raj relics have dominated our macroeconomic policy-making

First published in Business Standard 28 September 2008

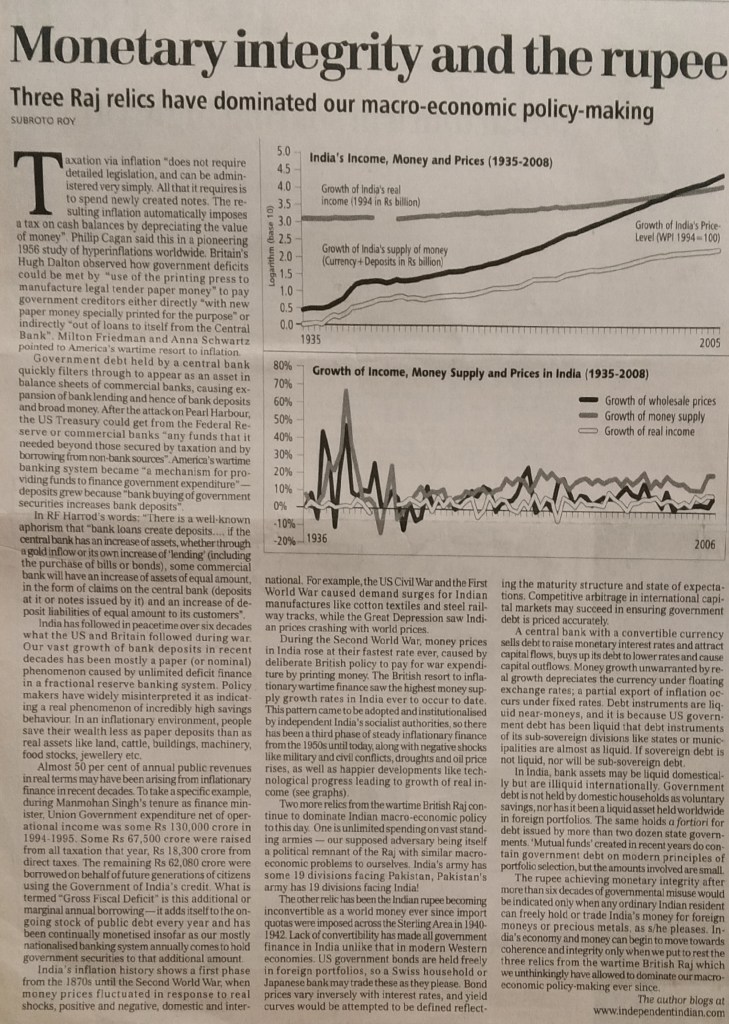

Taxation via inflation “does not require detailed legislation, and can be administered very simply. All that it requires is to spend newly created notes. The resulting inflation automatically imposes a tax on cash balances by depreciating the value of money”. Philip Cagan said this in a pioneering 1956 study of hyperinflations worldwide. Britain’s Hugh Dalton observed how government deficits could be met by “use of the printing press to manufacture legal tender paper money” to pay government creditors either directly “with new paper money specially printed for the purpose” or indirectly “out of loans to itself from the Central Bank”. Milton Friedman and Anna Schwartz pointed to America’s wartime resort to inflation.

Government debt held by a central bank quickly filters through to appear as an asset in balance-sheets of commercial banks, causing expansion of bank-lending and hence of bank-deposits and broad money. After the attack on Pearl Harbour, the US Treasury could get from the Federal Reserve or commercial banks “any funds that it needed beyond those secured by taxation and by borrowing from non-bank sources”. America’s wartime banking system became “a mechanism for providing funds to finance government expenditure” — deposits grew because “bank buying of government securities increases bank deposits”.

In RF Harrod’s words: “There is a well-known aphorism that ‘bank loans create deposits’…. if the central bank has an increase of assets, whether through a gold inflow or its own increase of ‘lending’ (including the purchase of bills or bonds), some commercial bank will have an increase of assets of equal amount, in the form of claims on the central bank (deposits at it or notes issued by it) and an increase of deposit liabilities of equal amount to its customers”.

