Mistaken Macroeconomics: An Open Letter to Prime Minister Dr Manmohan Singh 12 June 2009

June 12, 2009 — drsubrotoroywhere g is defined to be the rate of growth (Y t+1-Yt)/Yt .

The Indian Revolution

December 8, 2008 — drsubrotoroyThe Indian Revolution

by

Subroto Roy

Prefatory Note Dec 2008: This outlines what might have happened if (a) Rajiv Gandhi had not been assassinated; (b) I had known at age 36 all that I now know at age 53. Both are counterfactuals and hence this is a work of fiction. It was written long before the Mumbai massacres; the text has been left unchanged.

“India’s revolution, when it came, was indeed bloodless and non-violent but it was firm and clear-headed and inevitably upset a lot of hitherto powerful people.

The first thing the Revolutionary Government declared when it took over in Delhi was that the rupee would become a genuine hard currency of the world economy within 18 months. This did not seem a very revolutionary thing to say and the people at first did not understand what was meant. The Revolutionaries explained: “Paper money and the banks have been abused by all previous regimes ruling in Delhi since 1947 who learnt their tricks from British war-time techniques. We will give you for the first time in free India a rupee as good as gold, an Indian currency as respectable as any other in the world, dollar, pound, yen, whatever. What you earn with your hard work and resources will be measured by a sound standard of value, not continuously devalued in secret by government misuse”.

The people were intrigued but not enlightened much. Nor did they grasp things to come when the Revolutionary Government abolished the old Planning Commission, sending its former head as envoy to New Zealand (with a long reading-list); attached the Planning Commission as a new R&D wing to the Finance Ministry; detached the RBI from the Finance Ministry; instructed the RBI Governor to bring proper work-culture and discipline to his 75,000 staff and instructed the Monetary Policy Deputy Governor to prepare plans for becoming a constitutionally independent authority, besides a possible monetary decentralization towards the States. India’s people did not understand all this, but there began to be a sense that something was up in Lutyens’ Delhi faraway.

The Revolutionary Government started to seem a little revolutionary when it called in police-chiefs of all States — the PM himself then signed an order routed via the Home Ministry that they were to state in writing, within a fortnight, how they intended to improve discipline and work-culture in the forces they commanded. Each was also asked to name three reliable deputies, and left in no doubt what that meant. State Chief Ministers murmured objections but rumours swirled about more to come and they shut up quickly. The Revolutionary Government sent a terse note to all CMs asking their assistance in implementation of this and any further orders. It also set up a “Prison Reform and Reconstruction Panel” with instructions to (a) survey all prisons in the country with a view to immediately reduce injustices within the prison-system; (b) enlarge capacity in the event fresh enforcement of the Rule of Law came to demand this.

The Revolutionary Government then asked all senior members of the judiciary to a meeting in Trivandrum. There they declared the judiciary must remain impartial and objective, not show favoritism even to members of the Revolutionary Party itself who might be in court before them for whatever reason. The judges were assured of carte blanche by way of resources to improve quality of all public services under them; at the same time, a new “Internal Affairs Department” was formed that would assure the public that the Bench and the Bar never forgot their noble calling. When a former judge and a former senior counsel came to be placed in two cells of the new prison-system, the public finally felt something serious was afoot. Late night comics on TV led the public’s mirth — “Thieves have authority when judges steal themselves”, waxed one eloquently.

The Revolutionary Government’s next step reached into all nooks and crannies of the country. A large room in the new Finance Ministry was assigned to each State – a few days later, the Revolutionary Government announced it had taken over control under the Constitution’s financial emergency provision of all State budgets for a period of six months at the outset.

Now there was an irrepressible outcry from State Chief Ministers, loud enough for the Revolutionary Government to ask them to a national meeting, this time in Agartala. When the Delhi CM sweetly complained she did not know how to get there, she got back two words “Get there”; and she did.

There the PM told the CMs they would get their budgets back some day but only after the Revolutionary Government had overseen their cleaning and restoration to financial health from their current rotten state. “But Prime Minister, the States have had no physical assets”, one bright young CM found courage to blurt out.

“That is the first good question I have heard since our Revolution began,” answered the PM. “We are going to give you the Railways to start with — Indian Railways will keep control of a few national trains and tracks but will be instructed to devolve control and ownership of all other assets to you, the States. See that you use your new assets properly”. There was a collective whoop of excitement. “During the time your budgets remain with us, get your police, transport, education and hospital systems to work for the benefit of common people, confer with your oppositions about how you can get your legislatures to work at all. Keep in mind we are committed to making the rupee a hard currency of the world and we will not stand for any waste, fraud or abuse of public moneys. We really don’t want to be tested on what we mean by that. We are doing the same with the Union Government and the whole public sector”. The Chief Ministers went home nervous and excited.

Finally, the Revolutionary Government turned to Lutyens’ Delhi itself. Foreign ambassadors were called in one by one and politely informed a scale-back had been ordered in Indian diplomatic missions in their countries, and hence by due protocol, a scale-back in their New Delhi embassies was called for. “We are pulling our staff, incidentally, from almost all international and UN agencies too because we need such high-quality administrators more at home than abroad”, the Revolutionary Foreign Minister told the startled ambassadors.

