Where are the Reserve Bank’s Macroeconomic Models?

December 11, 2009 — drsubrotoroy“On the blissful innocence of the RBI” (2009) From Facebook:

A Small Challenge to the RBI’s Governor Subbarao

Mistaken Macroeconomics: An Open Letter to Prime Minister Dr Manmohan Singh 12 June 2009

June 12, 2009 — drsubrotoroy12 June 2009

The Hon’ble Dr Manmohan Singh, MP, Rajya Sabha

Prime Minister of India

Respected Pradhan Mantriji:

In September 1993 at the residence of the Indian Ambassador to Washington, I had the privilege of being introduced to you by our Ambassador the Hon’ble Siddhartha Shankar Ray, Bar-at-Law. Ambassador Ray was kind enough to introduce me saying the 1991 “Congress manifesto had been written on (my laptop) computer” – a reference to my work as adviser on economic and other policy to the late Rajiv Gandhi in his last months. I presented you a book Foundations of India’s Political Economy: Towards an Agenda for the 1990s created and edited by myself and WE James at the University of Hawaii since 1986 — the unpublished manuscript of that book had reached Rajivji by my hand when he and I first met on September 18 1990. Tragically, my pleadings in subsequent months to those around him that he seemed to my layman’s eyes vulnerable to the assassin went unheeded.

When you and I met in 1993, we had both forgotten another meeting twenty years earlier in Paris. My father had been a long-time friend of the late Brahma Kaul, ICS, and the late MG Kaul, ICS, who knew you in your early days in the Government of India. In the late summer of 1973, you had acceded to my father’s request to advise me about economics before I embarked for the London School of Economics as a freshman undergraduate. You visited our then-home in Paris for about 40 minutes despite your busy schedule as part of an Indian delegation to the Aid-India Consortium. We ended up having a tense debate about the merits (as you saw them) and demerits (as I saw them) of the Soviet influence on Indian economic “planning”. You had not expected such controversy from a lad of 18 but you were kindly disposed and offered when departing to write a letter of introduction to Amartya Sen, then teaching at the LSE, which you later sent me and which I was delighted to carry to Professor Sen.

I may add my father, back in 1973 in Paris, had predicted to me that you would become Prime Minister of India one day, and he, now in his 90s, is joined by myself in sending our warm congratulations at the start of your second term in that high office.

The controversy though that you and I had entered that Paris day in 1973 about scientific economics as applied to India, must be renewed afresh!

This is because of your categorical statement on June 9 2009 to the new 15th Lok Sabha:

“I am convinced, since our savings rate is as high as 35%, given the collective will, if all of us work together, we can achieve a growth-rate of 8%-9%, even if the world economy does not do well.” (Statement of Dr Manmohan Singh to the Lok Sabha, June 9 2009)

I am afraid there may be multiple reasons why such a statement is gravely and incorrigibly in error within scientific economics. From your high office as Prime Minister in a second term, faced perhaps with no significant opposition from either within or without your party, it is possible the effects of such an error may spell macroeconomic catastrophe for India.

As it happens, the British Labour Party politician Dr Meghnad Desai made an analogous statement to yours about India when he claimed in 2006 that China

“now has 10.4% growth on a 44 % savings rate… ”

Indeed the idea that China and India have had extremely high economic growth-rates based on purportedly astronomical savings rates has become a commonplace in recent years, repeated endlessly in international and domestic policy circles though perhaps without adequate basis.

1. Germany & Japan

What, at the outset, is supposed to be measured when we speak of “growth”? Indian businessmen and their media friends seem to think “growth” refers to something like nominal earnings before tax for the organised corporate sector, or any unspecified number that can be sold to visiting foreigners to induce them to park their funds in India: “You will get a 10% return if you invest in India” to which the visitor says “Oh that must mean India has 10% growth going on”. Of such nonsense are expensive international conferences in Davos and Delhi often made.

You will doubtless agree the economist at least must define economic growth properly and with care — what is referred to must be annual growth of per capita inflation-adjusted Gross Domestic Product. (Per capita National Income or Net National Product would be even better if available).

West Germany and Japan had the highest annual per capita real GDP growth-rates in the world economy starting from devastated post-World War II initial conditions. What were their measured rates?

West Germany: 6.6% in 1950-1960, falling to 3.5% by 1960-1970 falling to 2.4% by 1970-1978.

Japan: 6.8 % in 1952-1960 rising to 9.4% in 1960-1970 falling to 3.8 % in 1970-1978.

Thus in recent decadesonly Japan measured a spike in the 1960s of more than 9% annual growth of real per capita GDP. Now India and China are said to be achieving 8%-10 % and more year after year routinely!

Perhaps we are observing an incredible phenomenon of world economic history. Or perhaps it is just something incredible, something false and misleading, like a mirage in the desert.

You may agree that processes of measurement of real income in India both at federal and provincial levels, still remain well short of the world standards described by the UN’s System of National Accounts 1993. The actuality of our real GDP growth may be better than what is being measured or it may be worse than what is being measured – from the point of view of public decision-making we at present simply do not know which it is, and to overly rely on such numbers in national decisions may be unwise. In any event, India’s population is growing at near 2% so even if your Government’s measured number of 8% or 9% is taken at face-value, we have to subtract 2% population growth to get per capita figures.

2. Growth of the aam admi’s consumption-basket

The late Professor Milton Friedman had been an invited adviser in 1955 to the Government of India during the Second Five Year Plan’s formulation. The Government of India suppressed what he had to say and I had to publish it 34 years later in May 1989 during the 1986-1992 perestroika-for-India project that I led at the University of Hawaii in the United States. His November 1955 Memorandum to the Government of India is a chapter in the book Foundations of India’s Political Economy: Towards an Agenda for the 1990s that I and WE James created.

At the 1989 project-conference itself, Professor Friedman made the following astute observation about all GNP, GDP etc growth-numbers that speaks for itself:

“I don’t believe the term GNP ought to be used unless it is supplemented by a different statistic: the rate of growth of the average consumption basket consumed by the ordinary individual in the country. I think GNP rates of growth can give very misleading information. For example, you have rapid rates of growth of GNP in the Soviet Union with a declining standard of life for the people. Because GNP includes monuments and includes also other things. I’m not saying that that is the case with India; I’m just saying I would like to see the two figures together.”