India has followed in peacetime over six decades what the USA and Britain followed during war. Our vast growth of bank-deposits in recent decades has been mostly a paper (or nominal) phenomenon caused by unlimited deficit-finance in a fractional reserve banking system. Policy-makers have widely misinterpreted it as indicating a real phenomenon of incredibly high savings behaviour. In an inflationary environment, people save their wealth less as paper deposits than as real assets like land, cattle, buildings, machinery, food-stocks, jewellery etc.

Almost 50% of annual public revenues in real terms may have been arising from inflationary finance in recent decades. To take a specific example, during Dr Manmohan Singh’s tenure as Finance Minister, Union Government expenditure net of operational income was some Rs. 1.3 trillion (Rs 1.3 lakh crore) in 1994-1995. Some Rs. 675 billion (1 bn= 100 crore) was raised from all taxation that year, Rs 183 billion from direct taxes. The remaining Rs. 620.8 billion was borrowed on behalf of future generations of citizens using the Government of India’s credit. What is termed “Gross Fiscal Deficit” is this additional or marginal annual borrowing — it adds itself to the ongoing stock of public debt every year and has been continually monetised insofar as our mostly nationalized banking system annually comes to hold government securities to that additional amount.

India’s inflation-history shows a first phase from the 1870s until the Second World War when money prices fluctuated in response to real shocks, positive and negative, domestic and international. E.g., the US Civil War and First World War caused demand surges for Indian manufactures like cotton textiles and steel railway-tracks, while the Great Depression saw Indian prices crashing with world prices.

During the Second World War, money prices in India rose at their fastest rate ever, caused by deliberate British policy to pay for war expenditure by printing money. The British resort to inflationary wartime finance saw the highest money supply growth rates in India ever to occur to date. This pattern came to be adopted and institutionalised by independent India’s socialist authorities, so there has been a third phase of steady inflationary finance from the 1950s until today, along with negative shocks like military and civil conflicts, droughts and oil price-rises, as well as happier developments like technological progress leading to growth of real income (see graph).

Two more relics from the wartime British Raj continue to dominate Indian macroeconomic policy to this day. One is unlimited spending on vast standing armies — our supposed adversary itself being a political remnant of the Raj with similar macroeconomic problems to ourselves. India’s army has some 19 divisions facing Pakistan, Pakistan’s army has 19 divisions facing India!

The other relic has been the Indian rupee becoming inconvertible as a world money ever since import quotas were imposed across the Sterling Area in 1940-1942. Lack of convertibility has made all government finance in India unlike that in modern Western economies. US government bonds are held freely in foreign portfolios so a Swiss household or Japanese bank may trade these as they please. Bond prices vary inversely with interest-rates, and yield curves would be attempted to be defined reflecting the maturity-structure and state of expectations. Competitive arbitrage in international capital markets may succeed in ensuring government debt is priced accurately.

A central bank with a convertible currency sells debt to raise monetary interest rates and attract capital flows, buys up its debt to lower rates and cause capital outflows. Money growth unwarranted by real growth depreciates the currency under floating exchange rates; a partial export of inflation occurs under fixed-rates. Debt instruments are liquid near-moneys, and it is because US Government debt has been liquid that debt instruments of its sub-sovereign divisions like States or municipalities are almost as liquid. If sovereign debt is not liquid, nor will be sub-sovereign debt.

In India, bank assets may be liquid domestically but are illiquid internationally. Government debt is not held by domestic households as voluntary savings nor has it been a liquid asset held worldwide in foreign portfolios. The same holds *a fortiori* for debt issued by more than two dozen State Governments. “Mutual funds” created in recent years do contain government debt on modern principles of portfolio-selection but amounts involved are small. The Rupee achieving monetary integrity after more than six decades of governmental misuse would be indicated only when any ordinary Indian resident can freely hold or trade India’s money for foreign moneys or precious metals as he/she pleases. India’s economy and money can begin to move towards coherence and integrity only when we put to rest the three relics from the wartime British Raj which we unthinkingly have allowed to dominate our macroeconomic policy-making ever since.