Palpable tension rose in the national capital when the Revolutionary Government announced that Members of Parliament would receive public housing of high quality but only in their home constituencies! The MPs would have to vacate their Delhi bungalows and apartments! “But we are Delhi! We must have facilities in Delhi!”, MPs cried. “Yes, rooms in nationalized hotels suffice for your legislative needs; kindly vacate the bungalows as required; we will be building national memorials, libraries and museums there”, replied the radicals in power. Tension in the capital did not subside for weeks because the old political parties all had thrived on Delhi’s social circuit, whose epicenter swirled around a handful of such bungalows. Now those old power-equations were all lost. A few MPs decided to boycott Delhi and only work in their constituencies.

When the Pakistan envoy was called with a letter for her PM, outlining a process of détente on the USSR-USA pattern of mutual verification of demilitarization, both bloated militaries were upset to see their jobs and perks being cut but steps had been taken to ensure there was never any serious danger of a coup. The Indian Revolution was in full swing and continued for a few years until coherence and integrity had been forced upon the public finances and currency of a thousand million people….”

see also

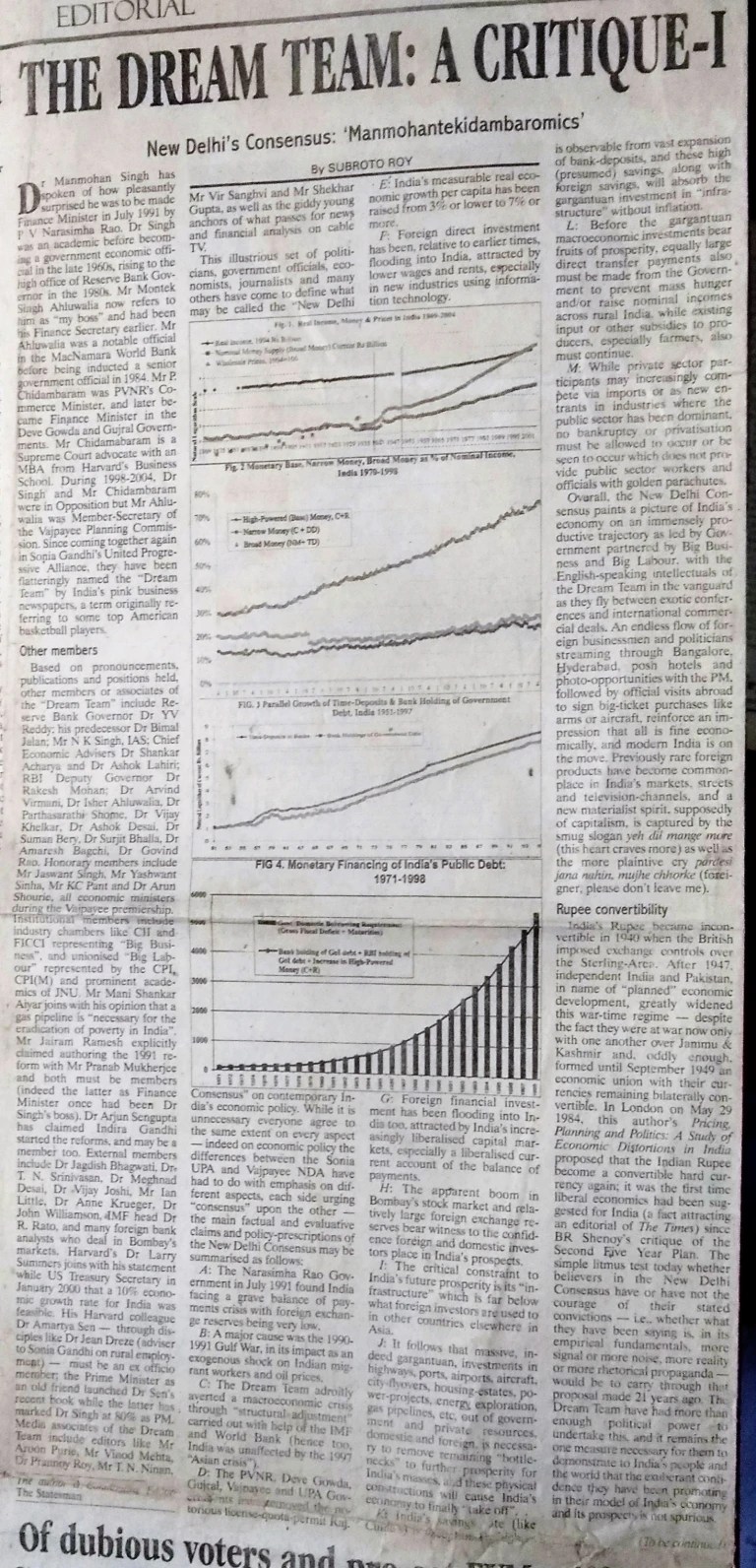

The Dream Team: A Critique (2006)

January 8, 2006 — drsubrotoroyThe Dream Team: A Critique

by Subroto Roy

First published in The Statesman and The Sunday Statesman, Editorial Page Special Article, January 6,7,8, 2006

(Author’s Note: Within a few weeks of this article appearing, the Dream Team’s leaders appointed the so-called Tarapore 2 committee to look into convertibility — which ended up recommending what I have since called the “false convertibility” the RBI is presently engaged in. This article may be most profitably read along with other work republished here: “Rajiv Gandhi and the Origins of India’s 1991 Economic Reform”, “Three Memoranda to Rajiv Gandhi”, “”Indian Money & Banking”, “Indian Money & Credit” , “India’s Macroeconomics”, “Fiscal Instability”, “Fallacious Finance”, “India’s Trade and Payments”, “Our Policy Process”, “Against Quackery”, “Indian Inflation”, etc)