You may perhaps agree upon reflection that not only may our national income growth measurements be less robust than we want, it may be better to be measuring something else instead, or as well, as a measure of the economic welfare of India’s people, namely, “the rate of growth of the average consumption basket consumed by the ordinary individual in the country”, i.e., the rate of growth of the average consumption basket consumed by the aam admi.

It would be excellent indeed if you were to instruct your Government’s economists and other spokesmen to do so this as it may be something more reliable as an indicator of our economic realities than all the waffle generated by crude aggregate growth-rates.

3. Logic of your model

Thirdly, the logic needs to be spelled out of the economic model that underlies such statements as yours or Meghnad Desai’s that seek to operationally relate savings rates to aggregate growth rates in India or China. This seems not to have been done publicly in living memory by the Planning Commission or other Government economists. I have had to refer, therefore, to pages 251-253 of my own Cambridge doctoral thesis under Professor Frank Hahn thirty years ago, titled “On liberty and economic growth: preface to a philosophy for India”, where the logic of such models as yours was spelled out briefly as follows:

Let

Kt be capital stock

Yt be national output

It be the level of real investment

St be the level of real savings

By definition

It = K t+1 – Kt

By assumption

Kt = k Yt 0 < k < 1

St = sYt 0 < s <1

In equilibrium ex ante investment equals ex ante savings

It = St

Hence in equilibrium

sYt = K t+1 – Kt

Or

s/k = g

where g is defined to be the rate of growth (Y t+1-Yt)/Yt .

The left hand side then defines the “warranted rate of growth” which must maintain the famous “knife-edge” with the right hand side “natural rate of growth”.

Your June 9 2009 Lok Sabha statement that a 35% rate of savings in India may lead to an 8%-9% rate of economic growth in India, or Meghnad Desai’s statement that a 44% rate of savings in China led to a 10.4% growth there, can only be made meaningful in the context of a logical economic model like the one I have given above.

[In the open-economy version of the model, let Mt be imports, Et be exports, Ft net capital inflows.

Assume

Mt = aIt + bYt 0 < a, b < 1

Et = E for all t

Balance of payments is

Bt = Mt – Et – Ft

In equilibrium It = St + Bt

Or

Ft = (s+b) Yt – (1-a) It – E is a kind of “warranted” level of net capital inflow.]

You may perhaps agree upon reflection that building the entire macroeconomic policy of the Government of India merely upon a piece of economic logic as simplistic as the

s/k = g

equation above, may spell an unacceptable risk to the future economic well-being of our vast population. An alternative procedural direction for macroeconomic policy, with more obviously positive and profound consequences, may have been that which I sought to persuade Rajiv Gandhi about with some success in 1990-1991. Namely, to systematically seek to improve towards normalcy the budgets, financial positions and decision-making capacities of the Union and all state and local governments as well as all public institutions, organisations, entities, and projects in general, with the aim of making our domestic money a genuine hard currency of the world again after seven decades, so that any ordinary resident of India may hold and trade precious metals and foreign exchange at his/her local bank just like all those glamorous privileged NRIs have been permitted to do. Such an alternative path has been described in “The Indian Revolution”, “Against Quackery”, “The Dream Team: A Critique”, “India’s Macroeconomics”, “Indian Inflation”, etc.

4. Gross exaggeration of real savings rate by misreading deposit multiplication

Specifically, I am afraid you may have been misled into thinking India’s real savings rate, s, is as high as 35% just as Meghnad Desai may have misled himself into thinking China’s real savings rate is as high as 44%.

Neither of you may have wanted to make such a claim if you had referred to the fact that over the last 25 years, the average savings rate across all OECD countries has been less than 10%. Economic theory always finds claims of discontinuous behaviour to be questionable. If the average OECD citizen has been trying to save 10% of disposable income at best, it appears prima facie odd that India’s PM claims a savings rate as high as 35% for India or a British politician has claimed a savings rate as high as 44% for China. Something may be wrong in the measurement of the allegedly astronomical savings rates of India and China. The late Professor Nicholas Kaldor himself, after all, suggested it was rich people who saved and poor people who did not for the simple reason the former had something left over to save which the latter did not!

And indeed something is wrong in the measurements. What has happened, I believe, is that there has been a misreading of the vast nominal expansion of bank deposits via deposit-multiplication in the Indian banking system, an expansion that has been caused by explosive deficit finance over the last four or five decades. That vast nominal expansion of bank-deposits has been misread as indicating growth of real savings behaviour instead. I have written and spoken about and shown this quite extensively in the last half dozen years since I first discovered it in the case of India. E.g., in a lecture titled “Can India become an economic superpower or will there be a monetary meltdown?” at Cardiff University’s Institute of Applied Macroeconomics and at London’s Institute of Economic Affairs in April 2005, as well as in May 2005 at a monetary economics seminar invited at the RBI by Dr Narendra Jadav. The same may be true of China though I have looked at it much less.

How I described this phenomenon in a 2007 article in The Statesman is this:

“Savings is indeed normally measured by adding financial and non-financial savings. Financial savings include bank-deposits. But India is not a normal country in this. Nor is China. Both have seen massive exponential growth of bank-deposits in the last few decades. Does this mean Indians and Chinese are saving phenomenally high fractions of their incomes by assiduously putting money away into their shaky nationalized banks? Sadly, it does not. What has happened is government deficit-financing has grown explosively in both countries over decades. In a “fractional reserve” banking system (i.e. a system where your bank does not keep the money you deposited there but lends out almost all of it immediately), government expenditure causes bank-lending, and bank-lending causes bank-deposits to expand. Yes there has been massive expansion of bank-deposits in India but it is a nominal paper phenomenon and does not signify superhuman savings behaviour. Indians keep their assets mostly in metals, land, property, cattle, etc., and as cash, not as bank deposits.”

An article of mine in 2008 in Business Standard put it like this:

“India has followed in peacetime over six decades what the US and Britain followed during war. Our vast growth of bank deposits in recent decades has been mostly a paper (or nominal) phenomenon caused by unlimited deficit finance in a fractional reserve banking system. Policy makers have widely misinterpreted it as indicating a real phenomenon of incredibly high savings behaviour. In an inflationary environment, people save their wealth less as paper deposits than as real assets like land, cattle, buildings, machinery, food stocks, jewellery etc.”