The Excel graphs built on my data were made into a nice picture by Business Standard but seem to have been removed from their website, and hence are reproduced here now for the first time today, Oct 2, 2011:

")

See also, more recently,

India’s Money, 2012,

Critical assessments of India’s economic policy, plus my 3 Dec 2012 Delhi talk on India’s money, Interview on Lok Sabha TV 2012, GDI Impuls Zürich Interview, Sunday Guardian Interview & Asian Age/Deccan Herald coverage

https://independentindian.com/2013/11/23/coverage-of-my-delhi-talk-on-3-dec-2012/

122 sensible American economists

September 26, 2008 — drsubrotoroy$700 billion comes to more than, uhhhm, $6,000 per income taxpayer in the USA.

Somehow, I have an inkling that foreign central banks have been left holding more bad US debt than might be remembered — which would explain the embarrassment of Messrs Paulson and Bernanke vis-a-vis their foreign counterparts… Dollar depreciation and an American inflation seem to be inevitable over the next several years.

Subroto Roy

Milton Friedman: A Man of Reason, 1912-2006

November 22, 2006 — drsubrotoroy

A Man of Reason

Milton Friedman (1912-2006)

First published in The Statesman, Perspective Page Nov 22 2006

Milton Friedman, who died on 16 November 2006 in San Francisco, was without a doubt the greatest economist after John Maynard Keynes. Before Keynes, great 20th century economists included Alfred Marshall and Knut Wicksell, while Keynes’s contemporaries included Irving Fisher, AC Pigou and many others. Keynes was followed by his younger critic FA Hayek, but Hayek is remembered less for his technical economics as for his criticism of “socialist economics” and contributions to politics. Milton Friedman more than anyone else was Keynes’s successor in economics (and in applied macroeconomics in particular), in the same way David Ricardo had been the successor of Adam Smith. Ricardo disagreed with Smith and Friedman disagreed with Keynes, but the impact of each on the direction and course both of economics and of the world in which they lived was similar in size and scope.

Friedman’s impact on the contemporary world may have been largest through his design and advocacy as early as 1953 of the system of floating exchange-rates. In the early 1970s, when the Bretton Woods system of adjustable fixed exchange-rates collapsed and Friedman’s friend and colleague George P. Shultz was US Treasury Secretary in the Nixon Administration, the international monetary system started to become of the kind Friedman had described two decades earlier. Equally large was Friedman’s worldwide impact in re-establishing concern about the frequent cause of macroeconomic inflation being money supply growth rates well above real income growth rates. All contemporary talk of “inflation targeting” among macroeconomic policy-makers since the 1980s has its roots in Friedman’s December 1967 presidential address to the American Economic Association. His main empirical disagreement with Keynes and the Keynesians lay in his belief that people held the intrinsically worthless tokens known as “money” largely in order to expedite their transactions and not as a store of value – hence the “demand for money” was a function mostly of income and not of interest rates, contrary to what Keynes had suggested in his 1930s analysis of “Depression Economics”. It is in this sense that Friedman restored the traditional “quantity theory” as being a specific theory of the demand for money.

Friedman’s main descriptive work lay in the monumental Monetary History of the United States he co-authored with Anna J. Schwartz, which suggested drastic contractions of the money supply had contributed to the Great Depression in America. Friedman made innumerable smaller contributions too, the most prominent and foresighted of which had to do with advocating larger parental choice in the public finance of their children’s school education via the use of “vouchers”. The modern Friedman Foundation has that as its main focus of philanthropy. The emphasis on greater individual choice in school education exemplified Friedman’s commitments both to individual freedom and the notion of investment in human capital.

Friedman had significant influences upon several non-Western countries too, most prominently India and China, besides a grossly misreported episode in Chile. As described in his autobiography with his wife Rose, Two Lucky People (Chicago 1998), Friedman spent six months in India in 1955 at the Government of India’s invitation during the formulation of the Second Five Year Plan. His work done for the Government of India came to be suppressed for the next 34 years. Peter Bauer had told me during my doctoral work at Cambridge in the late 1970s of the existence of a Friedman memorandum, and N. Georgescu-Roegen told me the same in America in 1980, adding that Friedman had been almost insulted publicly by VKRV Rao at the time after giving a lecture to students on his analysis of India’s problems.

When Friedman and I met in 1984, I asked him for the memorandum and he sent me two documents. The main one dated November 1955 I published in Hawaii on 21 May 1989 during a project on a proposed Indian “perestroika” (which contributed to the origins of the 1991 reform through Rajiv Gandhi), and was later published in Delhi in Foundations of India’s Political Economy: Towards an Agenda for the 1990s, edited by myself and WE James.

