My “Critique of Monetary Ideas of Manmohan & Modi: the Roy Model explaining to Bimal Jalan, Nirmala Sitharaman, RBI etc what it is they are doing” of 2019 is here.

My 5 December 2012 interview by Mr Paranjoy Guha Thakurta, on Lok Sabha TV, the channel of India’s Lower House of Parliament, broadcast for the first time on 9 December 2012 on Lok Sabha TV, is here and here in two parts.

My interview by GDI Impuls banking quarterly of Zürich published on 6 Dec 2012 is here.

My interview by Ragini Bhuyan of Delhi’s Sunday Guardian published on 16 Dec 2012 is here.

Subroto Roy has really done what he can, just about, for his country, & has been rewarded by his country’s government and its “institution of national importance” with the most despicable evil. It is a toss-up between whether my personal experience of Indian corruption and vicious state-tyranny is worse than my personal experience of bribery and perjury in the federal court system in America.

AKe Your bitterness is understandable. Patriotism is rising above appropriate anger toward individuals and continuing to love and serve the nation, even if it is infected by wicked individuals.

Subroto Roy Yes it is indeed, you are right…

AKe The history of most great nations contains examples of individuals who, though later acknowledged as heroes, were treated shabbily by their respective homelands. It is sad that you are being treated badly, but surely it is just by one institution and its envious employees, rather than by the entire country? At least, I hope this is caused by a small number of wickedly envious people rather than by an established policy of the government.;

Subroto Roy Corruption is endemic in India… the matters I exposed some years ago had to do with (a) apparent siphoning off money in building (and purchase) contracts; and (b) apparently abusing the fiduciary interest of students by stealing from their fees to pay for round the world business-class travel, etc.. No, I am not bitter, either about India or about America but yes, as I have said it is a toss-up between whether my personal experience of Indian corruption and vicious state-tyranny is worse than my personal experience of bribery and perjury in the federal court system in America.

AlKu A is right, though, that you were affected by individual actions more, I think, than by the nation as a whole in both instances. I wish that your fine work was getting the lion’s share of attention and not causing you troubles at all. But ideas have their natural audiences and all too often that audience is located in the future — as Andrea noted. Keep the faith, Suby. Truth does win out in time. And that really does matter too. Listen to the ladies, Suby …

Subroto Roy Thanks though, that you were affected by individual actions”, Individualism is of course something I know much about since my Hayek days (Frank Hahn called me 26 years ago “probably the outstanding young Hayekian”) but my experience has been mixed.

I have had quite long associations with three academic institutions, two in America, one in India. At the first, my academic work was attacked by a gang of what I have called “inert game theorists”, game theory being the prevalent fashion at the time, there was an academic freedom issue and I let it be; but on top of that arose the open and blatant sexual harassment of a woman graduate student by the department head, and my helping her, in a very minimal but essential way, contributed to the conflict. I did not fight it more than a bit and left (for BYU, where the Mormons gave me refuge and allowed me to complete my book, almost).

The second case, also in America, was one of outrageous collective targeting of my work as an academic and an economist by my national origin, even my purported race and religion, and when I did battle that, having immense faith in the American system, my adversary responded by demonstrated perjury, buying out my attorney (and getting caught doing it), and compromising the federal judge. Not good. Certainly my faith in the American system was shaken but *not* in America herself — why? because two of the greatest 20th C American economists, Milton Friedman and TW Schultz — gladly stood for me, and their testimony (ignored by the compromised judge) was far more important than anything else to me. I.e., it was these two American *individuals* (as well as several others less eminent but equally heroic) who allowed my faith in America to continue unshaken even though the personal experience of the institutions had been ghastly.

The Indian case is wholly different as it is a wholly different political culture for the most part. The issues are cheap and pathetic — fraudulent academic credentials, stealing money from the government, stealing money from students, stealing others’ property wherever possible in the knowledge you can get away with it, etc.

I have been a rather harsh critic of Indian English-language media but I was pleased to see Mr Karan Thapar with good research systematically expose the other day the nonsense being purveyed by Mr Nandan Nilekani about the idea of branding each of a billion Indians with a government number. This is not Auschwitz. Nor can India create an American-style Social Security Administration. Mr Nilekani seems not to have the faintest idea about India’s poor and destitute, else he would not have made a statement like “We need one single, non-duplicate way of identifying a person and we need a mechanism by which we can authenticate that online anywhere because that can have huge benefits and impact on public services and also on making the poor more inclusive in what is happening in India today.” (italics added)

What does he plan to do? Haul away the hundreds of thousands of homeless from the streets and flyovers of our major cities and start interrogating, measuring, photographing and fingerprinting them against their will? On what ploy? That without the number he will give them they will not be able to continue to live and do what they have been doing for half a generation? Or that they will get a delicious hot meal from the Taj or Oberoi if they cooperate? And what about rural India? Does he plan to make an aerial survey of India’s rural landscapes by helicopter to find whom he can catch to interrogate and fingerprint? It will be grotesquely amusing to see his cohorts try to identify and then haul away India’s poor from their normal activities — he and his friends will likely come to grief trying to do so! Guaranteed. And the people will cheer because they know fakery when they see it.

Mr Nilekani needs to ask his economist-friends to teach him about asymmetric information, incentive-compatiblity theory etc. There have been several Bank of Sweden prizes given to economists for this material, beginning with FA Hayek in 1974 or even earlier.

(As for the wholly different stated agenda of preventing crime and terrorism using Mr Nilekani’s numbering, might we recall that Kasab’s dead companions have remained unclaimed in a Mumbai morgue for almost ten months now?)

The whole exercise that Prime Minister Manmohan Singh has with such fanfare set Mr Nilekani is ill-conceived and close to complete nonsense — designed only to keep in business the pampered industry that Mr Nilekani has been part of as well as its bureaucratic friends. The Prime Minister has made another error and should put a stop to it before it gets worse. The poor have their privacy and their dignity. They are going to refuse to waste their valuable time at the margins of survival volunteering for such gimmickry.

A Discussion Regarding Mr Nilekani’s Public Project

I don’t think registering everyone in the country is such a bad idea. It may be difficult. But the post office reaches letters to anyone in the country, even the homeless. I don’t think it is doing anything wrong.

I replied:

The post office reaches letters to those with an address.

Friendly Critic replied:

You are mistaken. It reaches letters to beggars, addressed to the nearest pan shop. To repeat, I do not think it is wrong to register all residents; there are some good uses for it. If it is all right to enumerate residents once every ten years, there is nothing wrong in maintaining a continuous inventory. Only the British have an aversion to doing so, on grounds of piracy. But even their electoral registers are based on enumeration. And to attack Nilekani simply because he has taken on a job offered seems excessive to me.

I replied:

Thanks for this correspondence. We may be slightly at cross-purposes and there may be some miscomprehension. Of course if a beggar has a pan-shop as an address, that is an address. But we are not talking about the efficiency or lack thereof of our postal services.

We are talking about the viability and utility of trying to attach a number, as an identification tag, to every Indian — for the declared purposes of (a) battling absolute poverty (of the worst kind); and(b) battling terrorism and crime.

Many Indians have passports, driving licenses, Voter cards, PAN numbers, mobile numbers etc. I am sure giving them a Nandan Nilekani Number will be easy. It will be, incidentally, lucrative for the IT industry.

It will also be pointless to the extent that these people, who may number into the hundreds of millions, are already adequately identifiable by one or two other forms of photo id-cards. (By way of analogy incidentally, Americans used to cash cheques at supermarkets using one or two photo ids — but the Social Security Card or number was not allowed to be one of them as it had no photo.)

Neither of the two declared objectives will have been explicitly served by giving Nandan Nilekani Numbers to those already adequately identifiable.

My point about incentive-compatibility is that the intended beneficiaries in any program of this kind (namely the anonymous absolute poor) need to have clear natural incentives to participate in order to make it work. Here there are none. Taking the very poorest people off the streets or out of their hamlets to be interrogated, photographed, fingerprinted and enumerated against their will, when they may have many more valuable things to be doing with their time in order to survive, is a violation of their freedom, privacy and dignity. Even if they submit to all this voluntarily, there are no obvious tangible benefits accruing to them as individuals as a result of this number (that many will not be able to read).