If you asked me “What then is India’s real savings rate?” I have little answer to give except to say I know what it is not – it is not what the Government of India says it is. It is certainly unlikely to be anywhere near the 35% you stated it to be in your June 9 2009 Lok Sabha statement. If the OECD’s real savings rate has been something like 10% out of disposable income, I might accept India’s is, say, 15% at a maximum when properly measured – far from the 35% being claimed. What I believe may have been mismeasured by you and Meghnad Desai and many others as indicating high real savings is actually the nominal or paper expansion of bank-deposits in a fractional reserve banking system induced by runaway government deficit-spending in both India and China over the last several decades.

5. Technological progress and the mainsprings of real economic growth

So much for the g and s variables in the s/k = g equation in your economic model. But the assumed constant k is a big problem too!

During the 1989 perestroika-for-India project-conference, Professor Friedman referred to his 1955 experience in India and said this about the assumption of a constant k:

“I think there was an enormously important point… That was the almost universal acceptance at that time of the view that there was a sort of technologically fixed capital output ratio. That if you wanted to develop, you just had to figure out how much capital you needed, used as a statistical technological capital output ratio, and by God the next day you could immediately tell what output you were going to achieve. That was a large part of the motivation behind some of the measures that were taken then.”

The crucial problem of the sort of growth-model from which your formulation relating savings to growth arises is that, with a constant k, you have necessarily neglected the real source of economic growth, which is technological progress!

I said in the 2007 article referred to above:

“Economic growth in India as elsewhere arises not because of what politicians and bureaucrats do in capital cities, but because of spontaneous technological progress, improved productivity and learning-by-doing on part of the general population. Technological progress is a very general notion, and applies to any and every production activity or commercial transaction that now can be accomplished more easily or using fewer inputs than before.”

In “Growth and Government Delusion” published in The Statesman last year, I described the growth process more fully like this:

“The mainsprings of real growth in the wealth of the individual, and so of the nation, are greater practical learning, increases in capital resources and improvements in technology. Deeper skills and improved dexterity cause output produced with fewer inputs than before, i.e. greater productivity. Adam Smith said there is “invention of a great number of machines which facilitate and abridge labour, and enable one man to do the work of many”. Consider a real life example. A fresh engineering graduate knows dynamometers are needed in testing and performance-certification of diesel engines. He strips open a meter, finds out how it works, asks engine manufacturers what design improvements they want to see, whether they will buy from him if he can make the improvement. He finds out prices and properties of machine tools needed and wages paid currently to skilled labour, calculates expected revenues and costs, and finally tries to persuade a bank of his production plans, promising to repay loans from his returns. Overcoming restrictions of religion or caste, the secular agent is spurred by expectation of future gains to approach various others with offers of contract, and so organize their efforts into one. If all his offers ~ to creditors, labour, suppliers ~ are accepted he is, for the moment, in business. He may not be for long ~ but if he succeeds his actions will have caused an improvement in design of dynamometers and a reduction in the cost of diesel engines, as well as an increase in the economy’s produced means of production (its capital stock) and in the value of contracts made. His creditors are more confident of his ability to repay, his buyers of his product quality, he himself knows more of his workers’ skills, etc. If these people enter a second and then a third and fourth set of contracts, the increase in mutual trust in coming to agreement will quickly decline in relation to the increased output of capital goods. The first source of increasing returns to scale in production, and hence the mainspring of real economic growth, arises from the successful completion of exchange. Transforming inputs into outputs necessarily takes time, and it is for that time the innovator or entrepreneur or “capitalist” or “adventurer” must persuade his creditors to trust him, whether bankers who have lent him capital or workers who have lent him labour. The essence of the enterprise (or “firm”) he tries to get underway consists of no more than the set of contracts he has entered into with the various others, his position being unique because he is the only one to know who all the others happen to be at the same time. In terms introduced by Professor Frank Hahn, the entrepreneur transforms himself from being “anonymous” to being “named” in the eyes of others, while also finding out qualities attaching to the names of those encountered in commerce. Profits earned are partly a measure of the entrepreneur’s success in this simultaneous process of discovery and advertisement. Another potential entrepreneur, fresh from engineering college, may soon pursue the pioneer’s success and start displacing his product in the market ~ eventually chasers become pioneers and then get chased themselves, and a process of dynamic competition would be underway. As it unfolds, anonymous and obscure graduates from engineering colleges become by dint of their efforts and a little luck, named and reputable firms and perhaps founders of industrial families. Multiply this simple story many times, with a few million different entrepreneurs and hundreds of thousands of different goods and services, and we shall be witnessing India’s actual Industrial Revolution, not the fake promise of it from self-seeking politicians and bureaucrats.”

Technological progress in a myriad of ways and discovery of new resources are important factors contributing to India’s growth today. But while India’s “real” economy does well, the “nominal” paper-money economy controlled by Government does not. Continuous deficit financing for half a century has led to exponential growth of public debt and broad money, and, as noted, the vast growth of nominal bank-deposits has been misinterpreted as indicating unusually high real savings behaviour when it in fact may just signal vast amounts of government debt being held by our nationalised banks. These bank assets may be liquid domestically but are illiquid internationally since our government debt is not held by domestic households as voluntary savings nor has it been a liquid asset held worldwide in foreign portfolios.

What politicians of all parties, especially your own and the BJP and CPI-M since they are the three largest, have been presiding over is exponential growth of our paper money supply, which has even reached 22% per annum. Parliament and the Government should be taking honest responsibility for this because it may certainly portend double-digit inflation (i.e., decline in the value of paper-money) perhaps as high as 14%-15% per annum, something that is certain to affect the aam admi’s economic welfare adversely.

6. Selling Government assets to Big Business is a bad idea in a potentially hyperinflationary economy

Respected PradhanMantriji, the record would show that I, and really I alone, 25 years ago, may have been the first among Indian economists to advocate the privatisation of the public sector. (Viz, “Silver Jubilee of Pricing, Planning and Politics: A Study of Economic Distortions in India”.) In spite of this, I have to say clearly now that in present circumstances of a potentially hyperinflationary economy created by your Government and its predecessors, I believe your Government’s present plans to sell Government assets may be an exceptionally unwise and imprudent idea. The reasoning is very simple from within monetary economics.