The other document on Mahalanobis is published in The Statesman today for the first time, though there has been an Internet copy floating around for a few years. The Friedmans’ autobiography quoted what I said in 1989 about the 1955 memorandum and may be repeated: “The aims of economic policy (in India) were to create conditions for rapid increase in levels of income and consumption for the mass of the people, and these aims were shared by everyone from PC Mahalanobis to Milton Friedman. The means recommended were different. Mahalanobis advocated a leading role for the state and an emphasis on the growth of physical capital. Friedman advocated a necessary but clearly limited role for the state, and placed on the agenda large-scale investment in the stock of human capital, encouragement of domestic competition, steady and predictable monetary growth, and a flexible exchange rate for the rupee as a convertible hard currency, which would have entailed also an open competitive position in the world economy… If such an alternative had been more thoroughly discussed at the time, the optimal role of the state in India today, as well as the optimum complementarity between human capital and physical capital, may have been more easily determined.”

A few months before attending my Hawaii conference on India, Friedman had been in China, and his memorandum to Communist Party General Secretary Zhao Ziyang and two-hour dialogue of 19 September 1988 with him are now classics republished in the 1998 autobiography. Also republished there are all documents relating to Friedman’s six-day academic visit to Chile in March 1975 and his correspondence with General Pinochet, which speak for themselves and make clear Friedman had nothing to do with that regime other than offer his opinion when asked about how to reduce Chile’s hyperinflation at the time.

My association with Milton has been the zenith of my engagement with academic economics, with e-mails exchanged as recently as September. I was a doctoral student of his bitter enemy yet for over two decades he not only treated me with unfailing courtesy and affection, he supported me in lonely righteous battles: doing for me what he said he had never done before, which was to stand as an expert witness in a United States Federal Court. I will miss him much though I know that he, as a man of reason, would not have wished me to.

Subroto Roy

Towards a Highly Transparent Fiscal & Monetary Framework for India’s Union & State Governments (29 April 2000)

April 29, 2000 — drsubrotoroyTowards a Highly Transparent Fiscal & Monetary Framework for India’s Union & State Governments

An address by Dr Subroto Roy to

the Conference of State Finance Secretaries, Reserve Bank of India, Mumbai, 29 April 2000.

It is a great privilege to speak to this distinguished gathering of Finance Secretaries and economic policy-makers here at the Reserve Bank today. I should like to begin by thanking the Hon’ble Governor Dr Bimal Jalan and the Hon’ble Deputy Governor Dr YV Reddy for their kind invitation for me to do so. I should also like to record here my gratitude to their eminent predecessor, the Hon’ble Governor of Andhra Pradesh, Dr C Rangarajan, for his encouragement of my thinking on these subjects over several years.

My aim will be to share with you and seek your help with my continuing and very incomplete efforts at trying to comprehend as clearly as possible the major public financial flows taking place between the Union of India and each of its constituent States. I plan to show you by the end of this discussion how all the information presently contained in the budgets of the Union and State Governments of India, may be usefully transformed one-to-one into a fresh modern format consistent with the best international practices of government accounting and public budgeting.

I do not use the term “Central Government”, because it is a somewhat sinister anachronism left over from British times. When we were not a free nation, there was indeed a Central Government in New Delhi which took its orders from London and gave orders to its peripheral Provinces as well as to the British “Residents” parked beside the thrones of those who were called “Indian Princes”.

Free India has been a Union of States. There is a Government of the whole Union and there is a Government of each State. The Union is the sovereign and the sole international power, while the States, as political subdivisions of the Union, also possess certain sub-sovereign powers; as indeed do their own subdivisions like zilla parishads, municipalities and other local bodies in smaller measure.

Our 15 large States, which account for 97% of the population of the country, have an average of something like 61 million citizens each, which is vastly more than most countries of the world. In size of population at least, we are like 15 Frances or 15 Britains put together. The Indian Republic is unique or sui generis in that there has never been in history any attempt at federalism or democracy with such sheer large numbers of people involved.