If those already adequately identifiable easily get an NNN (at low cost and without violation of indvidual freedom or dignity), while those who are the intended beneficiaries do not do so (except at high cost and with violations of individual freedom and dignity), that would enhance inequality.

Because such obvious points have failed to be accounted ab initio in this Big Business scheme paid for by public money, I have had to call it nonsensical.

Some follow-up 11 January 2013

From Facebook 11 January 2013

A biometrically generated large number is given to a very poor barely literate person and he/she is instructed that that is the key, the *sole* key, to riches and benefits from the state. The person lives on the margins of survival, eking out a daily income for himself/herself plus dependents under trying conditions. It is that absolute anonymous poor — who are *not* already identifiable easily through mobile numbers, voter id cards, drivers’ licenses etc — who are the intended beneficiaries. Suppose that person loses the card or has it stolen. Has the key to the riches and benefits from the state vanished? Those who are already easily identifiable need only produce alternative sources of identification and so for them to get the number as a means of identification is redundant, yet it is they who will likely have better access to the supposed benefits rather than the absolute poor. What New Delhi’s governing class fails to see is that the masses of India’s poor are not themselves a mass waiting for New Delhi’s handouts: they are *individuals*, free, rational, thinking individuals who know their own lives and resources and capacities and opportunities, and how to go about living their lives best. What they need is security, absence of state or other tyranny, roads, fresh water, electricity, functioning schools for their children, market opportunities for work, etc, not handouts from a monarch or aristocrats or businessmen….

“Manmohan and Sonia have violated Rajiv Gandhi’s intended reforms”.

I said inter alia

“WASTE, fraud and abuse are inevitable in the use and allocation of public property and resources in India as elsewhere, but Government is supposed to fight and resist such tendencies. The Sonia-Manmohan Government have done the opposite, aiding and abetting a wasteful anti-economics ~ i.e., an economic quackery. Vajpayee-Advani and other Governments, including Narasimha-Manmohan in 1991-1996, were just as complicit in the perverse policy-making. So have been State Governments of all regional parties like the CPI-M in West Bengal, DMK/ AIADMK in Tamil Nadu, Congress/NCP/ BJP/Sena in Maharashtra, TDP /Congress in Andhra Pradesh, SP/BJP/BSP in Uttar Pradesh etc. Our dismal politics merely has the pot calling the kettle black while national self-delusion and superstition reign in the absence of reason. The general pattern is one of well-informed, moneyed, mostly city-based special interest groups (especially including organised capital and organised labour) dominating government agendas at the cost of ill-informed, diffused anonymous individual citizens ~ peasants, small businessmen, non-unionized workers, old people, housewives, medical students etc….Rajiv Gandhi had a sense of noblesse oblige out of remembrance of his father and maternal grandfather. After his assassination, the comprador business press credited Narasimha Rao and Manmohan Singh with having originated the 1991 economic reform. In May 2002, however, the Congress Party itself passed a resolution proposed by Digvijay Singh explicitly stating Rajiv and not either of them was to be so credited. The resolution was intended to flatter Sonia Gandhi but there was truth in it too. Rajiv, a pilot who knew no political economy, was a quick learner with intelligence to know a good idea when he saw one and enough grace to acknowledge it. …Rajiv was entirely convinced when the suggestion was made to him in September 1990 that an enormous infusion of public resources was needed into the judicial system for promotion and improvement of the Rule of Law in the country, a pre-requisite almost for a new market orientation. Capitalism without the Rule of Law can quickly degenerate into an illiberal hell of cronyism and anarchy which is what has tended to happen since 1991. The resources put since Independence to the proper working of our judiciary from the Supreme Court and High Courts downwards have been abysmal, while the state of prisons, borstals, mental asylums and other institutions of involuntary detention is nothing short of pathetic. Only police forces, like the military, paramilitary and bureaucracies, have bloated in size….Neither Sonia-Manmohan nor the BJP or Communists have thought promotion of the Rule of Law in India to be worth much serious thought ~ certainly less important than attending bogus international conclaves and summits to sign expensive deals for arms, aircraft, reactors etc. Yet Rajiv Gandhi, at a 10 Janpath meeting on 23 March 1991 when he received the liberalisation proposals he had authorized, explicitly avowed the importance of greater resources towards the Judiciary. Dr Singh and his acolytes were not in that loop, indeed they precisely represented the bureaucratic ancien regime intended to be changed, and hence have seemed quite uncomprehending of the roots of the intended reforms ever since 1991.”

Days after the article appeared there were press reports Dr Singh was murmuring about quitting, and then came a fierce speech in Hindi from the Congress President saying “enemies” would receive their dues or whatever – only to be retracted a few days later saying that no more had been meant than a local critique of the BJP in Haryana politics! (Phew! I said to myself in relief…)

All this is constructive and positive, late as it is since Sonia Gandhi and Manmohan Singh both became heavy-duty Congress Party politicians for the first time a dozen years ago.

“….….The most serious examples of the malfunctioning of civil government in India are probably the failure to take feasible public precautions against the monsoons and the disarray of the judicial system. …The Statesman lamented in July 1980:`The simplest matter takes an inordinate amount of time, remedies seldom being available to those without means or influence. Of the more than 16,000 cases pending in the Supreme Court, about 5,000 were introduced more than five years ago; while nearly 16,000 of the backlog of more than 600,000 cases in our high courts have been hanging fire for over a decade. Allahabad is the worst offender but there are about 75,000 uncleared cases in the Calcutta High Court in addition to well over a million in West Bengal’s lower courts.” Such a state of affairs has been caused not only by lazy and corrupt policemen, court clerks and lawyers, but also by the paucity of judges and magistrates. . . . a vast volume of laws provokes endless litigation as much because of poor drafting which leads to disputes over interpretation as because they appear to violate particular rights and privileges…. When governments determinedly do what they need not or should not do, it may be expected that they will fail to do what civil government positively should be doing.”A few months ago was the 25th anniversary of this statement… ! 🙂

“Similarly, Rajiv comprehended when it was said to him that the primary fiscal problem faced by India is the vast and uncontrolled public debt, interest payments on which suck dry all public budgets leaving no room for provision of public goods. Government accounts: Government has been routinely “rolling over” its domestic debt in the asset-portfolios of the nationalised banks while displaying and highlighting only its new additional borrowing in a year as the “Fiscal Deficit”. More than two dozen States have been doing the same and their liabilities ultimately accrue to the Union too. The stock of public debt in India is Rs 30 trillion (Rs 30 lakh crore) at least, and portends a hyperinflation in the future. There has been no serious recognition of this since it is political and bureaucratic actions that have been causing the problem. Proper recognition would entail systematically cleaning up the budgets and accounts of every single governmental entity in the country: the Union, every State, every district and municipality, every publicly funded entity or organisation, and at the same time improving public decision-making capacity so that once budgets and accounts recover from grave sickness over decades, functioning institutions exist for their proper future management. All this would also stop corruption in its tracks, and release resources for valuable public goods and services like the Judiciary, School Education and Basic Health. Institutions for improved political and administrative decision-making are needed throughout the country if public preferences with respect to raising and allocating common resources are to be elicited and then translated into actual delivery of public goods and services. Our dysfunctional legislatures will have to do at least a little of what they are supposed to. When public budgets and accounts are healthy and we have functioning public goods and services, macroeconomic conditions would have been created for the paper-rupee to once more become a money as good as gold ~ a convertible world currency for all of India’s people, not merely the metropolitan special interest groups that have been controlling our governments and their agendas.”

I may add my father, back in 1973 in Paris, had predicted to me that you would become Prime Minister of India one day, and he, now in his 90s, is joined by myself in sending our warm congratulations at the start of your second term in that high office.

The controversy though that you and I had entered that Paris day in 1973 about scientific economics as applied to India, must be renewed afresh!

This is because of your categorical statement on June 9 2009 to the new 15th Lok Sabha:

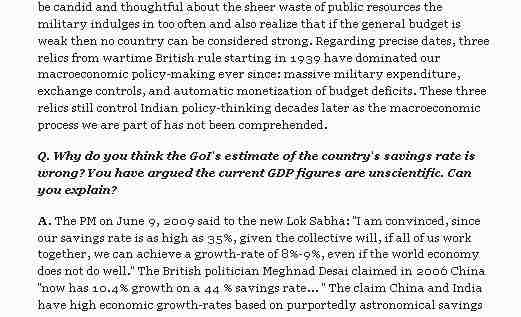

“I am convinced, since our savings rate is as high as 35%, given the collective will, if all of us work together, we can achieve a growth-rate of 8%-9%, even if the world economy does not do well.” (Statement of Dr Manmohan Singh to the Lok Sabha, June 9 2009)

I am afraid there may be multiple reasons why such a statement is gravely and incorrigibly in error within scientific economics. From your high office as Prime Minister in a second term, faced perhaps with no significant opposition from either within or without your party, it is possible the effects of such an error may spell macroeconomic catastrophe for India.