Government every year has produced paper rupees and bank deposits in practically unlimited amounts to pay for its practically unlimited deficit financing, and it has behaved thus over decades. Such has been the nature of the macroeconomic process that all Indian political parties have been part of, whether they are aware of it or not.

Indian Big Business has an acute sense of this long-term nominal/paper expansion of India’s economy, and acts towards converting wherever possible its own hoards of paper rupees and rupee-denominated assets into more valuable portfolios for itself of real or durable assets, most conspicuously including hard-currency denominated assets, farm-land and urban real-estate, and, now, the physical assets of the Indian public sector. Such a path of trying to transform local domestic paper assets – produced unlimitedly by Government monetary and fiscal policy and naturally destined to depreciate — into real durable assets, is a privately rational course of action to follow in an inflationary economy. It is not rocket-science to realise the long-term path of rupee-denominated assets is downwards in comparison to the hard-currencies of the world – just compare our money supply growth and inflation rates with those of the rest of the world.

The Statesman of November 16 2006 had a lead editorial titled Government’s land-fraud: Cheating peasants in a hyperinflation-prone economy which said:

“There is something fundamentally dishonourable about the way the Centre, the state of West Bengal and other state governments are treating the issue of expropriating peasants, farm-workers, petty shop-keepers etc of their small plots of land in the interests of promoters, industrialists and other businessmen. Singur may be but one example of a phenomenon being seen all over the country: Hyderabad, Karnataka, Kerala, Haryana, everywhere. So-called “Special Economic Zones” will merely exacerbate the problem many times over. India and its governments do not belong only to business and industrial lobbies, and what is good for private industrialists may or may not be good for India’s people as a whole. Economic development does not necessarily come to be defined by a few factories or high-rise housing complexes being built here or there on land that has been taken over by the Government, paying paper-money compensation to existing stakeholders, and then resold to promoters or industrialists backed by powerful political interest-groups on a promise that a few thousand new jobs will be created. One fundamental problem has to do with inadequate systems of land-description and definition, implementation and recording of property rights. An equally fundamental problem has to do with fair valuation of land owned by peasants etc. in terms of an inconvertible paper-money. Every serious economist knows that “land” is defined as that specific factor of production and real asset whose supply is fixed and does not increase in response to its price. Every serious economist also knows that paper-money is that nominal asset whose price can be made to catastrophically decline by a massive increase in its supply, i.e. by Government printing more of the paper it holds a monopoly to print. For Government to compensate people with paper-money it prints itself by valuing their land on the basis of an average of the price of the last few years, is for Government to cheat them of the fair present-value of the land. That present-value of land must be calculated in the way the present-value of any asset comes to be calculated, namely, by summing the likely discounted cash-flows of future values. And those future values should account for the likelihood of a massive future inflation causing decline in the value of paper-money in view of the fact we in India have a domestic public debt of some Rs. 30 trillion (Rs. 30 lakh crore) and counting, and money supply growth rates averaging 16-17% per annum. In fact, a responsible Government would, given the inconvertible nature of the rupee, have used foreign exchange or gold as the unit of account in calculating future-values of the land. India’s peasants are probably being cheated by their Government of real assets whose value is expected to rise, receiving nominal paper assets in compensation whose value is expected to fall.”

Shortly afterwards the Hon’ble MP for Kolkata Dakshin, Km Mamata Banerjee, started her protest fast, riveting the nation’s attention in the winter of 2006-2007. What goes for government buying land on behalf of its businessman friends also goes, mutatis mutandis, for the public sector’s real assets being bought up by the private sector using domestic paper money in a potentially hyperinflationary economy. If your new Government wishes to see real assets of the public sector being sold for paper money, let it seek to value these assets not in inconvertible rupees that Government itself has been producing in unlimited quantities but perhaps in forex or gold-units instead!

In the 2004-2005 volume Margaret Thatcher’s Revolution: How it Happened and What it Meant, edited by myself and Professor John Clarke, there is a chapter by Professor Patrick Minford on Margaret Thatcher’s fiscal and monetary policy (macroeconomics) that was placed ahead of the chapter by Professor Martin Ricketts on Margaret Thatcher’s privatisation (microeconomics). India’s fiscal and monetary or macroeconomic problems are far worse today than Britain’s were when Margaret Thatcher came to power. We need to get our macroeconomic problems sorted before we attempt the microeconomic privatisation of public assets.

It is wonderful that your young party colleague, the Hon’ble MP from Amethi, Shri Rahul Gandhi, has declined to join the present Government and instead wishes to reflect further on the “common man” and “common woman” about whom I had described his late father talking to me on September 18 1990. Certainly the aam admi is not someone to be found among India’s lobbyists of organised Big Business or organised Big Labour who have tended to control government agendas from the big cities.

With my warmest personal regards and respect, I remain,

Cordially yours

Subroto Roy, PhD (Cantab.), BScEcon (London)

see also https://independentindian.com/thoughts-words-deeds-my-work-1973-2010/rajiv-gandhi-and-the-origins-of-indias-1991-economic-reform/did-jagdish-bhagwati-originate-pioneer-intellectually-father-indias-1991-economic-reform-did-manmohan-singh-or-did-i-through-my-e/

Against Quackery (2007)

September 24, 2007 — drsubrotoroyAgainst Quackery

First published in two parts in The Sunday Statesman, September 23 2007, The Statesman September 24 2007

by

Subroto Roy

Manmohan and Sonia have violated Rajiv Gandhi’s intended reforms; the Communists have been appeased or bought; the BJP is incompetent

WASTE, fraud and abuse are inevitable in the use and allocation of public property and resources in India as elsewhere, but Government is supposed to fight and resist such tendencies. The Sonia-Manmohan Government have done the opposite, aiding and abetting a wasteful anti-economics ~ i.e., an economic quackery. Vajpayee-Advani and other Governments, including Narasimha-Manmohan in 1991-1996, were just as complicit in the perverse policy-making. So have been State Governments of all regional parties like the CPI-M in West Bengal, DMK/ AIADMK in Tamil Nadu, Congress/NCP/ BJP/Sena in Maharashtra, TDP /Congress in Andhra Pradesh, SP/BJP/BSP in Uttar Pradesh etc. Our dismal politics merely has the pot calling the kettle black while national self-delusion and superstition reign in the absence of reason.