In such a framework the citizen is supposed to feel a voter and a taxpayer at different levels, owing loyalty and taxes to both the national unit and the subdivisions in which he or she resides. In exchange, government at different levels is expected to provide citizens with public goods and services in appropriate measure. The problem of optimal fiscal decentralisation in India as elsewhere is one of allocating to each level of government the power to tax and responsibility to provide, public goods and services most appropriate to that level of government given the availability of information of resources and citizens’ preferences.

In parallel, a problem of optimal monetary decentralisation may be identified as that of allocating between an autonomous Central Bank and its regional or even State-level affiliates or subsidiaries, the power to finance through money-creation the deficits, if any, of the Union and State Governments respectively. It is not impossible to imagine a world in which individual State deficits did not flow into the Union deficit as a matter of course, but instead were intended to be financed more or less independently of the Union budget from a single-window source. There would be a clear conceptual independence between the Union and State levels of public action in the country. In such a world, the Union Government might approach a constitutionally autonomous national-level Central Bank to finance its deficit, while individual State Governments did something analogous with respect to autonomous regional or even State-level Central Banks which would be affiliates or subsidiaries of the national Central Bank.

This is similar to the intended model of the United States Federal Reserve System when it started 90 years ago, though it has not worked like that, in part because of the rapid rise to domination by the New York Federal Reserve relative to the other 11 regional Federal Reserve Banks.

A more radical monetary step would be to contemplate a “Reverse Euro” model by which a national currency issued by the national-level Central Bank acts in parallel with a number of regional or State-level currencies with full convertibility and floating exchange-rates guaranteed between all of them in a world of unhindered mobility of goods and factors.

However, these are very incomplete and theoretical thoughts which perhaps deserve to be shelved for the time being.[1] What necessitates this kind of discussion is after all not something theoretical but rather the practical ground realities of our country’s fiscal and monetary position, something of which this audience will be far better aware than am I.

Economic and political analysis suggests that managing a process of public financial decision-making requires a coincidence of the people who have the best information with the people who have the authority to act. In other words, decision-makers need to have relevant, reliable and timely information made available to them, and then they need to be considered accountable for the decisions made on that basis.

In a democracy like ours, the locus of economic policy decision-making must be Parliament and the State legislatures. Academics, civil servants, journalists, special interest groups, this or that business or industrial lobbyist or foreign management consultant can all have their say — but consensus on the direction and nature of economic policy, if it is to be genuine, has to ultimately emerge out of the legislative process on the basis of reasonable, well-informed discussion and debate, given full relevant timely information. The proper source of all economic policy decisions and initiatives is Parliament, the State legislatures and local government bodies — not this or that lobby or interest-group which may be vocal or powerful enough to be heard at a given time in New Delhi or some State capital-city.

Our 1950 Constitution was a marvellous document in its time and it has worked tolerably well. It defined the functions of government in India in accordance with the main parameters of normative public finance.

Economics ascribed a quite extensive traditional role to Government, the most important functions being collective and individual security, followed by all activities which in the words of Adam Smith,

“though they may be in the highest degree advantageous to a great society, are, however, of such a nature that the profit could never repay the expence to any individual or small number of individuals, and which it, therefore, cannot be expected that any individual or small number of individuals should erect or maintain.” (Wealth of Nations, V.i.c., 1776)

Our 1950 Constitution defined the Union’s responsibilities to be

External Security;

Foreign Relations & Trade;

Supreme Court & Domestic Security;

Debt Service, Foreign & Domestic;

National Infrastructure;

Communications & Broadcasting;

Atomic Energy;

Public Sector Industries;

Banking; Currency & Finance;

Archives; Surveys & National Institutions;

National Universities;

National Civil Services & Administration.

Each State’s responsibilities were

High Courts & Lower Judiciary;

Police; Civil Order; Prisons;

Water; Sanitation; Health;

State Debt Service;

Intra-State Infrastructure & Communications;

Local Government;

Liquor & Other Public Sector Industries; Trade; Local Banking & Finance;

Land; Agriculture; Animal Husbandry;

Libraries, Museums, Monuments;

State Civil Service & Administration.

Some duties were supposed to be shared by the Union with each State, including

Criminal Law;

Civil & Family Law, Contracts & Torts;

Forests & Environmental Protection;

Unemployment & Refugee Relief;

Electricity;

Education.