Indeed the idea that China and India have had extremely high economic growth-rates based on purportedly astronomical savings rates has become a commonplace in recent years, repeated endlessly in international and domestic policy circles though perhaps without adequate basis.

1. Germany & Japan

What, at the outset, is supposed to be measured when we speak of “growth”? Indian businessmen and their media friends seem to think “growth” refers to something like nominal earnings before tax for the organised corporate sector, or any unspecified number that can be sold to visiting foreigners to induce them to park their funds in India: “You will get a 10% return if you invest in India” to which the visitor says “Oh that must mean India has 10% growth going on”. Of such nonsense are expensive international conferences in Davos and Delhi often made.

You will doubtless agree the economist at least must define economic growth properly and with care — what is referred to must be annual growth of per capita inflation-adjusted Gross Domestic Product. (Per capita National Income or Net National Product would be even better if available).

West Germany and Japan had the highest annual per capita real GDP growth-rates in the world economy starting from devastated post-World War II initial conditions. What were their measured rates?

West Germany: 6.6% in 1950-1960, falling to 3.5% by 1960-1970 falling to 2.4% by 1970-1978.

Japan: 6.8 % in 1952-1960 rising to 9.4% in 1960-1970 falling to 3.8 % in 1970-1978.

Thus in recent decadesonly Japan measured a spike in the 1960s of more than 9% annual growth of real per capita GDP. Now India and China are said to be achieving 8%-10 % and more year after year routinely!

Perhaps we are observing an incredible phenomenon of world economic history. Or perhaps it is just something incredible, something false and misleading, like a mirage in the desert.

You may agree that processes of measurement of real income in India both at federal and provincial levels, still remain well short of the world standards described by the UN’s System of National Accounts 1993. The actuality of our real GDP growth may be better than what is being measured or it may be worse than what is being measured – from the point of view of public decision-making we at present simply do not know which it is, and to overly rely on such numbers in national decisions may be unwise. In any event, India’s population is growing at near 2% so even if your Government’s measured number of 8% or 9% is taken at face-value, we have to subtract 2% population growth to get per capita figures.

2. Growth of the aam admi’s consumption-basket

The late Professor Milton Friedman had been an invited adviser in 1955 to the Government of India during the Second Five Year Plan’s formulation. The Government of India suppressed what he had to say and I had to publish it 34 years later in May 1989 during the 1986-1992 perestroika-for-India project that I led at the University of Hawaii in the United States. His November 1955 Memorandum to the Government of India is a chapter in the book Foundations of India’s Political Economy: Towards an Agenda for the 1990s that I and WE James created.

“I don’t believe the term GNP ought to be used unless it is supplemented by a different statistic: the rate of growth of the average consumption basket consumed by the ordinary individual in the country. I think GNP rates of growth can give very misleading information. For example, you have rapid rates of growth of GNP in the Soviet Union with a declining standard of life for the people. Because GNP includes monuments and includes also other things. I’m not saying that that is the case with India; I’m just saying I would like to see the two figures together.”

You may perhaps agree upon reflection that not only may our national income growth measurements be less robust than we want, it may be better to be measuring something else instead, or as well, as a measure of the economic welfare of India’s people, namely, “the rate of growth of the average consumption basket consumed by the ordinary individual in the country”, i.e., the rate of growth of the average consumption basket consumed by the aam admi.

It would be excellent indeed if you were to instruct your Government’s economists and other spokesmen to do so this as it may be something more reliable as an indicator of our economic realities than all the waffle generated by crude aggregate growth-rates.

3. Logic of your model

Thirdly, the logic needs to be spelled out of the economic model that underlies such statements as yours or Meghnad Desai’s that seek to operationally relate savings rates to aggregate growth rates in India or China. This seems not to have been done publicly in living memory by the Planning Commission or other Government economists. I have had to refer, therefore, to pages 251-253 of my own Cambridge doctoral thesis under Professor Frank Hahn thirty years ago, titled “On liberty and economic growth: preface to a philosophy for India”, where the logic of such models as yours was spelled out briefly as follows:

Let

Kt be capital stock

Yt be national output

It be the level of real investment

St be the level of real savings

By definition

It = K t+1 – Kt

By assumption

Kt = k Yt 0 < k < 1

St = sYt 0 < s <1

In equilibrium ex ante investment equals ex ante savings

It = St

Hence in equilibrium

sYt = K t+1 – Kt

Or

s/k = g

where g is defined to be the rate of growth (Y t+1-Yt)/Yt .

The left hand side then defines the “warranted rate of growth” which must maintain the famous “knife-edge” with the right hand side “natural rate of growth”.

Your June 9 2009 Lok Sabha statement that a 35% rate of savings in India may lead to an 8%-9% rate of economic growth in India, or Meghnad Desai’s statement that a 44% rate of savings in China led to a 10.4% growth there, can only be made meaningful in the context of a logical economic model like the one I have given above.

[In the open-economy version of the model, let Mt be imports, Et be exports, Ft net capital inflows.

Assume

Mt = aIt + bYt 0 < a, b < 1

Et = E for all t

Balance of payments is

Bt = Mt – Et – Ft

In equilibrium It = St + Bt

Or

Ft = (s+b) Yt – (1-a) It – E is a kind of “warranted” level of net capital inflow.]

You may perhaps agree upon reflection that building the entire macroeconomic policy of the Government of India merely upon a piece of economic logic as simplistic as the

s/k = g

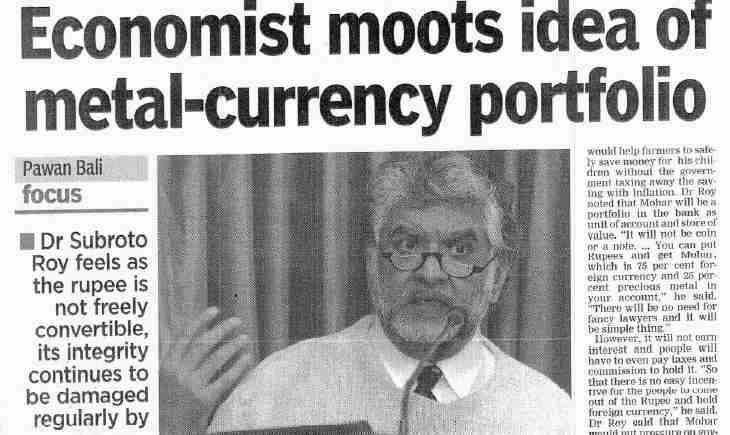

equation above, may spell an unacceptable risk to the future economic well-being of our vast population. An alternative procedural direction for macroeconomic policy, with more obviously positive and profound consequences, may have been that which I sought to persuade Rajiv Gandhi about with some success in 1990-1991. Namely, to systematically seek to improve towards normalcy the budgets, financial positions and decision-making capacities of the Union and all state and local governments as well as all public institutions, organisations, entities, and projects in general, with the aim of making our domestic money a genuine hard currency of the world again after seven decades, so that any ordinary resident of India may hold and trade precious metals and foreign exchange at his/her local bank just like all those glamorous privileged NRIs have been permitted to do. Such an alternative path has been described in “The Indian Revolution”, “Against Quackery”, “The Dream Team: A Critique”,“India’s Macroeconomics”, “Indian Inflation”, etc.

4. Gross exaggeration of real savings rate by misreading deposit multiplication

Specifically, I am afraid you may have been misled into thinking India’s real savings rate, s, is as high as 35% just as Meghnad Desai may have misled himself into thinking China’s real savings rate is as high as 44%.