The general pattern is one of well-informed, moneyed, mostly city-based special interest groups (especially including organised capital and organised labour) dominating government agendas at the cost of ill-informed, diffused anonymous individual citizens ~ peasants, small businessmen, non-unionized workers, old people, housewives, medical students etc. The extremely expensive “nuclear deal” with the USA is merely one example of such interest group politics.

Nuclear power is and shall always remain of tiny significance as a source of India’s electricity (compared to e.g. coal and hydro); hence the deal has practically nothing to do with the purported (and mendacious) aim of improving the country’s “energy security” in the long run. It has mostly to do with big business lobbies and senior bureaucrats and politicians making a grab, as they always have done, for India’s public purse, especially access to foreign currency assets. Some $300 million of India’s public money had to be paid to GE and Bechtel Corporation before any nuclear talks could begin in 2004-2005 ~ the reason was the Dabhol fiasco of the 1990s, a sheer waste for India’s ordinary people. Who was responsible for that loss? Pawar-Mahajan-Munde-Thackeray certainly but also India’s Finance Minister at the time, Manmohan Singh, and his top Finance Ministry bureaucrat, Montek Ahluwalia ~ who should never have let the fiasco get off the ground but instead actively promoted and approved it.

Cost-benefit analysis prior to any public project is textbook operating procedure for economists, and any half-competent economist would have accounted for the scenario of possible currency-depreciation which made Dabhol instantly unviable. Dr Singh and Mr Ahluwalia failed that test badly and it cost India dearly. The purchase of foreign nuclear reactors on a turnkey basis upon their recommendation now reflects similar financial dangers for the country on a vastly larger scale over decades.

Our Government seems to function most expeditiously in purchasing foreign arms, aircraft etc ~ not in improving the courts, prisons, police, public utilities, public debt. When the purchase of 43 Airbus aircraft surfaced, accusations of impropriety were made by Boeing ~ until the local Airbus representative said on TV that Boeing need not complain because they were going to be rewarded too and soon 68 aircraft were ordered from Boeing!

India imports all passenger and most military aircraft, besides spare parts and high-octane jet fuel. Domestic aviation generates near zero forex revenues and incurs large forex costs ~ a debit in India’s balance of payments. Domestic airline passengers act as importers subsidised by our meagre exporters of textiles, leather, handicrafts, tea, etc. What a managerially-minded PM and Aviation Minister needed to do before yielding to temptations of buying new aircraft was to get tough with the pampered managements and unions of the nationalized airlines and stand up on behalf of ordinary citizens and taxpayers, who, after all, are mostly rail or road-travellers not jet-setters.

The same pattern of negligent policy-behaviour led Finance Minister P. Chidambaram in an unprecedented step to mention in his 2007 Union Budget Speech the private American companies Blackstone and GE ~ endorsing the Ahluwalia/Deepak Parekh idea that India’s forex reserves may be made available to be lent out to favoured private businesses for purported “infrastructure” development. We may now see chunks of India’s foreign exchange reserves being “borrowed” and never returned ~ a monumental scam in front of the CBI’s noses.

The Reserve Bank’s highest echelons may have become complicit in all this, permitting and encouraging a large capital flight to take place among the few million Indians who read the English newspapers and have family-members abroad. Resident Indians have been officially permitted to open bank accounts of US $100,000 abroad, as well as transfer gifts of $50,000 per annum to their adult children already exported abroad ~ converting their largely untaxed paper rupees at an artificially favourable exchange-rate.

In particular, Mr Ratan Tata (under a misapprehension he may do whatever Lakshmi Mittal does) has been allowed to convert Indian rupees into some US$13,000,000,000 to make a cash purchase of a European steel company. The same has been allowed of the Birlas, Wipro, Dr Reddy’s and numerous other Indian corporations in the organised sector ~ three hundred million dollars here, five hundred million dollars there, etc. Western businessmen now know all they have to do is flatter the egos of Indian boxwallahs enough and they might have found a buyer for their otherwise bankrupt or sick local enterprise. Many newcomers to New York City have been sold the Brooklyn Bridge before. “There’s a sucker born every minute” is the classic saying of American capitalism.

The Sonia-Manmohan Government, instead of hobnobbing with business chambers, needed to get Indian corporations to improve their accounting, audit and governance, and reduce managerial pilfering and embezzlement, which is possible only if Government first set an example.

Why have Indian foreign currency reserves zoomed up in recent years? Not mainly because we are exporting more textiles, tea, software engineers, call centre services or new products to the world, but because Indian corporations have been allowed to borrow abroad, converting their hoards of paper rupees into foreign debt. Forex reserves are a residual in a country’s international balance of payments and are not like tax-resources available to be spent by Government; India’s reserves largely constitute foreign liabilities of Indian residents. This may bear endless repetition as the PM and his key acolytes seem impervious to normal postgraduate-level economics textbooks.

Other official fallacies include thinking India’s savings rate is near 32 per cent and that clever bureaucratic use of it can cause high growth. In fact, real growth arises not because of what politicians and bureaucrats do but because of spontaneous technological progress, improved productivity and learning-by-doing of the general population ~ mostly despite not because of an exploitative parasitic State. What has been mismeasured as high savings is actually expansion of bank-deposits in a fractional reserve banking system caused by runaway government deficit-spending.

Another fallacy has been that agriculture retards growth, leading to nationwide politically-backed attempts at land-grabbing by wily city industrialists and real estate developers. In a hyperinflation-prone economy with wild deficit-spending and runaway money-printing, cheating poor unorganised peasants of their land, when that land is an asset that is due to appreciate in value, has seemed like child’s play.

What of the Opposition? The BJP/RSS have no economists who are not quacks though opportunists were happy to say what pleased them to hear when they were in power; they also have much implicit support among organised business lobbies and the anti-Muslim senior bureaucracy. The official Communists have been appeased or bought, sometimes so cheaply as with a few airline tickets here and there. The nonsensical “Rural Employment Guarantee” is descending into the wasteland of corruption it was always going to be. The “Domestic Violence Act” as expected has started to destroy India’s families the way Western families have been destroyed. The Arjun-DMK OBC quota corrodes higher education further from its already dismal state. All these were schemes that Congress and Communist cabals created or wholeheartedly backed, and which the BJP were too scared or ignorant to resist.

