My “Critique of Monetary Ideas of Manmohan & Modi: the Roy Model explaining to Bimal Jalan, Nirmala Sitharaman, RBI etc what it is they are doing” of 2019 is here.

Foundations of India’s Political Economy: Towards an Agenda for the 1990s edited by Subroto Roy & William E James, 1986-1992… pdf copy uploaded 2021

Pricing, Planning & Politics: A Study of Economic Distortions in India 1984, uploaded as pdf 2021

My Sep 2019 recommendation PM address each State Legislature, get all India Govt Accounting & Public Decision Making to have integrity; 16 May 2014 Advice scrap “Planning Commission”,integrate its assets with the Treasury, get the nationalised banks & RBI out of the Treasury

My critical assessment dated 23 August 2013 of Professors Jagdish Bhagwati & Amartya Sen and Dr Manmohan Singh is here…

My critique of PM Modi’s 8 November 2016 statement began on Twitter immediately, and is summarized here “Modi & Monetary Theory: Economic Consequences of the Prime Minister of India”

My critical assessment dated 19 August 2013 of Professor Raghuram Rajan is here and here.

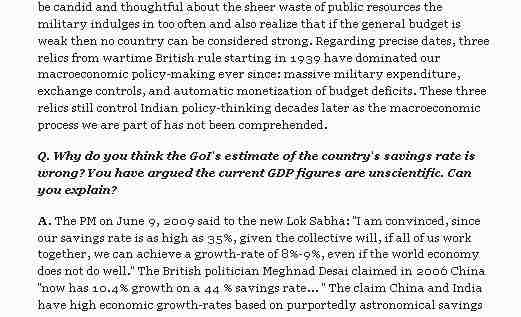

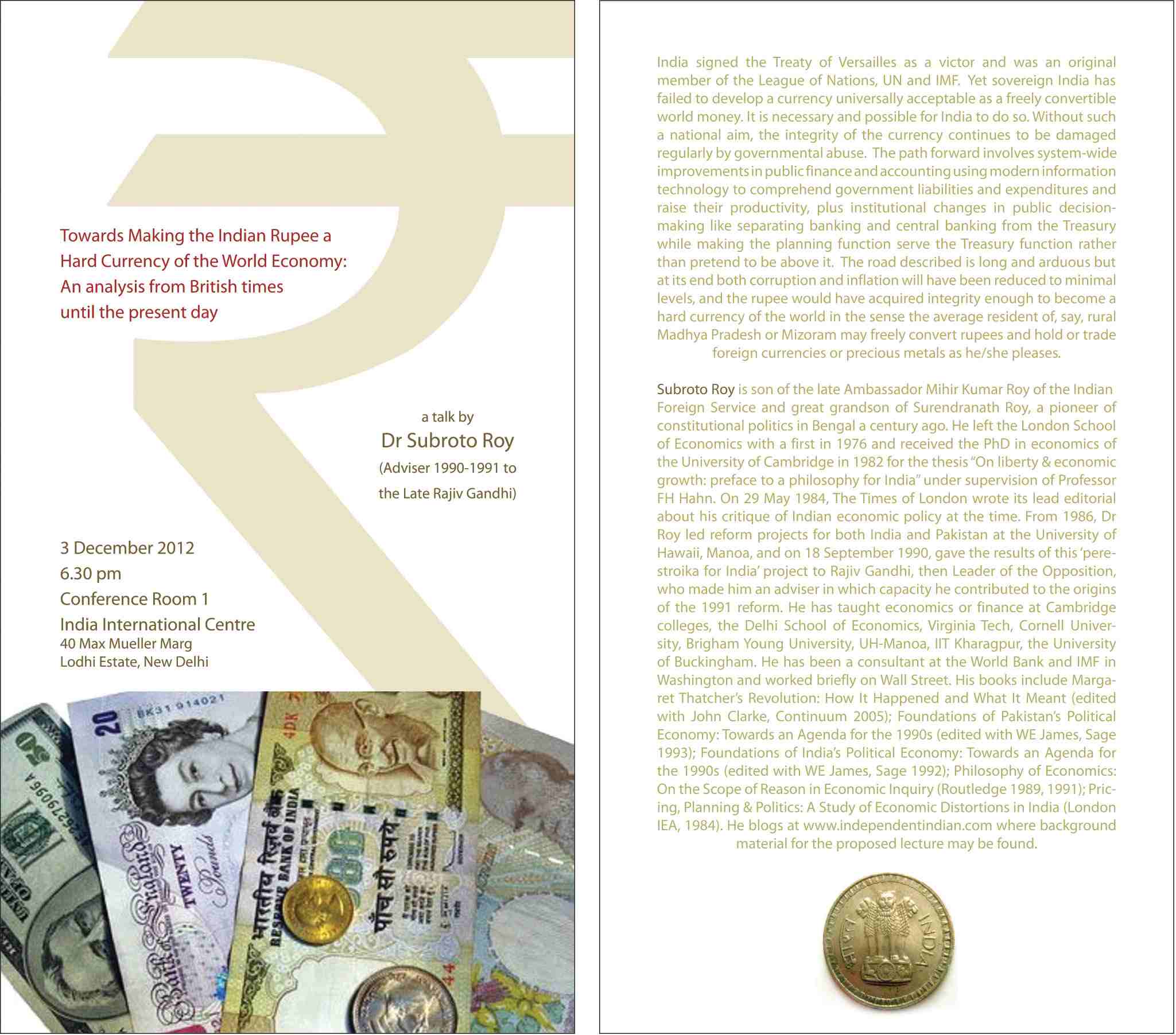

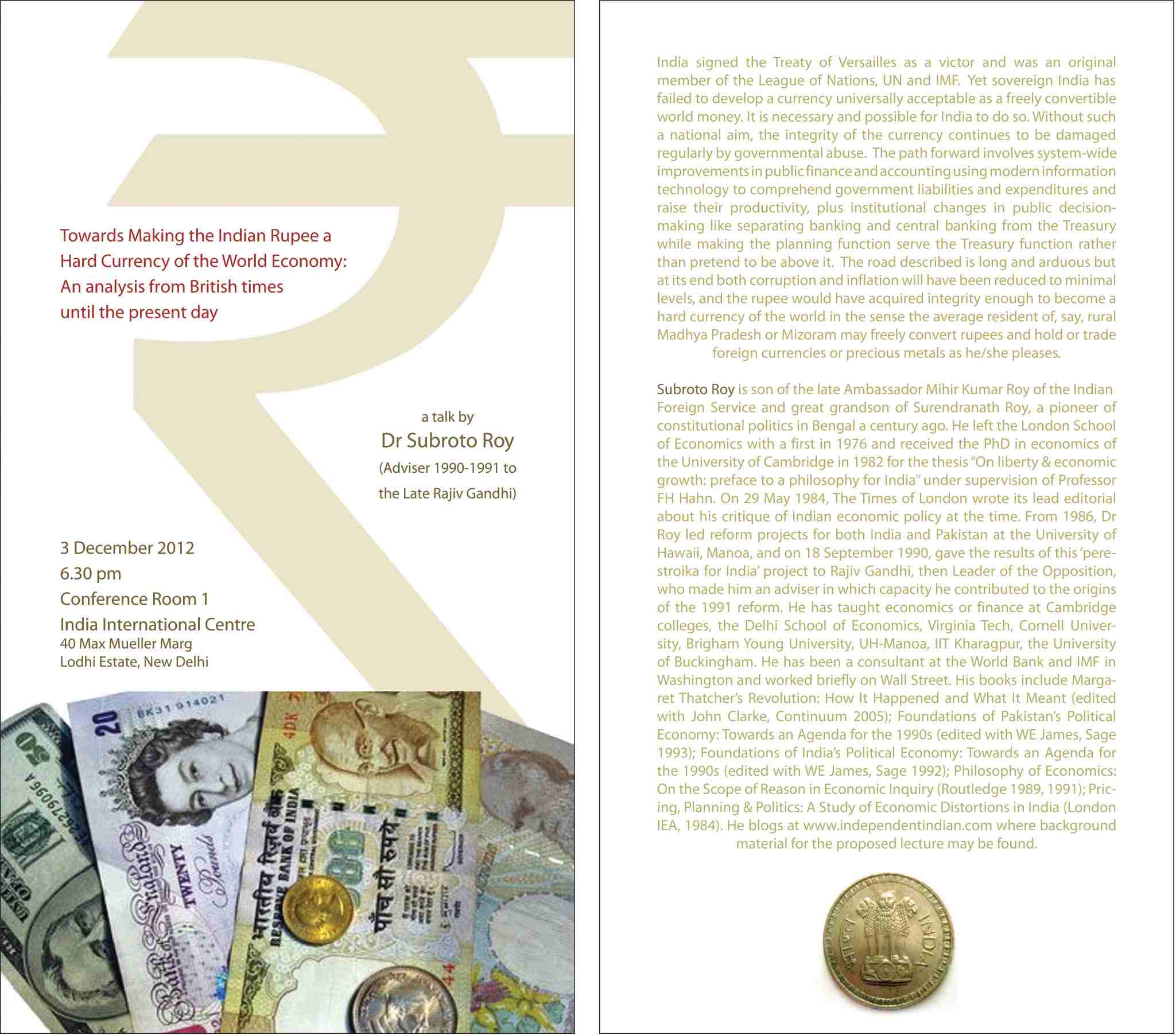

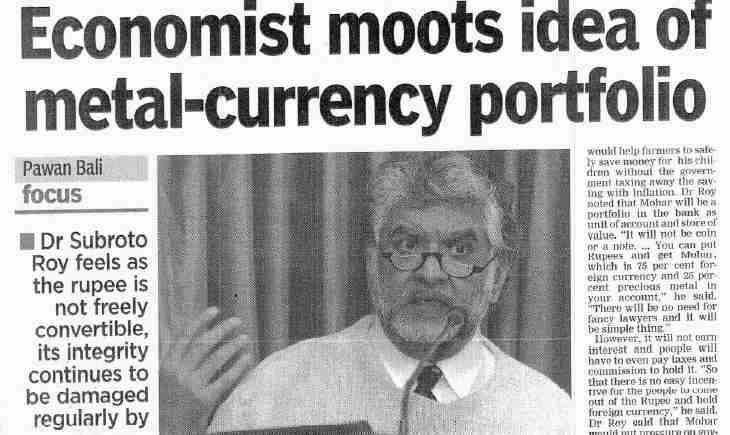

My 3 Dec 2012 Delhi talk on India’s Money is now available at You-Tube in an audio version here.

My July 2012 article “India’s Money” in the Caymans Financial Review is here and here https://independentindian.com/2012/07/21/my-article-indias-money-in-the-cayman-financial-review-july-2012/

My 5 December 2012 interview by Mr Paranjoy Guha Thakurta, on Lok Sabha TV, the channel of India’s Lower House of Parliament, broadcast for the first time on 9 December 2012 on Lok Sabha TV, is here and here in two parts.

My interview by GDI Impuls banking quarterly of Zürich published on 6 Dec 2012 is here.

My interview by Ragini Bhuyan of Delhi’s Sunday Guardian published on 16 Dec 2012 is here.

“Monetary Integrity and the Rupee” (2008)

https://independentindian.com/2008/09/28/monetary-integrity-and-the-rupee/

“India’s Macroeconomics” (2007)

“Fiscal Instability” (2007)

“Fallacious Finance” (2007)

https://independentindian.com/2007/03/05/fallacious-finance-the-congress-bjp-cpi-m-et-al-may-be-leading-india-to-hyperinflation/

https://independentindian.com/2021/12/01/on-the-simplest-smallest-most-universal-direct-flattax-of-500-rupees-per-annum-for-india-accruing-to-the-states-with-a-bpl-exemption-too/

Budgets & Financial Positions of Three of India’s Most Populous States (combined population c.300 million)…Brought to you especially by Dr Subroto Roy… Feel free to use (with acknowledgment)…

“Growth and Government Delusion” (2008)

https://independentindian.com/2008/02/22/growth-government-delusion/

“Distribution of Govt of India Expenditure (Net of Operational Income) 1995”

https://independentindian.com/2008/07/27/distribution-of-govt-of-india-expenditure-net-of-operational-income-1995/

