First published in The Sunday Statesman, Feb 11 2007, The Statesman, Feb 12 2007

Editorial Page Special Article

TWO and a half millennia ago, the Greeks described how brightly coloured textiles imported from India were popular among the Persians. Five centuries later, the Roman historian Pliny complained that India every year “took from Italy a hundred million sesterces in return for spices, perfumes and ornaments”. Montesquieu observed in 1748: “All peoples who have traded with India have always taken metals there and brought back commodities. Indians need only our metals, which are the signs of value. In all times those who deal with India will take silver there and bring back none”.

During the British period, India remained a great trading nation. JM Keynes found Britain, the world’s largest exporter in 1913, exporting more to India than anywhere else, and Germany, the world’s fastest growing economy in 1913, receiving 5 percent of its imports from India and sending it 1.5 percent of exports, making India the sixth largest exporter to Germany (after the USA, Russia, Britain, Austria-Hungary, France) and eighth largest importer from it (after Britain, Austria-Hungary, Russia, France, the USA, Belgium, Italy). India’s share of world exports during 1870-1914 may have been about 3-4 per cent. As of 1917-1918, India’s balance of payments and fiscal budget appear idyllic: an export surplus of £61.42 million, official reserves of £66.53 million, total claims on the rest of the world of £127.5 million (or 32.85 million troy ozs of gold), and a 1916-1917 budget surplus of £6,594,885.

Even at mid-20th Century, India was still a trading power with 2 percent of world exports and a rank of 16 in the world economy after the USA, Britain, West Germany, France, Canada, Belgium, Holland, Japan, Italy, Australia, Sweden, Venezuela, Brazil, Malaya and Switzerland.

Yet during the second half of the 20th Century, the Indian subcontinent collapsed to near insignificance in world trade and payments. The traditional export surplus implied a high “treasure” demand for precious metals on capital account; this was reversed and the new India became a chronic trade-deficit country dependant on foreign borrowings and grants. Of world merchandise exports, the subcontinent’s share today is 0.8 of 1 per cent, and of Asia’s 6 percent (India accounting for two thirds); by contrast, Malaysia alone accounts for 0.9 of 1 percent of world exports and 6.5 percent of Asia’s. Most poignantly, among 11 major developing countries (Korea, Taiwan, Singapore, Hong Kong, Argentina, Brazil, Chile, Mexico, Israel, Yugoslavia), India’s share of manufactured exports to the world fell from 65 per cent in 1953 to 51 percent in 1960 to 31 per cent in 1966 to 10 per cent by 1973. Our legendary textiles lost ground steadily. As of 1962-1971, India held an average annual market-share of almost 20 percent of manufactured textile imports into the USA; this fell to 10 percent by 1972-1981 and less than 5 percent by 1982-1991. India’s share of Britain’s imports of textile manufactures fell from 16 per cent in the early 1960s to less than 4 per cent in the 1990s. India and Sri Lanka once dominated world tea exports but lost rapidly to Kenya, Indonesia and Malawi. Of total British tea imports, Sri Lanka’s market-share fell from 11 percent in 1980 to 7 per cent by 1991 while India’s fell from 33 percent in 1980 to 17 per cent by 1991. Today India may not be in the top thirty largest merchandise exporting countries of the world.

Several causes may be identified for our historical collapse in world trade and payments. These include Western protectionism e.g. of domestic textiles between 1965-2005, and emergence of new technologies like synthetic fibres, plastics, tea-bags etc as well as new competitors in the world marketplace willing to use these. Successful commerce depends on intangible quantities like trust, reliable information and contacts between individual contracting parties. Decline in our shares of world exports led to wastage of such informational capital and commercial trust. Foreign importers established new relations with India’s competitors, and for Indian entrepreneurs (now facing lessened foreign protectionism or newly liberalized domestic policies) to win new customers or win back old ones becomes doubly difficult.

But the most important cause of the decline was undoubtedly the political discord and trauma leading to economic disintegration of Old India into modern India, Pakistan, Sri Lanka and Bangladesh. Partly as a result of their conflict, independent India and Pakistan deepened government requisitioning and rationing of foreign exchange purportedly as part of pseudo-socialist “planning”.

Trade policy followed the British pattern of import quotas imposed to conserve hard currency and save shipping space during war. Discretionary controls were in place by 1942 on grounds of “essentiality” and non-availability from indigenous sources. War needs over-rode others, and consumer goods banned ~ favouring their production by domestic business houses. In 1945 consumer goods were placed on open general license, as “the pattern of post-war trade should not be dictated by perpetuation of controls set up for purely war-time purposes”, and in 1946 there was further liberalization in view of India’s enormous sterling balances. But by March 1947 this ended, and import of gold and 200 “luxury” goods were banned. Only a few “essential” goods remained on the open list.