And then came Singur and Nandigram ~ where the sheer greed driving the alliance between the Sonia-Manmohan-Pranab Congress and the CPI-M mask that is Buddhadeb, came to be exposed by a handful of brave women like Mamata and Medha.

A Fiscal U-Turn is Needed For India to Go in The Right Economic Direction

Rajiv Gandhi had a sense of noblesse oblige out of remembrance of his father and maternal grandfather. After his assassination, the comprador business press credited Narasimha Rao and Manmohan Singh with having originated the 1991 economic reform. In May 2002, however, the Congress Party itself passed a resolution proposed by Digvijay Singh explicitly stating Rajiv and not either of them was to be so credited. The resolution was intended to flatter Sonia Gandhi but there was truth in it too. Rajiv, a pilot who knew no political economy, was a quick learner with intelligence to know a good idea when he saw one and enough grace to acknowledge it.

Rule of Law

The first time Dr Manmohan Singh’s name arose in contemporary post-Indira politics was on 22 March 1991 when M K Rasgotra challenged the present author to answer how Dr Singh would respond to proposals being drafted for a planned economic liberalisation that had been authorised by Rajiv, as Congress President and Opposition Leader, since September 1990. It was replied that Dr Singh’s response was unknown and he had been heading the “South-South Commission” for Tanzania’s Julius Nyerere, while what needed to be done urgently was make a clear forceful statement to restore India’s credit-worthiness and the confidence of international markets, showing that the Congress at least knew its economics and was planning to take bold new steps in the direction of progress.

There is no evidence Dr Singh or his acolytes were committed to any economic liberalism prior to 1991 as that term is understood worldwide, and scant evidence they have originated liberal economic ideas for India afterwards. Precisely because they represented the decrepit old intellectual order of statist ”Ma-Bap Sarkari” policy-making, they were not asked in the mid-1980s to be part of a “perestroika-for-India” project done at a foreign university ~ the results of which were received, thanks to Siddhartha Shankar Ray, by Rajiv Gandhi in hand at 10 Janpath on 18 September 1990 and specifically sparked the change in the direction of his economic thinking.

India is a large, populous country with hundreds of millions of materially poor citizens, a weak tax-base, a vast internal and external public debt (i.e. debt owed by the Government to domestic and foreign creditors), massive annual fiscal deficits, an inconvertible currency, and runaway printing of paper-money. It is unsurprising Pakistan’s economy is similar, since it is born of the same land and people. Certainly there have been real political problems between India and Pakistan since the chaotic demobilisation and disintegration of the old British Indian Army caused the subcontinent to plunge into war-like or “cold peace” conditions for six decades beginning with a bloody Partition and civil war in J&K. High military expenditures have been necessitated due to mutual and foreign tensions, but this cannot be a permanent state if India and Pakistan wish for genuine mass economic well-being.

Even with the continuing mutual antagonism, there is vast scope for a critical review of Indian military expenditures towards greatly improving the “teeth-to-tail” ratio of its fighting forces. The abuse of public property and privilege by senior echelons of the armed forces (some of whom have been keen most of all to export their children preferably to America) is also no great secret.

On the domestic front, Rajiv was entirely convinced when the suggestion was made to him in September 1990 that an enormous infusion of public resources was needed into the judicial system for promotion and improvement of the Rule of Law in the country, a pre-requisite almost for a new market orientation. Capitalism without the Rule of Law can quickly degenerate into an illiberal hell of cronyism and anarchy which is what has tended to happen since 1991.

The Madhava Menon Committee on criminal justice policy in July proposed a Hong Kong model of “a single high-tech integrated Criminal Justice complex in every district headquarters which may be a multi-storied structure, devoting the ground floor for the police station including a video-installed interrogation room; the first floor for the police-lockups/sub-jail and the Magistrate’s Court; the second floor for the prosecutor’s office, witness rooms, crime laboratories and legal aid services; the third floor for the Sessions Court and the fourth for the administrative offices etc…. (Government of India) should take steps to evolve such an efficient model… and not only recommend it to the States but subsidize its construction…” The question arises: Why is this being proposed for the first time in 2007 after sixty years of Independence? Why was it not something designed and implemented starting in the 1950s?

The resources put since Independence to the proper working of our judiciary from the Supreme Court and High Courts downwards have been abysmal, while the state of prisons, borstals, mental asylums and other institutions of involuntary detention is nothing short of pathetic. Only police forces, like the military, paramilitary and bureaucracies, have bloated in size.

Neither Sonia-Manmohan nor the BJP or Communists have thought promotion of the Rule of Law in India to be worth much serious thought ~ certainly less important than attending bogus international conclaves and summits to sign expensive deals for arms, aircraft, reactors etc. Yet Rajiv Gandhi, at a 10 Janpath meeting on 23 March 1991 when he received the liberalisation proposals he had authorized, explicitly avowed the importance of greater resources towards the Judiciary. Dr Singh and his acolytes were not in that loop, indeed they precisely represented the bureaucratic ancien regime intended to be changed, and hence have seemed quite uncomprehending of the roots of the intended reforms ever since 1991.

Similarly, Rajiv comprehended when it was said to him that the primary fiscal problem faced by India is the vast and uncontrolled public debt, interest payments on which suck dry all public budgets leaving no room for provision of public goods.

Government accounts

Government has been routinely “rolling over” its domestic debt in the asset-portfolios of the nationalised banks while displaying and highlighting only its new additional borrowing in a year as the “Fiscal Deficit”. More than two dozen States have been doing the same and their liabilities ultimately accrue to the Union too. The stock of public debt in India is Rs 30 trillion (Rs 30 lakh crore) at least, and portends a hyperinflation in the future.