“India in World Trade & Payments” (2007)

https://independentindian.com/2007/02/12/india-in-world-trade-payments/

“Path of the Indian Rupee 1947-1993″ (1993)

https://independentindian.com/1993/06/01/path-of-the-indian-rupee-1947-1993/

“Our Policy Process” (2007)

https://independentindian.com/2007/02/20/our-policy-process-self-styled-planners-have-controlled-indias-paper-money-for-decades/

“Indian Money and Credit” (2006)

https://independentindian.com/2006/08/06/indian-money-and-credit/

“Indian Money and Banking” (2006)

https://independentindian.com/2006/04/23/indian-money-and-banking/

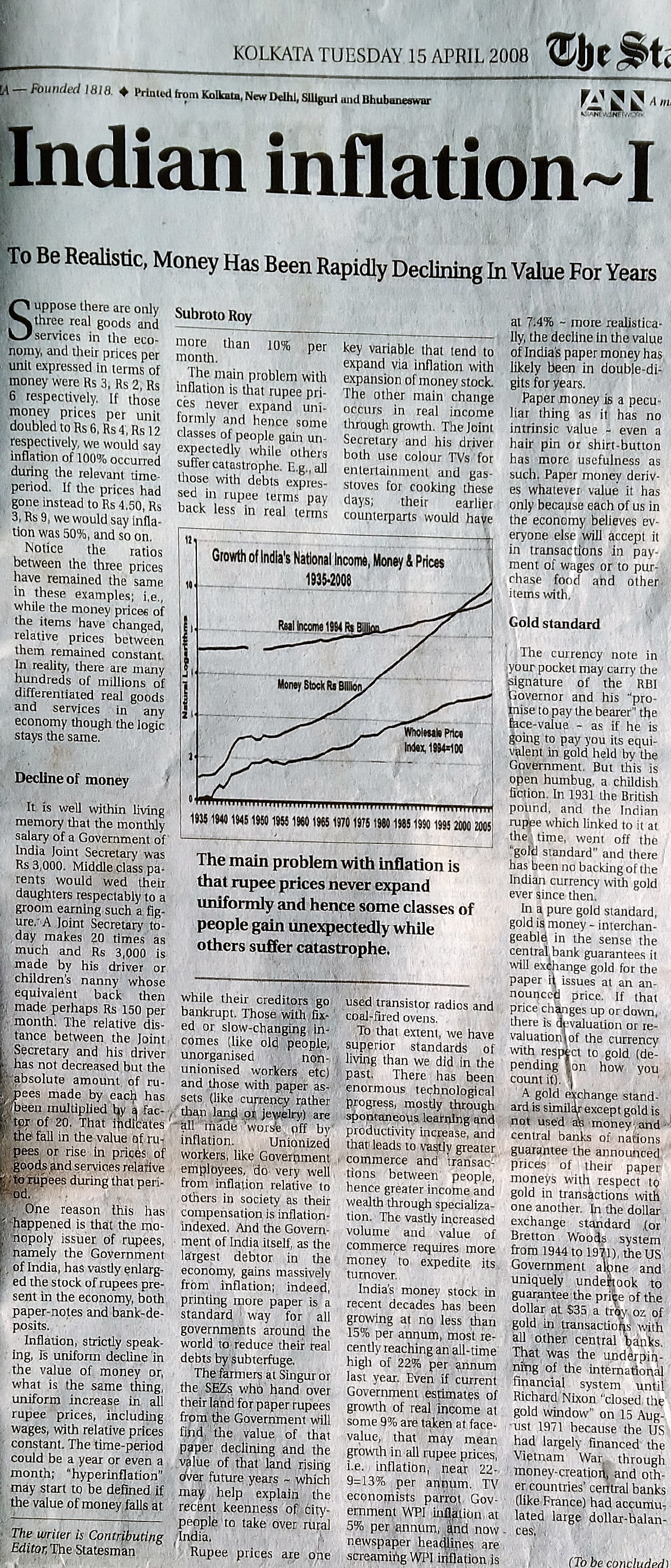

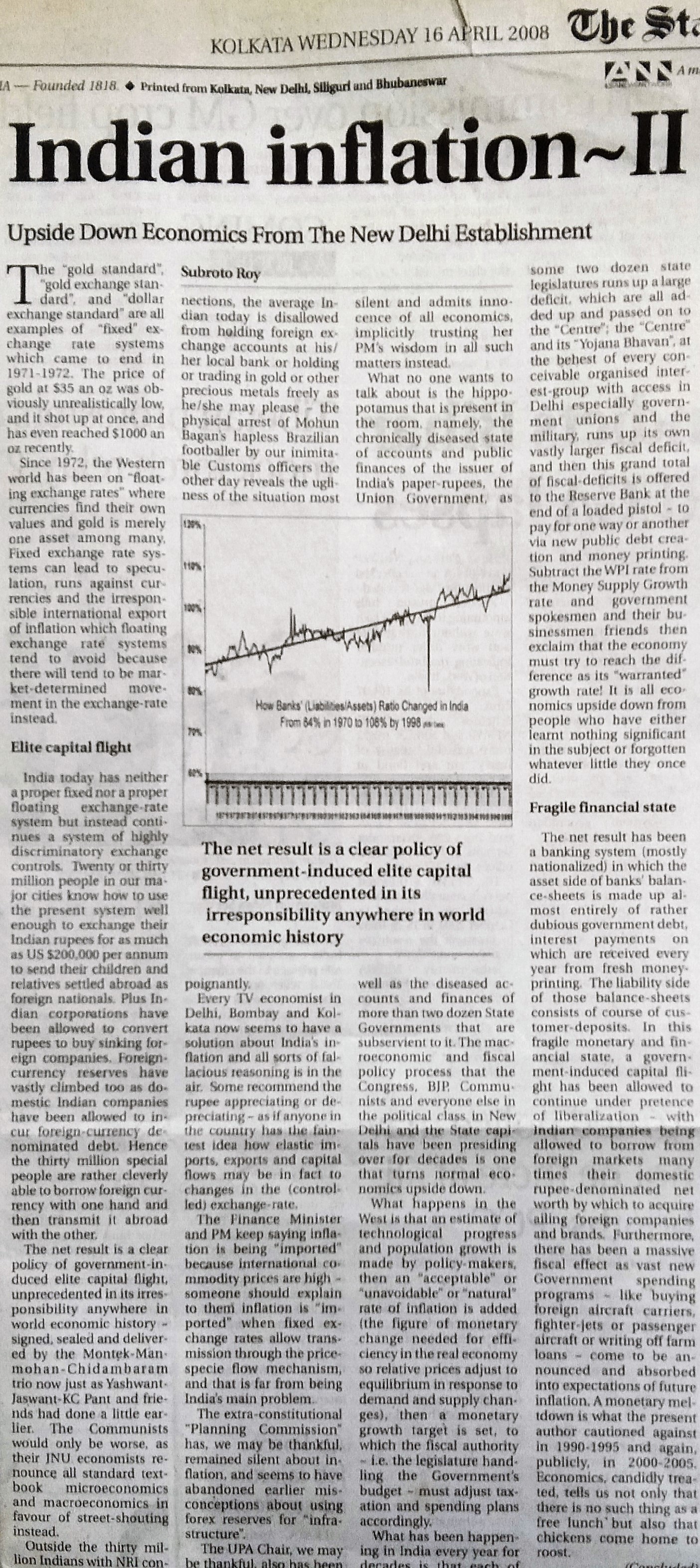

“Indian Inflation” (2008)

https://independentindian.com/2008/04/16/indian-inflation-upside-down-economics-from-new-delhis-establishment/