Neither of you may have wanted to make such a claim if you had referred to the fact that over the last 25 years, the average savings rate across all OECD countries has been less than 10%. Economic theory always finds claims of discontinuous behaviour to be questionable. If the average OECD citizen has been trying to save 10% of disposable income at best, it appears prima facie odd that India’s PM claims a savings rate as high as 35% for India or a British politician has claimed a savings rate as high as 44% for China. Something may be wrong in the measurement of the allegedly astronomical savings rates of India and China. The late Professor Nicholas Kaldor himself, after all, suggested it was rich people who saved and poor people who did not for the simple reason the former had something left over to save which the latter did not!

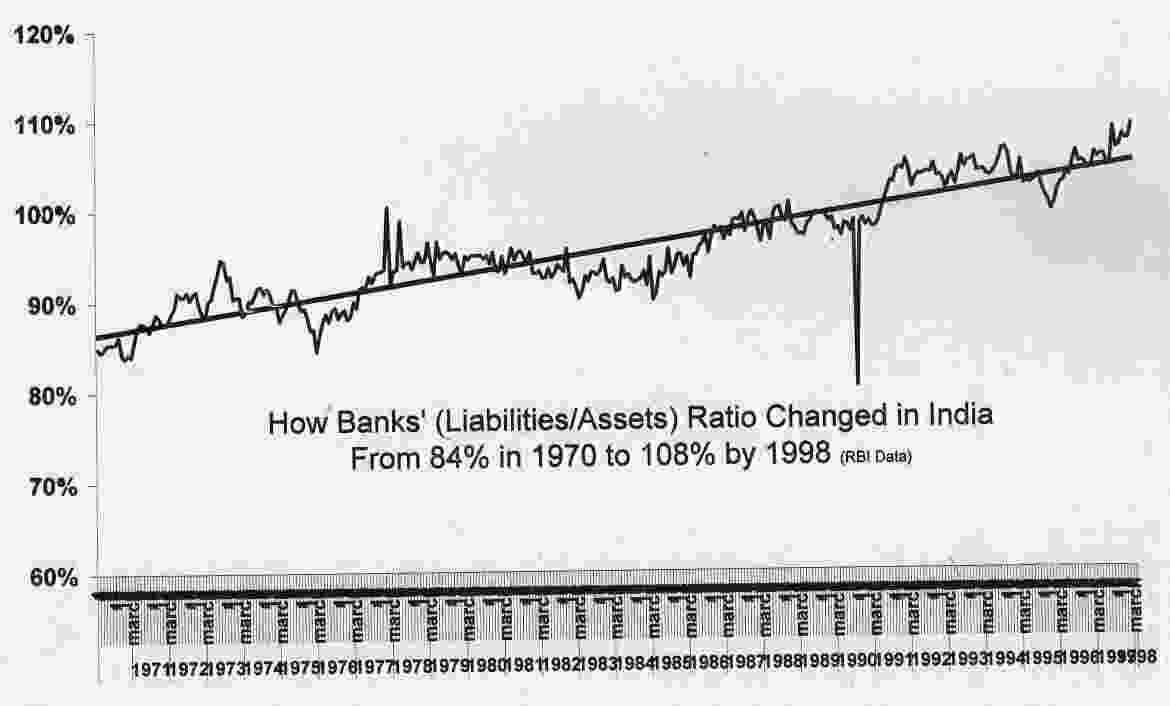

And indeed something is wrong in the measurements. What has happened, I believe, is that there has been a misreading of the vast nominal expansion of bank deposits via deposit-multiplication in the Indian banking system, an expansion that has been caused by explosive deficit finance over the last four or five decades. That vast nominal expansion of bank-deposits has been misread as indicating growth of real savings behaviour instead. I have written and spoken about and shown this quite extensively in the last half dozen years since I first discovered it in the case of India. E.g., in a lecture titled “Can India become an economic superpower or will there be a monetary meltdown?” at Cardiff University’s Institute of Applied Macroeconomics and at London’s Institute of Economic Affairs in April 2005, as well as in May 2005 at a monetary economics seminar invited at the RBI by Dr Narendra Jadav. The same may be true of China though I have looked at it much less.

“Savings is indeed normally measured by adding financial and non-financial savings. Financial savings include bank-deposits. But India is not a normal country in this. Nor is China. Both have seen massive exponential growth of bank-deposits in the last few decades. Does this mean Indians and Chinese are saving phenomenally high fractions of their incomes by assiduously putting money away into their shaky nationalized banks? Sadly, it does not. What has happened is government deficit-financing has grown explosively in both countries over decades. In a “fractional reserve” banking system (i.e. a system where your bank does not keep the money you deposited there but lends out almost all of it immediately), government expenditure causes bank-lending, and bank-lending causes bank-deposits to expand. Yes there has been massive expansion of bank-deposits in India but it is a nominal paper phenomenon and does not signify superhuman savings behaviour. Indians keep their assets mostly in metals, land, property, cattle, etc., and as cash, not as bank deposits.”

“India has followed in peacetime over six decades what the US and Britain followed during war. Our vast growth of bank deposits in recent decades has been mostly a paper (or nominal) phenomenon caused by unlimited deficit finance in a fractional reserve banking system. Policy makers have widely misinterpreted it as indicating a real phenomenon of incredibly high savings behaviour. In an inflationary environment, people save their wealth less as paper deposits than as real assets like land, cattle, buildings, machinery, food stocks, jewellery etc.”

If you asked me “What then is India’s real savings rate?” I have little answer to give except to say I know what it is not – it is not what the Government of India says it is. It is certainly unlikely to be anywhere near the 35% you stated it to be in your June 9 2009 Lok Sabha statement. If the OECD’s real savings rate has been something like 10% out of disposable income, I might accept India’s is, say, 15% at a maximum when properly measured – far from the 35% being claimed. What I believe may have been mismeasured by you and Meghnad Desai and many others as indicating high real savings is actually the nominal or paper expansion of bank-deposits in a fractional reserve banking system induced by runaway government deficit-spending in both India and China over the last several decades.

5. Technological progress and the mainsprings of real economic growth

So much for the g and s variables in the s/k = g equation in your economic model. But the assumed constant k is a big problem too!

During the 1989 perestroika-for-India project-conference, Professor Friedman referred to his 1955 experience in India and said this about the assumption of a constant k:

“I think there was an enormously important point… That was the almost universal acceptance at that time of the view that there was a sort of technologically fixed capital output ratio. That if you wanted to develop, you just had to figure out how much capital you needed, used as a statistical technological capital output ratio, and by God the next day you could immediately tell what output you were going to achieve. That was a large part of the motivation behind some of the measures that were taken then.”

The crucial problem of the sort of growth-model from which your formulation relating savings to growth arises is that, with a constant k, you have necessarily neglected the real source of economic growth, which is technological progress!

I said in the 2007 article referred to above:

“Economic growth in India as elsewhere arises not because of what politicians and bureaucrats do in capital cities, but because of spontaneous technological progress, improved productivity and learning-by-doing on part of the general population. Technological progress is a very general notion, and applies to any and every production activity or commercial transaction that now can be accomplished more easily or using fewer inputs than before.”

“The mainsprings of real growth in the wealth of the individual, and so of the nation, are greater practical learning, increases in capital resources and improvements in technology. Deeper skills and improved dexterity cause output produced with fewer inputs than before, i.e. greater productivity. Adam Smith said there is “invention of a great number of machines which facilitate and abridge labour, and enable one man to do the work of many”. Consider a real life example. A fresh engineering graduate knows dynamometers are needed in testing and performance-certification of diesel engines. He strips open a meter, finds out how it works, asks engine manufacturers what design improvements they want to see, whether they will buy from him if he can make the improvement. He finds out prices and properties of machine tools needed and wages paid currently to skilled labour, calculates expected revenues and costs, and finally tries to persuade a bank of his production plans, promising to repay loans from his returns. Overcoming restrictions of religion or caste, the secular agent is spurred by expectation of future gains to approach various others with offers of contract, and so organize their efforts into one. If all his offers ~ to creditors, labour, suppliers ~ are accepted he is, for the moment, in business. He may not be for long ~ but if he succeeds his actions will have caused an improvement in design of dynamometers and a reduction in the cost of diesel engines, as well as an increase in the economy’s produced means of production (its capital stock) and in the value of contracts made. His creditors are more confident of his ability to repay, his buyers of his product quality, he himself knows more of his workers’ skills, etc. If these people enter a second and then a third and fourth set of contracts, the increase in mutual trust in coming to agreement will quickly decline in relation to the increased output of capital goods. The first source of increasing returns to scale in production, and hence the mainspring of real economic growth, arises from the successful completion of exchange. Transforming inputs into outputs necessarily takes time, and it is for that time the innovator or entrepreneur or “capitalist” or “adventurer” must persuade his creditors to trust him, whether bankers who have lent him capital or workers who have lent him labour. The essence of the enterprise (or “firm”) he tries to get underway consists of no more than the set of contracts he has entered into with the various others, his position being unique because he is the only one to know who all the others happen to be at the same time. In terms introduced by Professor Frank Hahn, the entrepreneur transforms himself from being “anonymous” to being “named” in the eyes of others, while also finding out qualities attaching to the names of those encountered in commerce. Profits earned are partly a measure of the entrepreneur’s success in this simultaneous process of discovery and advertisement. Another potential entrepreneur, fresh from engineering college, may soon pursue the pioneer’s success and start displacing his product in the market ~ eventually chasers become pioneers and then get chased themselves, and a process of dynamic competition would be underway. As it unfolds, anonymous and obscure graduates from engineering colleges become by dint of their efforts and a little luck, named and reputable firms and perhaps founders of industrial families. Multiply this simple story many times, with a few million different entrepreneurs and hundreds of thousands of different goods and services, and we shall be witnessing India’s actual Industrial Revolution, not the fake promise of it from self-seeking politicians and bureaucrats.”