There has been no serious recognition of this since it is political and bureaucratic actions that have been causing the problem. Proper recognition would entail systematically cleaning up the budgets and accounts of every single governmental entity in the country: the Union, every State, every district and municipality, every publicly funded entity or organisation, and at the same time improving public decision-making capacity so that once budgets and accounts recover from grave sickness over decades, functioning institutions exist for their proper future management. All this would also stop corruption in its tracks, and release resources for valuable public goods and services like the Judiciary, School Education and Basic Health. Institutions for improved political and administrative decision-making are needed throughout the country if public preferences with respect to raising and allocating common resources are to be elicited and then translated into actual delivery of public goods and services. Our dysfunctional legislatures will have to do at least a little of what they are supposed to. When public budgets and accounts are healthy and we have functioning public goods and services, macroeconomic conditions would have been created for the paper-rupee to once more become a money as good as gold ~ a convertible world currency for all of India’s people, not merely the metropolitan special interest groups that have been controlling our governments and their agendas.

Fallacious Finance: Congress, BJP, CPI-M et al may be leading India to hyperinflation (2007)

March 5, 2007 — drsubrotoroyFallacious Finance: Congress, BJP, CPI-M et al may be leading India to hyperinflation

by

Subroto Roy

first published in The Statesman, 5 March 2007

Editorial Page Special Article

It seems the Dream Team of the PM, Finance Minister, Mr. Montek Ahluwalia and their acolytes may take India on a magical mystery tour of economic hallucinations, fantasies and perhaps nightmares. I hasten to add the BJP and CPI-M have nothing better to say, and criticism of the Government or of Mr Chidambaram’s Budget does not at all imply any sympathy for their political adversaries.

It may be best to outline a few of the main fallacies permeating the entire Governing Class in Delhi, and their media and businessman friends:

1. “India’s Savings Rate is near 32%”. This is factual nonsense. Savings is indeed normally measured by adding financial and non-financial savings. Financial savings include bank-deposits. But India is not a normal country in this. Nor is China. Both have seen massive exponential growth of bank-deposits in the last few decades. Does this mean Indians and Chinese are saving phenomenally high fractions of their incomes by assiduously putting money away into their shaky nationalized banks? Sadly, it does not. What has happened is government deficit-financing has grown explosively in both countries over decades. In a “fractional reserve” banking system (i.e. a system where your bank does not keep the money you deposited there but lends out almost all of it immediately), government expenditure causes bank-lending, and bank-lending causes bank-deposits to expand. Yes there has been massive expansion of bank-deposits in India but it is a nominal paper phenomenon and does not signify superhuman savings behaviour. Indians keep their assets mostly in metals, land, property, cattle, etc., and as cash, not as bank deposits.

2. “High economic growth in India is being caused by high savings and intelligently planned government investment”. This too is nonsense. Economic growth in India as elsewhere arises not because of what politicians and bureaucrats do in capital cities, but because of spontaneous technological progress, improved productivity and learning-by-doing on part of the general population. Technological progress is a very general notion, and applies to any and every production activity or commercial transaction that now can be accomplished more easily or using fewer inputs than before. New Delhi still believes in antiquated Soviet-era savings-investment models without technological progress, and some non-sycophant must tell our top Soviet-era bureaucrat that such growth models have been long superceded and need to be scrapped from India’s policy-making too. Can politicians and bureaucrats assist India’s progress? Indeed they can: the telecom revolution in recent years was something in which they participated. But the general presumption is against them. Progress, productivity gains and hence economic growth arise from enterprise and effort of ordinary people — mostly despite not because of an exploitative, parasitic State.

3. “Agriculture is a backward sector that has been retarding India’s recent economic growth”. This is not merely nonsense it is dangerous nonsense, because it has led to land-grabbing by India’s rulers at behest of their businessman friends in so-called “SEZ” schemes. The great farm economist Theodore W. Schultz once quoted Andre and Jean Mayer: “Few scientists think of agriculture as the chief, or the model science. Many, indeed, do not consider it a science at all. Yet it was the first science – Mother of all science; it remains the science which makes human life possible”. Centuries before Europe’s Industrial Revolution, there was an Agricultural Revolution led by monks and abbots who were the scientists of the day. Thanks partly to American help, India has witnessed a Green Revolution since the 1960s, and our agriculture has been generally a calm, mature, stable and productive industry. Our farmers are peaceful hardworking people who should be paying taxes and user-fees normally but should not be otherwise disturbed or needlessly provoked by outsiders. It is the businessmen wishing to attack our farm populations who need to look hard in the mirror – to improve their accounting, audit, corporate governance, to enforce anti-embezzlement and shareholder protection laws etc.

4. “India’s foreign exchange reserves may be used for ‘infrastructure’ financing”. Mr Ahluwalia promoted this idea and now the Budget Speech mentioned how Mr Deepak Parekh and American banks may be planning to get Indian businesses to “borrow” India’s forex reserves from the RBI so they can purchase foreign assets. It is a fallacy arising among those either innocent of all economics or who have quite forgotten the little they might have been mistaught in their youth. Forex reserves are a residual in a country’s balance of payments and are not akin to tax revenues, and thus are not available to be borrowed or spent by politicians, bureaucrats or their businessman friends — no matter how tricky and shady a way comes to be devised for doing so. If anything, the Government and RBI’s priority should have been to free the Rupee so any Indian could hold gold or forex at his/her local bank. India’s vast sterling balances after the Second World War vanished quickly within a few years, and the country plunged into decades of balance of payments crisis – that may now get repeated. The idea of “infrastructure” is in any case vague and inferior to the “public goods” Adam Smith knew to be vital. Serious economists recommend transparent cost-benefit analyses before spending any public resources on any project. E.g., analysis of airport/airline industry expansion would have found the vast bulk of domestic airline costs to be forex-denominated but revenues rupee-denominated – implying an obvious massive currency-risk to the industry and all its “infrastructure”. All the PM’s men tell us nothing of any of this.

5. “HIV-AIDS is a major Indian health problem”. Government doctors privately know the scare of an AIDS epidemic is based on false assumptions and analysis. Few if any of us have met, seen or heard of an actual incontrovertible AIDS victim in India (as opposed to someone infected by hepatitis-contaminated blood supplies). Syringe-exchange by intravenous drug users is not something widely prevalent in Indian society, while the practise that caused HIV to spread in California’s Bay Area in the 1980s is not something depicted even at Khajuraho. Numerous real diseases do afflict Indians – e.g. 11 children died from encephalitis in one UP hospital on a single day in July 2006, while thousands of children suffer from “cleft lip” deformity that can be solved surgically for 20,000 rupees, allowing the child a normal life. Without any objective survey being done of India’s real health needs, Mr Chidamabaram has promised more than Rs 9.6 Billion (Rs 960 crore) to the AIDS cottage industry.