But the authors of the 1950 Constitution could not have envisaged the nature of present problems, or foreseen in those early years what we would have become like today. Our fiscal system has become such that a few clauses may have led to an impossibly complex centralization of fiscal power and information. Not only did the 1950 Constitution identify agendas of the Union and State Governments, it also dictated the procedure of decision-making and it is this which may have become intractable over 50 years. Under Article 280, a Finance Commission is appointed every five years whose task is to try to efficiently and equitably allot tax revenues collected by the Union downwards to the States and laterally between the States. Members of Finance Commissions have been elder statesmen of high reputation and integrity, yet the practical impossibility of their task has made their actions seem to all observers to be clouded in mystery and perhaps muddle. As one recent member, Justice Qureshi, has candidly stated

“it is humanly impossible for a person to understand the problems of the Centre and the 25 States and take a decision thereon within such a short time” (Ninth Finance Commission, Issues and Recommendations, p.350).

No matter how competent or well-meaning a Finance Commission’s members may be, their purpose may be stymied by the overload of information and overcentralisation of authority that has come to take place. As a result, it may have been inevitable that Government has ended up doing what it need not have done at the expense concomitantly of failing to do what only Government could or must have done.

The present situation is such that, despite the best efforts of the Reserve Bank and other Government agencies, there may be a gross lack of timely, relevant and reliable information reaching all decision-makers including the ordinary citizen, who as voter and taxpayer is the cornerstone of the fiscal system. My own inquiry started when Mr. Hubert Neiss, then Central Asia Director at the IMF, hired me as a consultant in December 1992. He told me the IMF was naturally concerned about India’s national budget deficit, but no one seemed to quite know how this related precisely to the budgets of the different States whose deficits seemed to be flowing into it. By its terms of reference, the IMF could not inquire into India’s States’ budgets and I did not do so in my work with them, but the import of his question remained in my thinking. Later I found similar questions being asked at the World Bank. I do not think it a great secret to state that there may be a great deal of simple puzzlement about the workings of our fiscal and monetary system on the part of observers and decision-makers who may be concerned about India’s fiscal position.

Among both public decision-makers and ordinary citizens right across the length and breadth of our country, a severe and widespread lack of information about and comprehension of India’s basic fiscal and monetary facts seems to exist. This in itself may be a cause of fiscal problems as citizens may not be adequately aware of the link between making their demands for public goods and services on the one hand, and the necessity of finding the resources to fund these goods and services on the other.

In any ultimate analysis, resources for public goods and services in an economy can be found only by diverting the real resources of individual citizens towards public uses. Other than printing fiat money, a national Government can only either tax those citizens who are present today in the population, or, borrow from the capital stock on behalf of unborn generations of future citizens.

West Europe and America are heirs to a long history of political development; yet even there, as Professor James Buchanan has often observed, the idea until has not been grasped until recently that benefits from use of public goods and services are supposed to accrue to citizens from whom resources have been raised. Until the 19th Century,

“government outlay was frequently considered “unproductive”, and there was, by implicit assumption, no return of services to the citizens who were taxed. In a political regime that devotes the bulk of government outlay to the maintenance expenses of a single sovereign, or even of an elite, there is no demonstrable return flow of services to the taxpayers…. Tax principles were discussed as if, once collected, revenues were removed forever from the economy; taxpayers, both individually and in the aggregate, were held to suffer real income loss” (James M. Buchanan, The Demand and Supply of Public Goods, Rand 1968, p. 167).

According to Buchanan, such an undemocratic fiscal model was transformed in the work of the great Swedish economist Knut Wicksell and others by introducing the key assumption of fiscal democracy, namely, that

“those who bear the costs of public services are also the beneficiaries in democratic structures”

Conversely, we may say those who demand public goods and services in a fiscal democracy should also expect to pay for them in real resources. If citizens are aware of taxes only as a burden and come to feel they receive little or nothing from Governments in return, there is a loss of incentive to pay taxes or to stand up and be counted as proud citizens of the country. There is an incentive instead to evade taxes or to flee the country or to cynically believe everything to be corrupt. On the other hand, if citizens demand public goods and services without expecting to contribute resources for their production, this amounts to being no more than a demand to be a free-rider on the general budget.