Technological progress in a myriad of ways and discovery of new resources are important factors contributing to India’s growth today. But while India’s “real” economy does well, the “nominal” paper-money economy controlled by Government does not. Continuous deficit financing for half a century has led to exponential growth of public debt and broad money, and, as noted, the vast growth of nominal bank-deposits has been misinterpreted as indicating unusually high real savings behaviour when it in fact may just signal vast amounts of government debt being held by our nationalised banks. These bank assets may be liquid domestically but are illiquid internationally since our government debt is not held by domestic households as voluntary savings nor has it been a liquid asset held worldwide in foreign portfolios.

What politicians of all parties, especially your own and the BJP and CPI-M since they are the three largest, have been presiding over is exponential growth of our paper money supply, which has even reached 22% per annum. Parliament and the Government should be taking honest responsibility for this because it may certainly portend double-digit inflation (i.e., decline in the value of paper-money) perhaps as high as 14%-15% per annum, something that is certain to affect the aam admi’s economic welfare adversely.

6. Selling Government assets to Big Business is a bad idea in a potentially hyperinflationary economy

Respected PradhanMantriji, the record would show that I, and really I alone, 25 years ago, may have been the first among Indian economists to advocate the privatisation of the public sector. (Viz, “Silver Jubilee of Pricing, Planning and Politics: A Study of Economic Distortions in India”.) In spite of this, I have to say clearly now that in present circumstances of a potentially hyperinflationary economy created by your Government and its predecessors, I believe your Government’s present plans to sell Government assets may be an exceptionally unwise and imprudent idea. The reasoning is very simple from within monetary economics.

Government every year has produced paper rupees and bank deposits in practically unlimited amounts to pay for its practically unlimited deficit financing, and it has behaved thus over decades. Such has been the nature of the macroeconomic process that all Indian political parties have been part of, whether they are aware of it or not.

Indian Big Business has an acute sense of this long-term nominal/paper expansion of India’s economy, and acts towards converting wherever possible its own hoards of paper rupees and rupee-denominated assets into more valuable portfolios for itself of real or durable assets, most conspicuously including hard-currency denominated assets, farm-land and urban real-estate, and, now, the physical assets of the Indian public sector. Such a path of trying to transform local domestic paper assets – produced unlimitedly by Government monetary and fiscal policy and naturally destined to depreciate — into real durable assets, is a privately rational course of action to follow in an inflationary economy. It is not rocket-science to realise the long-term path of rupee-denominated assets is downwards in comparison to the hard-currencies of the world – just compare our money supply growth and inflation rates with those of the rest of the world.

The Statesman of November 16 2006 had a lead editorial titled Government’s land-fraud: Cheating peasants in a hyperinflation-prone economy which said:

“There is something fundamentally dishonourable about the way the Centre, the state of West Bengal and other state governments are treating the issue of expropriating peasants, farm-workers, petty shop-keepers etc of their small plots of land in the interests of promoters, industrialists and other businessmen. Singur may be but one example of a phenomenon being seen all over the country: Hyderabad, Karnataka, Kerala, Haryana, everywhere. So-called “Special Economic Zones” will merely exacerbate the problem many times over. India and its governments do not belong only to business and industrial lobbies, and what is good for private industrialists may or may not be good for India’s people as a whole. Economic development does not necessarily come to be defined by a few factories or high-rise housing complexes being built here or there on land that has been taken over by the Government, paying paper-money compensation to existing stakeholders, and then resold to promoters or industrialists backed by powerful political interest-groups on a promise that a few thousand new jobs will be created. One fundamental problem has to do with inadequate systems of land-description and definition, implementation and recording of property rights. An equally fundamental problem has to do with fair valuation of land owned by peasants etc. in terms of an inconvertible paper-money. Every serious economist knows that “land” is defined as that specific factor of production and real asset whose supply is fixed and does not increase in response to its price. Every serious economist also knows that paper-money is that nominal asset whose price can be made to catastrophically decline by a massive increase in its supply, i.e. by Government printing more of the paper it holds a monopoly to print. For Government to compensate people with paper-money it prints itself by valuing their land on the basis of an average of the price of the last few years, is for Government to cheat them of the fair present-value of the land. That present-value of land must be calculated in the way the present-value of any asset comes to be calculated, namely, by summing the likely discounted cash-flows of future values. And those future values should account for the likelihood of a massive future inflation causing decline in the value of paper-money in view of the fact we in India have a domestic public debt of some Rs. 30 trillion (Rs. 30 lakh crore) and counting, and money supply growth rates averaging 16-17% per annum. In fact, a responsible Government would, given the inconvertible nature of the rupee, have used foreign exchange or gold as the unit of account in calculating future-values of the land. India’s peasants are probably being cheated by their Government of real assets whose value is expected to rise, receiving nominal paper assets in compensation whose value is expected to fall.”

Shortly afterwards the Hon’ble MP for Kolkata Dakshin, Km Mamata Banerjee, started her protest fast, riveting the nation’s attention in the winter of 2006-2007. What goes for government buying land on behalf of its businessman friends also goes, mutatis mutandis, for the public sector’s real assets being bought up by the private sector using domestic paper money in a potentially hyperinflationary economy. If your new Government wishes to see real assets of the public sector being sold for paper money, let it seek to value these assets not in inconvertible rupees that Government itself has been producing in unlimited quantities but perhaps in forex or gold-units instead!

In the 2004-2005 volume Margaret Thatcher’s Revolution: How it Happened and What it Meant, edited by myself and Professor John Clarke, there is a chapter by Professor Patrick Minford on Margaret Thatcher’s fiscal and monetary policy (macroeconomics) that was placed ahead of the chapter by Professor Martin Ricketts on Margaret Thatcher’s privatisation (microeconomics). India’s fiscal and monetary or macroeconomic problems are far worse today than Britain’s were when Margaret Thatcher came to power. We need to get our macroeconomic problems sorted before we attempt the microeconomic privatisation of public assets.

It is wonderful that your young party colleague, the Hon’ble MP from Amethi, Shri Rahul Gandhi, has declined to join the present Government and instead wishes to reflect further on the “common man” and “common woman” about whom I had described his late father talking to me on September 18 1990. Certainly the aam admi is not someone to be found among India’s lobbyists of organised Big Business or organised Big Labour who have tended to control government agendas from the big cities.

With my warmest personal regards and respect, I remain,

The power of organised Big Business over New Delhi’s economic policies (whether Congress-led or BJP-led) was signalled by the presence in the audience at Rashtrapati Bhavan last week of several prominent lobbyists when Dr Manmohan Singh and his senior-most Cabinet colleagues were being sworn-in by the President of India. Why were such witnesses needed at such an auspicious national occasion?