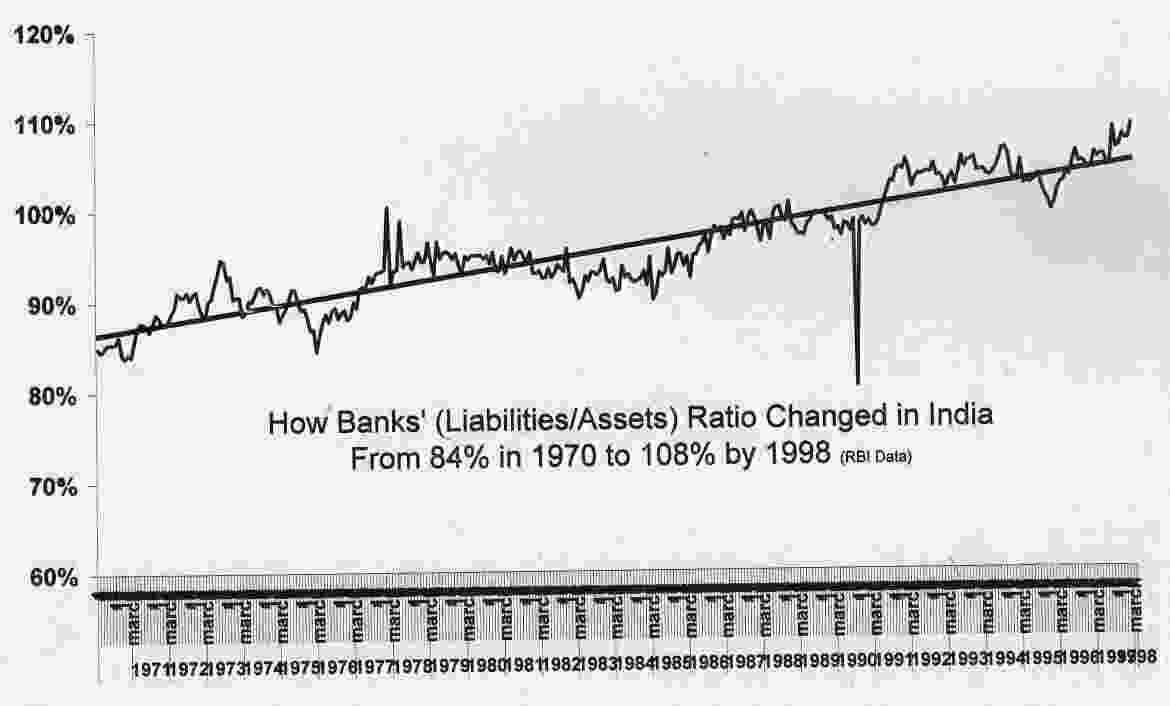

How the Liabilities/Assets Ratio of Indian Banks Changed from 84% in 1970 to 108% in 1998 https://independentindian.com/2008/10/20/how-the-liabilitiesassets-ratio-of-indian-banks-changed-from-84-in-1970-to-108-in-1998/