In our country, we may have been seeing both phenomena. On one hand, there is, rightly or wrongly, a tremendous public cynicism present almost everywhere with respect to expecting effective provision of public goods and services. On the other hand, the idea that the beneficiaries of public goods and services must also, sooner or later, come to bear the costs in terms of taxed resources is far from established so our politics come to often be unreasonable and irresponsible.

Reliable and comprehensible information about the system as a whole and about the contents of public budgets is thus vital for a fiscal democracy to function. In ancient Athens it was said:

“Here each individual is interested not only in his own affairs but in the affairs of the State as well; even those who are mostly occupied with their own business are extremely well-informed on general politics — this is a peculiarity of ours: we do not say that a man who has no interest in politics is a man who minds his own business; we say that he has no business here at all.” Pericles (Funeral Oration, Thucydides, The Pelopennesian War)

That was the criterion that Pericles defined for ancient Athenian democracy, and I see no reason why in the 21st Century it cannot be met in modern India’s democracy.

This finally brings me to the positive contribution I have promised to make. The aim my attempt to redesign the Union and State’s budgets utilising precisely the same data as available has been to make the fiscal position of all public entities accessible to any interested citizen.

We do not have to say that every Indian citizen, or even every literate and numerate citizen of our country, has to be able to understand the intricacies of the public budgets of his or her State and the Union. But if information is available such that anyone who understands the finances of his own family or his own business enterprise is also reasonably able to understand the public budget then a standard of maximum feasible transparency would have been defined and met.

I have relied on the international normative model developed by our own countryman, Mr. A. Premchand, who retired from the IMF a few years ago, as described in his outstanding book Effective Government Accounting (IMF 1995), where he showed applications for e.g. the USA, New Zealand and Switzerland. What I have done – or rather did in 1997/1998, with the help of a research assistant and a student – is apply that to all of our States and the Union too.[2] What will be seen by way of differences with the present methodology is that there is essentially an Operating Statement, a Financial Statement and a Cash Flow Statement offered for each State and the Union. The financial position and gross fiscal deficit definition emerge rather neatly from this – while there the rather confusing “Development/Non-development” and “Planning/Non-Planning” distinctions have been done away with.

The exercise points to the foundations of a new and fresh federal framework for our Republic. A central new fact of modern India is that many, perhaps most, of our States have developed what is effectively a bipolar division in their legislatures. Voters have also increasingly started to judge Governments not by the personalities they contain but rather by their performance on the job, and, at election-time, have begun to frequently enough shown one side the door in the hope the other side may do better. In such circumstances, there seems no reason in principle why an entity as large as the average State of modern India today cannot be entrusted to legislate and administer a modern tax-system, based especially on the income-tax, and especially taxing income from all sources including agriculture. In a fresh and modern federalism, an elected State Government would have appropriate economic powers to run its own affairs, and be mainly accountable to the legislature whose confidence it requires, and ultimately to voters below.

From an efficiency standpoint, we should want a framework in which repercussions of political turmoil or bad financial management by a State Government to not spill into other States or flow into the Union Government’s own problems of deficit financing. With free mobility of goods and factors throughout the Union, citizens faced with a poorly performing State Government could seek to vote it out of office, or may of course “vote with their feet” by moving their capital or resources to another part of the country. In short, State Governments will be held responsible by their electorates for their expenditures on public goods and services, while having the main powers of domestic taxation in the economy, especially taxes on income from all sources including agriculture.

At the same time, diverse as India is, we are not 15 or 25 separate republics federated together but rather one country all of whose peoples are united by a common geography and a common experience of history. From an equity and indeed national standpoint, we may also want a system which also firmly established that the National Parliament would have to determine how much each citizen should be taxed for the Union to provide public goods and services for the country as a whole, as well as what transfers ought to be made between the States via the Union in the interests of equity given differences in initial resource-endowments between them.