Organised Big Business (both private sector and public sector) along with organised Big Labour (whose interests are represented most ably by New Delhi’s official communist parties like the CPI-M and CPI), are astutely aware of how best to advance their own economic interests; this usually gets assisted nicely enough through clever use of our comprador English-language TV, newspaper and magazine media. Shortly after the election results, lobbyists were all over commercial TV proposing things like FDI in insurance and airports etc– as if that was the meaning of the Sonia-Rahul mandate or were issues of high national priority. A typical piece of such “pretend-economics” appears in today’s business-press from a formerly Leftist Indian bureaucrat: “With its decisive victory, the new Manmohan Singh government should at last be able to implement the required second generation reforms. Their lineaments (sic) are well known and with the removal of the Left’s veto, many of those stalled in the legislature as well as those which were forestalled can now be implemented. These should be able to put India back on a 9-10 per cent per annum growth rate…”

Today’s business-press also reports that the new Government is planning to create a fresh “Disinvestment Ministry” and Dr Singh’s chief economic policy aide is “a frontrunner among the names short-listed to head the new ministry” with Cabinet rank.

That being said, I have to say I think a new Indian policy of creating a Ministry to privatise India’s public sector is probably a very BAD idea indeed in present circumstances — mainly because it will be driven by the interests of the organised Big Business lobbies that have so profoundly and subtly been able to control the New Delhi Government’s behaviour in recent decades.

Now our Government every year produces paper rupees and bank deposits in practically unlimited amounts to pay for its practically unlimited deficit financing, and it has behaved thus over decades. Why we do not hear about this at all is because the most prominent Government economists themselves remain clueless — sometimes by choice, mostly by sheer ignorance — about the nature of the macroeconomic process that they are or have been part of. (See my “India’s Macroeconomics”, “The Dream Team: A Critique” etc elsewhere here). As for the Opposition’s economists, the less said about the CPI-M’s economists the better while the BJP, poor thing, has absolutely no economists at all!

Briefly speaking, Indian Big Business has acquired an acute sense of this long-term nominal/paper expansion of India’s economy, and as a result acts towards converting wherever possible its own hoards of paper rupees and rupee-denominated assets into more valuable portfolios for itself of real or durable assets, most conspicuously including hard-currency denominated assets, farm-land and urban real-estate, and, now, the physical assets of the Indian public sector. Such a path of trying to transform local domestic paper assets – produced unlimitedly by Government monetary and fiscal policy and naturally destined to depreciate — into real durable assets, is a privately rational course of action to follow in an inflationary economy. It is not rocket-science to realise the long-term path of the Indian rupee is downwards in comparison to the hard-currencies of the world – just compare our money supply growth and inflation rates with those of the rest of the world.

The Statesman of November 15 2006 had a lead editorial titled Government’s land-fraud: Cheating peasants in a hyperinflation-prone economy. It said:

“There is something fundamentally dishonourable about the way the Centre, the state of West Bengal and other state governments are treating the issue of expropriating peasants, farm-workers, petty shop-keepers etc of their small plots of land in the interests of promoters, industrialists and other businessmen. Singur may be but one example of a phenomenon being seen all over the country: Hyderabad, Karnataka, Kerala, Haryana, everywhere. So-called “Special Economic Zones” will merely exacerbate the problem many times over. India and its governments do not belong only to business and industrial lobbies, and what is good for private industrialists may or may not be good for India’s people as a whole. Economic development does not necessarily come to be defined by a few factories or high-rise housing complexes being built here or there on land that has been taken over by the Government, paying paper-money compensation to existing stakeholders, and then resold to promoters or industrialists backed by powerful political interest-groups on a promise that a few thousand new jobs will be created. One fundamental problem has to do with inadequate systems of land-description and definition, implementation and recording of property rights. An equally fundamental problem has to do with fair valuation of land owned by peasants etc. in terms of an inconvertible paper-money. Every serious economist knows that “land” is defined as that specific factor of production and real asset whose supply is fixed and does not increase in response to its price. Every serious economist also knows that paper-money is that nominal asset whose price can be made to catastrophically decline by a massive increase in its supply, i.e. by Government printing more of the paper it holds a monopoly to print. For Government to compensate people with paper-money it prints itself by valuing their land on the basis of an average of the price of the last few years, is for Government to cheat them of the fair present-value of the land. That present-value of land must be calculated in the way the present-value of any asset comes to be calculated, namely, by summing the likely discounted cash-flows of future values. And those future values should account for the likelihood of a massive future inflation causing decline in the value of paper-money in view of the fact we in India have a domestic public debt of some Rs. 30 trillion (Rs. 30 lakh crore) and counting, and money supply growth rates averaging 16-17% per annum. In fact, a responsible Government would, given the inconvertible nature of the rupee, have used foreign exchange or gold as the unit of account in calculating future-values of the land. India’s peasants are probably being cheated by their Government of real assets whose value is expected to rise, receiving nominal paper assets in compensation whose value is expected to fall.”

Mamata Banerjee started her famous protest fast-unto-death in Kolkata not long afterwards, riveting the nation’s attention in the winter of 2006-2007.

What goes for the government buying land on behalf of its businessman friends also goes, mutatis mutandis, for the public sector’s real assets being bought up by the private sector using domestic paper money in a potentially hyperinflationary economy. If Dr Singh’s new Government wishes to see real public sector assets being sold, let the Government seek to value these assets not in inconvertible rupees which the Government itself has been producing in unlimited quantities but rather in forex or gold-units instead!

Today’s headline says “Short of cash, govt. plans to revive disinvestment ministry”. Big Business’s powerful lobbies will suggest that real public assets must be sold (to whom? to organised Big Business of course!) in order to solve the grave fiscal problems in an inflationary economy caused precisely by those grave fiscal problems! What I said in 2002 at IndiaSeminar may still be found to apply: I said the BJP’s privatisation ideas “deserve to be condemned…because they have made themselves believe that the proceeds of selling the public sector should merely go into patching up the bleeding haemorrhage which is India’s fiscal and monetary situation… (w)hile…Congress were largely responsible for that haemorrhage to have occurred in the first place.”

If the new Government would like to know how to proceed more wisely, they need to read and grasp, in the book edited by myself and Professor John Clarke in 2004-2005, the chapter by Professor Patrick Minford on Margaret Thatcher’s fiscal and monetary policy (macroeconomics) before they read the chapter by Professor Martin Ricketts on Margaret Thatcher’s privatisation (microeconomics). India’s fiscal and monetary or macroeconomic problems are far worse today than Britain’s were when Thatcher came in.

During the recent Election Campaign, I contrasted Dr Singh’s flattering praise in 2005 of the CPI-M’s Buddhadeb Bhattacharjee with Sonia Gandhi’s pro-Mamata line in 2009 saying the CPI-M had taken land away from the poor. This may soon signal a new fault-line in the new Cabinet too on economic policy with respect to not only land but also public sector privatisation – with Dr Singh’s pro-Big Business acolytes on one side and Mamata Banerjee’s stance in favour of small-scale unorganised business and labour on the other. Party heavyweights like Dr Singh himself and Sharad Pawar and Pranab Mukherjee will weigh in one side or the other with Sonia being asked in due course to referee.

I personally am delighted to see the New Rahul Gandhi deciding not to be in Government and to instead reflect further on the “common man” and “common woman” about whom I had described his father talking to me on September 18 1990 at his home. Certainly the “aam admi” is not someone to be found among India’s organised Big Business or organised Big Labour nor their paid lobbyists in the big cities.

Textbook corporate finance theory says that when a going concern takes over an ailing or bankrupt company (with low or zero or negative value), it does so in expectation that the net value of the combined entity shall, at least in due course, exceed the present value of the successful buyer.

The most peculiar aspect of the Satyam auction process has been the delay and obfuscation that greeted attempts by potential buyers to ascertain the extent of its liabilities (many of which may be contingent liabilities depending on the outcomes of American class-action suits.) Even so, Satyam appears to have been taken over. Caveat emptor! may be all that needs to be said. We are like this only.

“[I]f Atal Behari Vajpayee and Lal Krishna Advani could bring themselves to honestly walk away from BJP politics, there would have to be a genuine leadership contest and some new principles emerging in their party. There is an excellent and very simple political reason for Vajpayee and Advani to go, which is not that they are too old (which they are) but that they led their party to electoral defeat. Had they walked away in May 2004, there might have been by now some viable conservative political philosophy in India and some recognisable new alternative leadership for 2009. Instead there is none and the BJP has not only failed very badly at being a responsible Opposition, it will go into the 2009 General Election looking exceptionally decrepit and incompetent.”