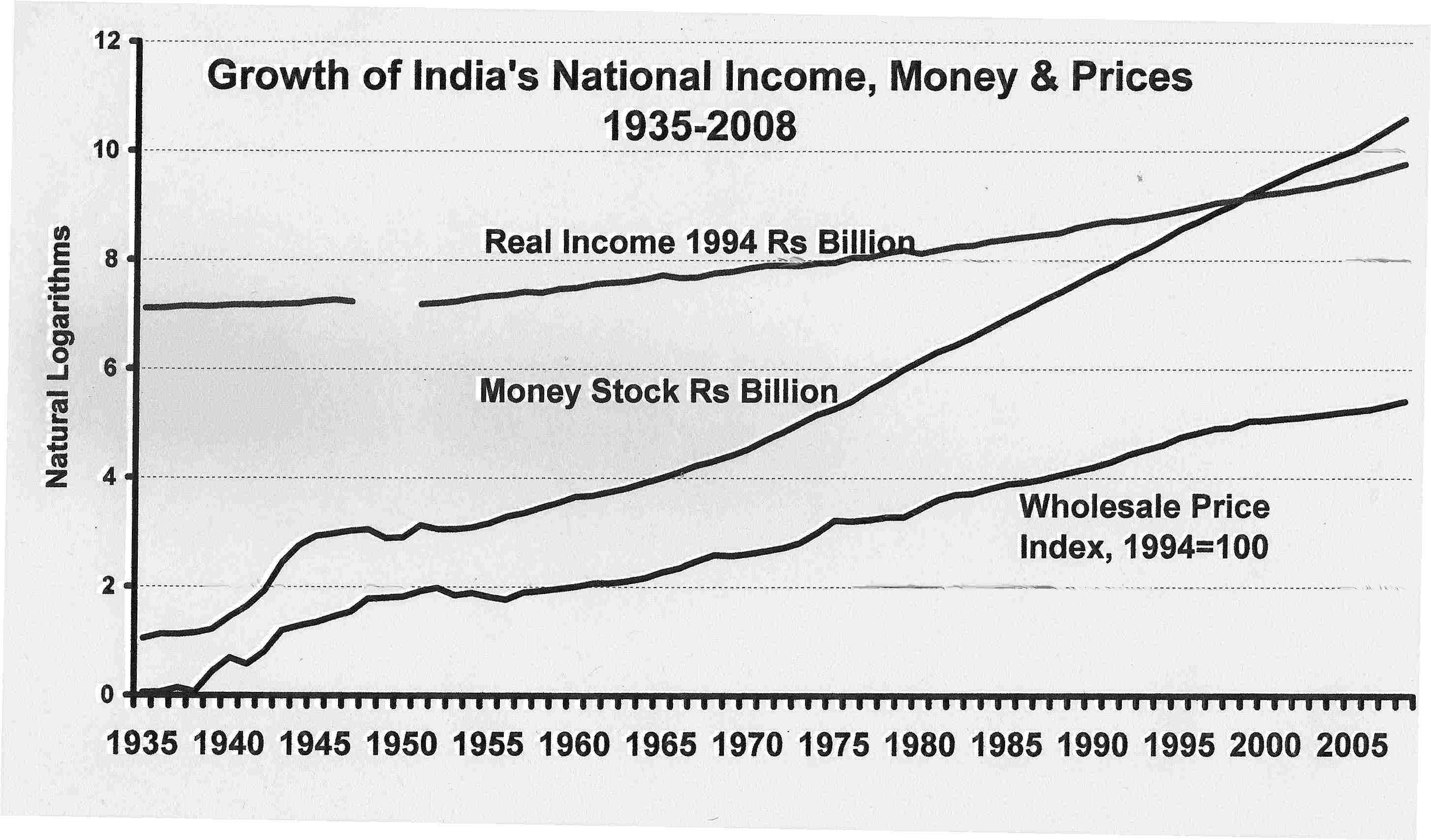

“Growth of Real Income, Money & Prices in India 1869-2004” (2005)

https://independentindian.com/2008/07/28/growth-of-real-income-money-prices-in-india-1869-2004/

“How to Budget” (2008)

https://independentindian.com/2008/02/26/how-to-budget-thrift-not-theft-should-guide-our-public-finances/

“Waffle but No Models of Monetary Policy: The RBI and Financial Repression (2005)”

https://independentindian.com/2005/10/27/waffle-but-no-models-of-monetary-policy-the-rbi-and-financial-repression/