After the British left, political/bureaucratic control of imports and foreign exchange were extended, not removed. Intricate restrictions, subsidies, barriers and import-licensing (based on obsolete war-time “essentiality” and “actual user” criteria) continued, now in name of “import-substitution” and “planning”. Major industries were nationalized, and these became leading consumers of imports obtained by administrative rationing of the foreign exchange earned by export sectors. As consumer goods’ imports were most restricted, Indian businesses predictably diverted to produce these in the large highly protected domestic markets that resulted, causing monopolistic profits and financing of a vast parallel or “black” economy with its thriving hawala sector. Restriction of consumer goods’ and gold imports also caused smuggling and open corruption in Customs. The international price of the rupee was viewed not as reflecting demand for foreign relative to domestic moneys but as just another administered price to be used by politicians and bureaucrats. Foreign exchange earnings of exporters were confiscated in exchange for rupees at the administered rate. Foreign currency thus requisitioned was (and still mostly is) disbursed by rationing in the following order of precedence: first to meet Government debt repayments to international organizations, and Government expenditures abroad like maintenance of embassies and purchase of military imports, plus politicians’ and bureaucrats’ foreign travel etc; secondly, for import of food, fertilizers, petroleum; thirdly, for imported inputs required by Government firms; fourthly, for import demands of those private firms successful in obtaining import licenses; lastly, to satisfy demands of the public at large for purposes like travel or study abroad.

After devaluing with sterling in 1949, the rupee was maintained at the same value for 17 years despite weakening reserve positions and numerous shocks to the economy like the 1962 war with China, 1965 war with Pakistan, and droughts and food crises. Devaluation on June 6 1966 to Rs. 7.50 per US dollar met political opposition and contributed to Congress Party losses in the 1967 elections. The rupee did not respond to sterling’s devaluation in November 1967 and was not adjusted downwards though the economy continued to suffer shocks like the rise in petroleum prices, refugees from the Pakistan civil war, and domestic strikes and political instability. In August 1971, India pegged to the dollar and devalued with the dollar’s depreciation but in December again linked to sterling at Rs 18.97. When sterling depreciated after floating in June 1972, the rupee effectively devalued with it, and until July 1975 there were three small devaluations against sterling. In September 1975, India pegged (within margins) to an undisclosed basket of hard currencies including the dollar, yen and deutschmark, and between 1981-1985, the rupee was slowly managed downwards, without political resistance. From September 1985-July 1991, it followed a more rapid downward course depreciating 40 per cent, while the dollar depreciated as well against major currencies, suggesting the dollar weighed heavily in the basket to which the rupee was pegged.

1991 reforms

Narasimha Rao, P Chidambaram and others received from Rajiv Gandhi in his last months the results of a “perestroika-for-India” project, and started a process of economic liberalisation. Chidambaram said at the time the reforms “were not miraculous” but based on rewriting the Congress manifesto: “We were ready when we came back to power in 1991”.

On July 1 1991, the rupee devalued 9 percent and on July 3 a further 11 percent. The new Government’s March 1 1992 Budget placed the rupee experimentally on a dual rate, implicitly taxing exporters who had to surrender 40 percent of their forex at an officially determined rate and could sell 60 percent in an open market. On March 1 1993, the rupee began to be made convertible for current account transactions, i.e. for import and export of goods and services. Trade reforms included removing many import quotas and some export subsidies. But grave fiscal and monetary problems were not (and have never been) addressed with any seriousness.

Balance of payments

The “balance of payments” sums a country’s current and capital accounts. In Western countries, the capital account consists of net trading in long and short-term securities like private stock and government debt ~ domestic securities being bought and sold freely by foreign residents and foreign securities by domestic residents. Prices determined by competitive trading are very sensitive to interest-rate differences. In India (and Pakistan etc) genuine capital account transactions have not existed since the 1930s, and do so only in highly distorted form even today. The traditional export surplus and positive current account, balanced by net inflow of precious metals, had been wiped out and current account deficits were coupled with overvalued currencies and closed capital markets – along with repressive financial policies causing capital flight of an elite nomenklatura. The inherent risk of unproductive use of funds by borrowers and consumers of forex (mostly Government) were shifted to export and other hard-currency earning sectors.

In particular, a severe trade-deficit had followed petroleum-price rises in the late 1970s, which continues today. There has been some exploration, discovery and extraction of domestic supplies of oil and gas, but no significant move to conserve or find economical alternatives to use of imported energy. (Indeed a coal-exporting petroleum-importing nation with the most heavily used railways in the world made an unprovoked decision to abolish steam-locomotives in favour of diesel and electric. And now, very expensive foreign nuclear plants are planned to be imported on a turnkey basis under a false assumption these will help India’s energy sector.)

India gained from exporting temporary workers to the Gulf since the 1970s but that could hardly finance the increased oil bill. Instead there has been large growth of foreign debt since the 1970s, mostly owed by the Government (and recently by large private businesses) to Western financial markets via brokerage of Western governments and organizations they control. India’s foreign debt amounts to more than $100 being owed by each of our one billion citizens, each of us having to earn five or six dollars every year on average just to meet interest payments due to foreign creditors.