Lest anyone think this was a tirade against the BJP, most of the article was actually a criticism of the Congress and the Communists!

Mr LK Advani’s claim that Indian resources have been illegally shipped overseas is hardly new or interesting — what is truly grotesque is the sheer irresponsibility of his claim that if somehow this could be reversed, it would suffice to

” Relieve the debts of all farmers and landless • Build world-class roads all over the country – from national and state highways to district and rural roads; • Completely eliminate the acute power shortage in the country and also to bring electricity to every unlit rural home; • Provide safe and adequate drinking water in all villages and towns in India • Construct good-quality houses, each worth Rs. 2.5 lakh, for 10 crore families; • Provide Rs. 4 crore to each of the nearly 6 lakh villages; the money can be used to build, in every single village, a school with internet-enabled education, a primary health centre with telemedicine facility, a veterinary clinic, a playground with gymnasium, and much more. “

This is simply appalling in its sheer mendacity. The BJP is going to give an amnesty to all those with such money and then confiscate it or requisition it or forcibly borrow it to make these resources equivalent to tax-revenues for the purposes of Indian public finance? What can one say beyond this being grotesque in its incomprehension of both facts and economic principles? Could someone who supports the BJP please teach them some Econ 101 asap?

Bankrupt companies get sold for nominal prices like Rs 100 or perhaps $2. But of course it is not impossible a notorious Government contractor or two will pump money in as a backdoor public subsidy aimed at creating a zombie.

Satyam may be able to summarily solve the problems caused by its high-level corporate fraud by transforming itself into a “Labour-Managed Firm”.

One of the new Government-appointed board members has stated publicly today that the company has little or no debt. If this is true it would be interesting because not only were the vast cash-assets non-existent, the liabilities-side of the balance-sheet also may be small, which could mean the company was simply far smaller in terms of value than it had made itself out to be. In a bankrupt firm, the remaining assets normally come to belong to the creditors but what if the main creditors happen to be the work-force? If that is in fact the situation in this case, Satyam may be a prime candidate to be transformed into a “Labour-Managed Firm” of the sort discussed by Jaroslav Vanek (The General Theory of Labour Managed Firms and Market Economies, 1970) and James Meade (The theory of the labour-managed firm and profit-sharing, Economic Journal 1972), and surveyed by e.g. Louis Putterman in the New Palgrave Dictionary and by Martin Ricketts in The Economics of Business Enterprise 2003.

As I had briefly mentioned earlier here, the transition could be made by Satyam’s existing technical and other staff being allowed to participate (with their personal savings and claims to future income) in any auction of the “works-in-progress” that constitute the client contracts the company presently has around the world and which constitute its major intangible asset. This may be the single best way to preserve the firm’s value as well as the income-streams of its staff.

The staff would have to make a transition from being employees to becoming self-managers which may not be easy in practice, although in theory the information-technology industry may be well-suited to labour-managed firms given the peculiarly intangible nature of their products. The marginal cost of production of (true) information is typically very high but the marginal cost of dissemination of information is near- zero.

If this happened and a corrupt bankrupt Satyam-I transformed itself into a viable Labour-Managed Satyam-II, the newly appointed board would become redundant even more quickly than it would have done otherwise — though this board may be even less likely to know of Vanek and Meade than to be familiar with modern corporate finance. Time perhaps to hit the textbooks, gentlemen, and burn that midnight candle! Is that something we can expect from some of the key lobbyists of India’s organized business sector?

Subroto Roy

Postscript 1 : Of course if the asset-side has been fraudulently exaggerated while the liabilities-side has been small, the fraud has been directly perpetrated on equity-holders who held stock that was overvalued by the market as a direct result of the fraud.

Postscript 2: I find (grotesquely) amusing the new found emphasis on “Independent Directors” in view of the obvious fraud in the advertised biographies of some rather notorious Independent Directors in the IT-business and other sectors of corporate India and the higher bureaucracy! There seems in fact to have been a wild hyperinflation of reputations generally, especially in Delhi, Mumbai, Bangalore, Pune and other such hip with-it places — people claiming to have earned PhDs when they have none, people calling themselves “Dr” on the basis of some defunct Soviet management institute having once paid them off, people claiming to be Harvard postgraduates on the basis of some outsourced executive development programme of a few weeks’ duration, people claiming academic publications and academic affiliations which are non-existent, etc etc. All that for another day! (But any former students of mine who may find the above pertinent to themselves may please know their old prof is cross with them! Tsk tsk!) (And then there was the one of the senior government economic planner who told his astrologer on the telephone his correct date of birth but had lied to the Government of India by a couple of years…. clearly he did not want to get his own Ptolomaic horoscope wrong even if his plans for India in the Copernican world went awry!)

In a March 5 2007 article in The Statesman, I said:

“Our farmers are peaceful hardworking people who should be paying taxes and user-fees normally but should not be otherwise disturbed or needlessly provoked by outsiders. It is the businessmen wishing to attack our farm populations who need to look hard in the mirror – to improve their accounting, audit, corporate governance, to enforce anti-embezzlement and shareholder protection laws etc.”

In a September 23-24 2007 article in The Sunday Statesman I said:

“… Government, instead of hobnobbing with business chambers, needed to get Indian corporations to improve their accounting, audit and governance, and reduce managerial pilfering and embezzlement, which is possible only if Government first set an example.”

In a February 4 2007 article in The Statesman, I said:

“Financial control of India’s fiscal condition, and hence monetary expansion, vitally requires control of the growth of these kinds of dynamic processes and comprehension of their analytical underpinnings. Yet such understanding and control seem quite absent from all organs of our Government, including establishment economists and the docile financial press…. the actual difference between Government Expenditure and Income in India has been made to appear much smaller than it really is. Although neglected by the Cabinet, Finance Ministry, RBI and even (almost) the C&AG, the significance of this discrepancy in measurement will not be lost on anyone seriously concerned to address India’s fiscal and monetary problems.”

All three articles are available elsewhere here and are republished below together. I have published elsewhere today my brief 2006 lecture on corporate governance. (See also my “The Indian Revolution”, “Monetary Integrity & the Rupee”, “Indian Inflation”, “The Dream Team: A Critique”, “India’s Macroeconomics”, “Growth & Government Delusion”, etc).

The fraud at Satyam amounts to it having been long bankrupt but not seemingly so. The fact it was long bankrupt was apparently overlooked or condoned by its auditors Pricewaterhouse Coopers! This may be big news today but the response of corporate India and the Indian business media seems utterly insincere (and there has been a lot of fake pontificating on TV by some notorious frauds). Remember the head of Satyam received awards with all the other honchos at those fake ceremonies that businessmen and the business media keep holding at this or that hotel. (See my several articles here under the categories “Satyam corporate fraud”, “Corporate governance” etc.)

Government agencies, as enforcers of the law, must be seen in such circumstances to have greater credibility than the violators, but who can say that Government accounting and audit and corporate governance in India is not as bad as that of the private sector? It may be in fact far, far worse. Poor accounting, endless deficit finance, unlimited paper money creation, false convertibility of the rupee etc is what emerges from our supposedly wise economic policy-makers.

When was the last time some major businessman or top politician spoke publicly about the importance of “Generally Accepted Accounting Principles”? The answer is never. Government (of this party or that) has become well-oiled by political lobbyists and is hand-in-glove with organized business, especially in a few cities. Until Government gets its own accounts straight, stops its endless deficit finance, reins in unlimited paper money-creation, creates an honest currency domestically and externally, there is no proper example or standard set for the private sector, and such scandals will erupt along with insincere responses from the cartels of corporate India.

What emerges from New Delhi’s economists seems often to have as much to do with economics as Bollywood has to do with cinema.