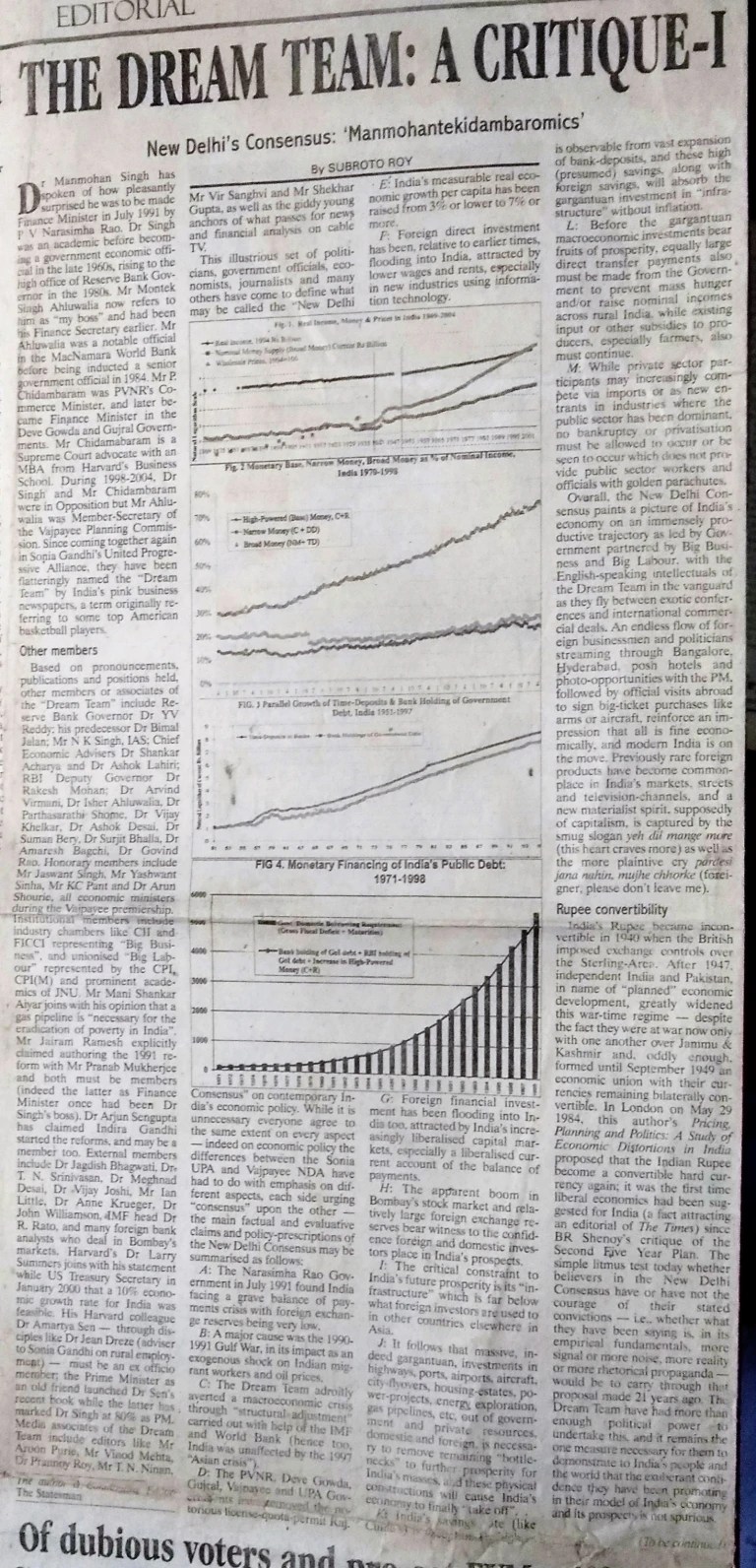

“The Dream Team: A Critique” (2006)

https://independentindian.com/2006/01/08/the-dream-team-a-critique/

“Against Quackery” (2007)

https://independentindian.com/2007/09/24/against-quackery/

“Mistaken Macroeconomics” (2009)

https://independentindian.com/2009/06/12/mistaken-macroeconomics-an-open-letter-to-prime-minister-dr-manmohan-singh/

Towards a Highly Transparent Fiscal & Monetary Framework for India’s Union & State Governments (RBI lecture 29 April 2000)

https://independentindian.com/2000/04/29/towards-a-highly-transparent-fiscal-monetary-framework-for-india%E2%80%99s-union-state-governments/

“The Indian Revolution (2008)”

https://independentindian.com/2008/12/08/the-indian-revolution/

Can India Become an Economic Superpower or Will There Be a Monetary Meltdown? (2005)

https://independentindian.com/2005/05/05/can-india-become-an-economic-superpower-or-will-there-be-a-monetary-meltdown-2005/

Memo to Kaushik Basu, 2010

Land, Liberty, & Value, 2006

https://independentindian.com/2006/12/31/land-liberty-value/

On Land-Grabbing, 2007

https://independentindian.com/2007/01/14/on-land-grabbing/

No Marxist MBAs? An amicus curiae brief for the Honourable High Court

https://independentindian.com/2007/08/29/no-marxist-mbasan-amicus-curae-brief-for-the-honourable-high-court/

Coverage in The *Asian Age*/*Deccan Herald* of 4 Dec 2012.

.