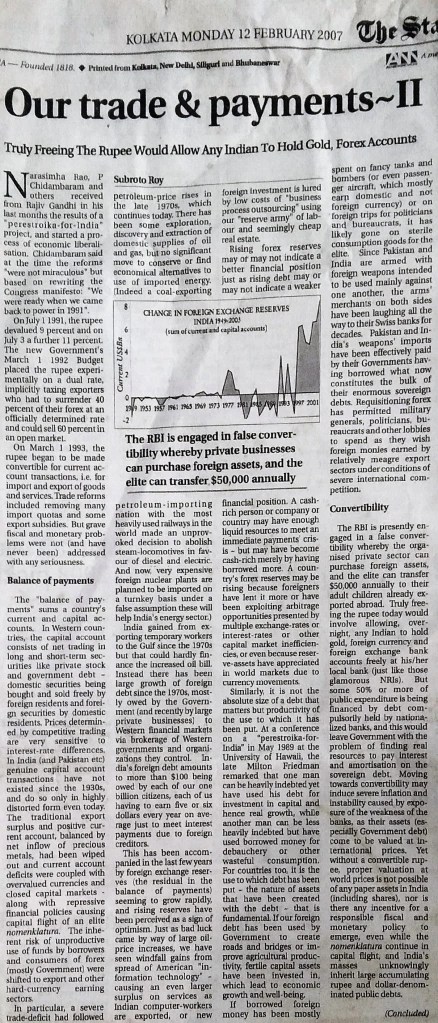

This has been accompanied in the last few years by foreign exchange reserves (the residual in the balance of payments) seeming to grow rapidly, and rising reserves have been perceived as a sign of optimism. Just as bad luck came by way of large oil-price increases, we have seen windfall gains from spread of American “information technology” ~ causing an even larger surplus on services as Indian computer-workers are exported, or new foreign investment is lured by low costs of “business process outsourcing” using our “reserve army” of labour and seemingly cheap real estate.

Rising forex reserves may or may not indicate a better financial position just as rising debt may or may not indicate a weaker financial position. A cash-rich person or company or country may have enough liquid resources to meet an immediate payments’ crisis ~ but may have become cash-rich merely by having borrowed more. A country’s forex reserves may be rising because foreigners have lent it more or have been exploiting arbitrage opportunities presented by multiple exchange-rates or interest-rates or other capital market inefficiencies, or even because reserve-assets have appreciated in world markets due to currency movements.

Similarly, it is not the absolute size of a debt that matters but productivity of the use to which it has been put. At a conference on a “perestroika-for-India” in May 1989 at the University of Hawaii, the late Milton Friedman remarked that one man can be heavily indebted yet have used his debt for investment in capital and hence real growth, while another man can be less heavily indebted but have used borrowed money for debauchery or other wasteful consumption.

For countries too, it is the use to which debt has been put ~ the nature of assets that have been created with the debt ~ that is fundamental. If our foreign debt has been used by Government to create roads and bridges or improve agricultural productivity, fertile capital assets have been invested in, which lead to economic growth and well-being.

If borrowed foreign money has been mostly spent on fancy tanks and bombers (or even passenger aircraft, which mostly earn domestic and not foreign currency) or on foreign trips for politicians and bureaucrats, it has likely gone on sterile consumption goods for the elite. Since Pakistan and India are armed with foreign weapons intended to be used mainly against one another, the arms’ merchants on both sides have been laughing all the way to their Swiss banks for decades. Pakistan and India’s weapons’ imports have been effectively paid by their Governments having borrowed what now constitutes the bulk of their enormous sovereign debts. Requisitioning forex has permitted military generals, politicians, bureaucrats and other lobbies to spend as they wish foreign monies earned by relatively meagre export sectors under conditions of severe international competition.

False convertibility

The RBI is presently engaged in a false convertibility whereby the organised private sector can purchase foreign assets, and the elite can transfer $50,000 annually to their adult children already exported abroad. Truly freeing the rupee today would involve allowing, overnight, any Indian to hold gold, foreign currency and foreign exchange bank accounts freely at his/her local bank (just like those glamorous NRIs). But some 50% or more of public expenditure is being financed by debt compulsorily held by nationalized banks, and this would leave Government with the problem of finding real resources to pay interest and amortisation on the sovereign debt. Moving towards convertibility may induce severe inflation and instability caused by exposure of the weakness of the banks, as their assets (especially Government debt) come to be valued at international prices. Yet without a convertible rupee, proper valuation at world prices is not possible of any paper assets in India (including shares), nor is there any incentive for a responsible fiscal and monetary policy to emerge, even while the nomenklatura continue in capital flight, and India’s masses unknowingly inherit large accumulating rupee and dollar-denominated public debts.

The search engine above should locate any article by its title; the Index and Archives may be used as well.

Readers are welcome to quote from my work under the normal “fair use” rule, but please try to quote me by name and indicate the place of original publication in case of work being republished here. I am at Twitter @subyroy, see my latest tweets above

Leave a comment