6. “Fiscal consolidation & stabilization has been underway since 1991”. There is extremely little reason to believe this. If you or I borrow Rs. 100,000 for a year, and one year later repay the sum only to borrow the same again along with another Rs 40,000, we would be said to have today a debt of Rs. 140,000 at least. Our Government has been routinely “rolling over” its domestic debt in this manner (in the asset-portfolios of the nationalised banking system) but displaying and highlighting only its new additional borrowing in a year as the “ Fiscal Deficit” (see graph, also “Fiscal Instability”, The Sunday Statesman, 4 February 2007). More than two dozen State Governments have been doing the same though, unlike the Government of India, they have no money-creating powers and their liabilities ultimately accrue to the Union as well. The stock of public debt in India may be Rs 30 trillion (Rs 30 lakh crore) at least, and portends a hyperinflation in the future. Mr Chidambaram’s announcement of a “Debt Management Office” yet to be created is hardly going to suffice to avert macroeconomic turmoil and a possible monetary collapse. The Congress, BJP, CPI-M and all their friends shall be responsible.

Of related interest: Mistaken Macroeconomics,

“The Indian Revolution”, “Against Quackery”, “The Dream Team: A Critique”, “India’s Macroeconomics”, “Indian Inflation”

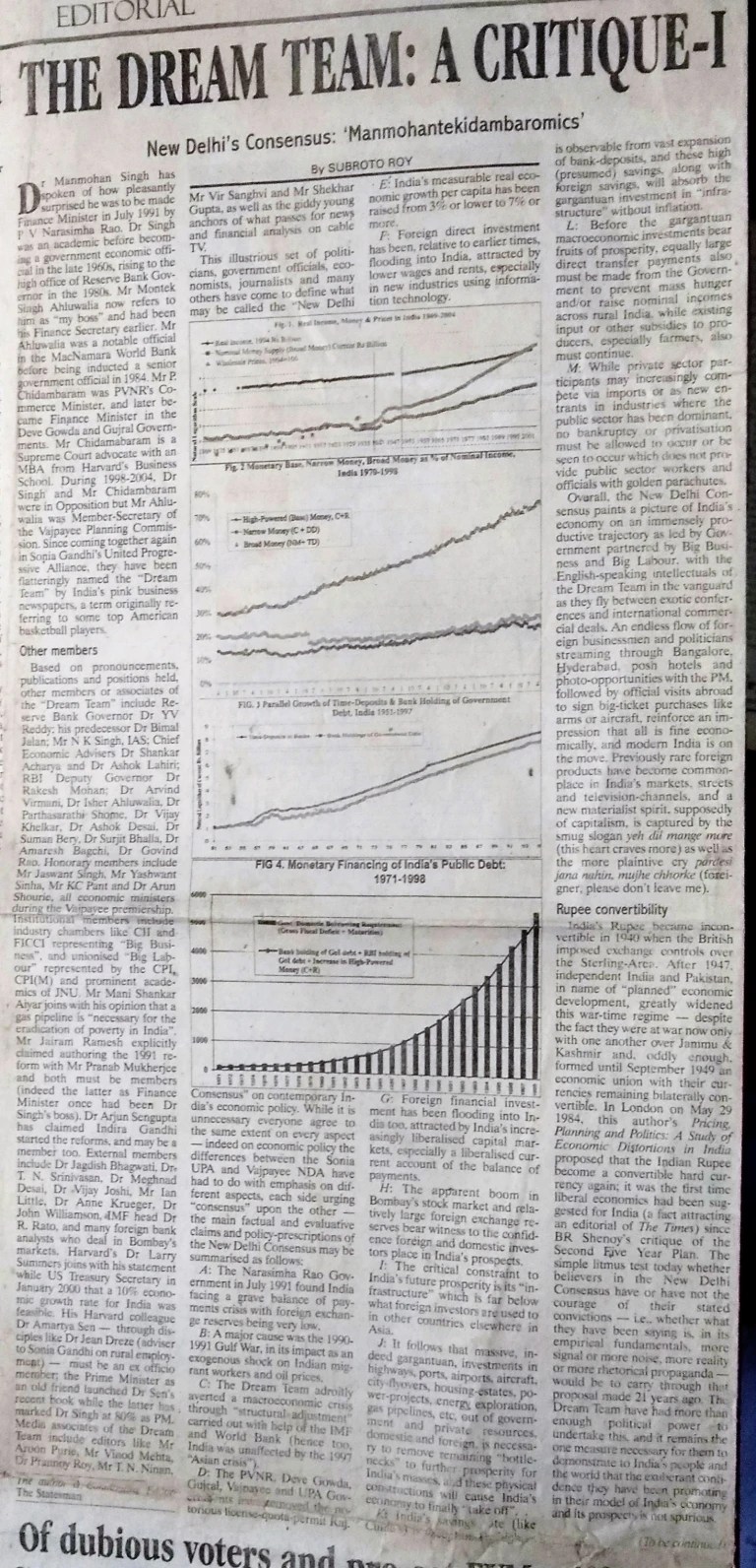

The Dream Team: A Critique (2006)

January 8, 2006 — drsubrotoroyThe Dream Team: A Critique

by Subroto Roy

First published in The Statesman and The Sunday Statesman, Editorial Page Special Article, January 6,7,8, 2006

(Author’s Note: Within a few weeks of this article appearing, the Dream Team’s leaders appointed the so-called Tarapore 2 committee to look into convertibility — which ended up recommending what I have since called the “false convertibility” the RBI is presently engaged in. This article may be most profitably read along with other work republished here: “Rajiv Gandhi and the Origins of India’s 1991 Economic Reform”, “Three Memoranda to Rajiv Gandhi”, “”Indian Money & Banking”, “Indian Money & Credit” , “India’s Macroeconomics”, “Fiscal Instability”, “Fallacious Finance”, “India’s Trade and Payments”, “Our Policy Process”, “Against Quackery”, “Indian Inflation”, etc)