Subroto Roy

Fallacious Finance: Congress, BJP, CPI-M et al may be leading India to hyperinflation

It seems the Dream Team of the PM, Finance Minister, Mr. Montek Ahluwalia and their acolytes may take India on a magical mystery tour of economic hallucinations, fantasies and perhaps nightmares. I hasten to add the BJP and CPI-M have nothing better to say, and criticism of the Government or of Mr Chidambaram’s Budget does not at all imply any sympathy for their political adversaries. It may be best to outline a few of the main fallacies permeating the entire Governing Class in Delhi, and their media and businessman friends:

1. “India’s Savings Rate is near 32%”. This is factual nonsense. Savings is indeed normally measured by adding financial and non-financial savings. Financial savings include bank-deposits. But India is not a normal country in this. Nor is China. Both have seen massive exponential growth of bank-deposits in the last few decades. Does this mean Indians and Chinese are saving phenomenally high fractions of their incomes by assiduously putting money away into their shaky nationalized banks? Sadly, it does not. What has happened is government deficit-financing has grown explosively in both countries over decades. In a “fractional reserve” banking system (i.e. a system where your bank does not keep the money you deposited there but lends out almost all of it immediately), government expenditure causes bank-lending, and bank-lending causes bank-deposits to expand. Yes there has been massive expansion of bank-deposits in India but it is a nominal paper phenomenon and does not signify superhuman savings behaviour. Indians keep their assets mostly in metals, land, property, cattle, etc., and as cash, not as bank deposits.

2. “High economic growth in India is being caused by high savings and intelligently planned government investment”. This too is nonsense. Economic growth in India as elsewhere arises not because of what politicians and bureaucrats do in capital cities, but because of spontaneous technological progress, improved productivity and learning-by-doing on part of the general population. Technological progress is a very general notion, and applies to any and every production activity or commercial transaction that now can be accomplished more easily or using fewer inputs than before. New Delhi still believes in antiquated Soviet-era savings-investment models without technological progress, and some non-sycophant must tell our top Soviet-era bureaucrat that such growth models have been long superceded and need to be scrapped from India’s policy-making too. Can politicians and bureaucrats assist India’s progress? Indeed they can: the telecom revolution in recent years was something in which they participated. But the general presumption is against them. Progress, productivity gains and hence economic growth arise from enterprise and effort of ordinary people — mostly despite not because of an exploitative, parasitic State.

3. “Agriculture is a backward sector that has been retarding India’s recent economic growth”. This is not merely nonsense it is dangerous nonsense, because it has led to land-grabbing by India’s rulers at behest of their businessman friends in so-called “SEZ” schemes. The great farm economist Theodore W. Schultz once quoted Andre and Jean Mayer: “Few scientists think of agriculture as the chief, or the model science. Many, indeed, do not consider it a science at all. Yet it was the first science – Mother of all science; it remains the science which makes human life possible”. Centuries before Europe’s Industrial Revolution, there was an Agricultural Revolution led by monks and abbots who were the scientists of the day. Thanks partly to American help, India has witnessed a Green Revolution since the 1960s, and our agriculture has been generally a calm, mature, stable and productive industry. Our farmers are peaceful hardworking people who should be paying taxes and user-fees normally but should not be otherwise disturbed or needlessly provoked by outsiders. It is the businessmen wishing to attack our farm populations who need to look hard in the mirror – to improve their accounting, audit, corporate governance, to enforce anti-embezzlement and shareholder protection laws etc.

4. “India’s foreign exchange reserves may be used for ‘infrastructure’ financing”. Mr Ahluwalia promoted this idea and now the Budget Speech mentioned how Mr Deepak Parekh and American banks may be planning to get Indian businesses to “borrow” India’s forex reserves from the RBI so they can purchase foreign assets. It is a fallacy arising among those either innocent of all economics or who have quite forgotten the little they might have been mistaught in their youth. Forex reserves are a residual in a country’s balance of payments and are not akin to tax revenues, and thus are not available to be borrowed or spent by politicians, bureaucrats or their businessman friends — no matter how tricky and shady a way comes to be devised for doing so. If anything, the Government and RBI’s priority should have been to free the Rupee so any Indian could hold gold or forex at his/her local bank. India’s vast sterling balances after the Second World War vanished quickly within a few years, and the country plunged into decades of balance of payments crisis – that may now get repeated. The idea of “infrastructure” is in any case vague and inferior to the “public goods” Adam Smith knew to be vital. Serious economists recommend transparent cost-benefit analyses before spending any public resources on any project. E.g., analysis of airport/airline industry expansion would have found the vast bulk of domestic airline costs to be forex-denominated but revenues rupee-denominated – implying an obvious massive currency-risk to the industry and all its “infrastructure”. All the PM’s men tell us nothing of any of this.

5. “HIV-AIDS is a major Indian health problem”. Government doctors privately know the scare of an AIDS epidemic is based on false assumptions and analysis. Few if any of us have met, seen or heard of an actual incontrovertible AIDS victim in India (as opposed to someone infected by hepatitis-contaminated blood supplies). Syringe-exchange by intravenous drug users is not something widely prevalent in Indian society, while the practise that caused HIV to spread in California’s Bay Area in the 1980s is not something depicted even at Khajuraho. Numerous real diseases do afflict Indians – e.g. 11 children died from encephalitis in one UP hospital on a single day in July 2006, while thousands of children suffer from “cleft lip” deformity that can be solved surgically for 20,000 rupees, allowing the child a normal life. Without any objective survey being done of India’s real health needs, Mr Chidamabaram has promised more than Rs 9.6 Billion (Rs 960 crore) to the AIDS cottage industry.

6. “Fiscal consolidation & stabilization has been underway since 1991”. There is extremely little reason to believe this. If you or I borrow Rs. 100,000 for a year, and one year later repay the sum only to borrow the same again along with another Rs 40,000, we would be said to have today a debt of Rs. 140,000 at least. Our Government has been routinely “rolling over” its domestic debt in this manner (in the asset-portfolios of the nationalised banking system) but displaying and highlighting only its new additional borrowing in a year as the “ Fiscal Deficit” (see graph, also “Fiscal Instability”, The Sunday Statesman, 4 February 2007). More than two dozen State Governments have been doing the same though, unlike the Government of India, they have no money-creating powers and their liabilities ultimately accrue to the Union as well. The stock of public debt in India may be Rs 30 trillion (Rs 30 lakh crore) at least, and portends a hyperinflation in the future. Mr Chidambaram’s announcement of a “Debt Management Office” yet to be created is hardly going to suffice to avert macroeconomic turmoil and a possible monetary collapse. The Congress, BJP, CPI-M and all their friends shall be responsible.

Against Quackery

First published in two parts in The Sunday Statesman, September 23 2007, The Statesman September 24 2007, http://www.thestatesman.net

By Subroto Roy

Manmohan and Sonia have violated Rajiv Gandhi’s intended reforms; the Communists have been appeased or bought; the BJP is incompetent

WASTE, fraud and abuse are inevitable in the use and allocation of public property and resources in India as elsewhere, but Government is supposed to fight and resist such tendencies. The Sonia-Manmohan Government have done the opposite, aiding and abetting a wasteful anti-economics ~ i.e., an economic quackery. Vajpayee-Advani and other Governments, including Narasimha-Manmohan in 1991-1996, were just as complicit in the perverse policy-making. So have been State Governments of all regional parties like the CPI-M in West Bengal, DMK/ AIADMK in Tamil Nadu, Congress/NCP/ BJP/Sena in Maharashtra, TDP /Congress in Andhra Pradesh, SP/BJP/BSP in Uttar Pradesh etc. Our dismal politics merely has the pot calling the kettle black while national self-delusion and superstition reign in the absence of reason.

The general pattern is one of well-informed, moneyed, mostly city-based special interest groups (especially including organised capital and organised labour) dominating government agendas at the cost of ill-informed, diffused anonymous individual citizens ~ peasants, small businessmen, non-unionized workers, old people, housewives, medical students etc. The extremely expensive “nuclear deal” with the USA is merely one example of such interest group politics.

Nuclear power is and shall always remain of tiny significance as a source of India’s electricity (compared to e.g. coal and hydro); hence the deal has practically nothing to do with the purported (and mendacious) aim of improving the country’s “energy security” in the long run. It has mostly to do with big business lobbies and senior bureaucrats and politicians making a grab, as they always have done, for India’s public purse, especially access to foreign currency assets. Some $300 million of India’s public money had to be paid to GE and Bechtel Corporation before any nuclear talks could begin in 2004-2005 ~ the reason was the Dabhol fiasco of the 1990s, a sheer waste for India’s ordinary people. Who was responsible for that loss? Pawar-Mahajan-Munde-Thackeray certainly but also India’s Finance Minister at the time, Manmohan Singh, and his top Finance Ministry bureaucrat, Montek Ahluwalia ~ who should never have let the fiasco get off the ground but instead actively promoted and approved it.