Here again an American example may be useful. As is well-known, the 50 United States each have their own Constitutions governing most intra-State political matters, yet all being inferior in authority to the 1789 Constitution of the United States as duly amended. In India, an author as early as 1888 recommended popular Constitutions for India’s States on the grounds

“where there are no popular constitutions, the personal character of the ruler becomes a most important factor in the government… evils are inherent in every government where autocracy is not tempered by a free constitution.”[3]

We could ask if a better institutional arrangement may occur by each State of India electing its own Constitutional Convention subject naturally to the supervision of the National Parliament and the obvious provision that all State Constitutions be inferior in authority to the Constitution of the Union of India.[4] These documents would then furnish the major sets of rules to govern intra-State political and fiscal decision-making more efficiently. An additional modern reason can be given from the work of Professor James M. Buchanan, namely, that fiscal constitutionalism, and perhaps only fiscal constitutionalism, allows over-riding to take place of the interests of competing power-groups.[5]

State-level Constitutional Conventions in India would provide an opportunity for a realistic assessment to be made by State-level legislators and citizens of the fiscal positions of their own States. Greater recognition and understanding of the plain facts and the desired relationships between income and expenditures, public benefits and public costs, would likely improve the quality of public decision-making at State-levels, sending public resources from destinations which are socially worthless towards destinations which are socially worthwhile. It bears repeating the average size of a large State of India is 61 million people, and almost all existing political Constitutions around the globe furnish rules for far smaller populations than that.

Thank you for your patience. Jai Hind.

[1] Monetary Federalism at Work: F. A. Hayek more than anyone else taught us that relative prices are signals or guides to economic activity — summarizing in a single statistic information about the resources, constraints, expectations and ambitions of market participants. An exchange-rate between two currencies is also a relative price, conveying information about relative market opinions regarding the issuers of the two currencies. Suppose we had two States of India in the fresh kind of federal framework outlined above, which were identical in all respects except one had a larger deficit and so a larger nominal money supply growth. Would that mean the first currency must depreciate relative to the second? Not necessarily; it is not the size of indebtedness that matters but rather the quality of public investment decisions, to which borrowed money has been put. Thus we come to the crux: Suppose we have two States which are identical in all respects except one: State X is found to have an efficient Government, i.e. one which has made relatively good quality public investment decisions, and State Y is found to have one which has made relatively bad quality public investment decisions. In the present amalgamated model of Indian federal finance, no objective distinction can be made between the two, and efficient State Governments are surreptitiously compelled to end up subsidising inefficient ones. In a differentiated federal framework for India, as the different information about the two State Governments comes to be discovered, the X currency will tend to appreciate as resources move towards it while the Y will tend to depreciate as resources move away from it. In an amalgamated model, efficient State Governments lose incentives to remain efficient, while in a differentiated model, inefficient State Governments will gain an incentive not to be inefficient. The present amalgamated situation is such that inefficient States – and this may include not only the State Government but also the State Legislature and the State electorate itself – receive no fiscal incentive to improve themselves. In a differentiated framework, the same inefficient State would face a tangible, visible loss of reserves or depreciation of its currency relative to other States on account of its inefficiency, and thereby have some incentive to mend its ways. I call the proposal given here a “Reverse Euro” model because Europe appears to be moving from differentiated currencies and money supplies to an amalgamated currency and money supply, while the argument given here for India is in the opposite direction. Professor Milton Friedman of the Hoover Institution at Stanford, has had the kindness, at the age of 88, to send me a brilliant and forceful critique of my Reverse Euro idea for India when I requested his comment. Since he is the founder of the flexible exchange-rate system and he has found it too radical, I have shelved it for the time being.

[2] The assistance of Dola Dasgupta and K. Shanmugam is recorded with gratitude.

[3] Surendranath Roy, A History of the Native States of India, Vol I. Gwalior, Calcutta & London: Thacker 1888.

[4] Large amounts of legal and constitutional precedent have built up on issues of a regional or local nature: whether a State legislature should be unicameral or bicameral, what should be its procedures, what days should be State holidays but need not be national holidays, on tenancy, rent control, school standards, health standards and so on ad infinitum. All this body of explicit and implicit local rules and conventions may be duly collected and placed in State-level Constitutions.

[5] James M. Buchanan, Limits to Liberty, Texas, 1978.

A major expansion and reorganization of the judiciary would have to accompany the sort of basic constitutional reform outlined above. Union and State judiciaries would need to be more clearly demarcated, and rules established for review of State-level decisions by Union courts of law. It is common knowledge the judiciary in India is in a state of organizational overload at the point of collapse and dysfunction. An expansion and reorganization of the judiciary to match new Union-State constitutional relations will likely improve efficiency, and therefore welfare levels of citizens.