The Reserve Bank of India @RBI like any central bank is charged with managing a country’s “foreign exchange reserves”; fx reserves are *not* what they sound like: they are a residual in a country’s balance of payments and are *not* akin to tax revenues, hence are *not* open to be purloined by a Government to spend.

India’s fx reserves were sought to be “borrowed” by the Manmohan Chidambaram Montek regime back then, and I harshly objected. The same is being attempted now by Modi Jaitley Shah Gurumurthy Sitharaman.

Then it was ostensibly for “infrastructure”, now ostensibly for “small business” subsidies, “poverty alleviation”, “recapitalising PSBs”; I denounced it as lobbyist-driven humbug then, and do so now too.

One of Manmohan’s acolytes has in recent days told PTI “in the past too, governments had contemplated a similar plan but dropped it as the negatives far outweighed the positives”.

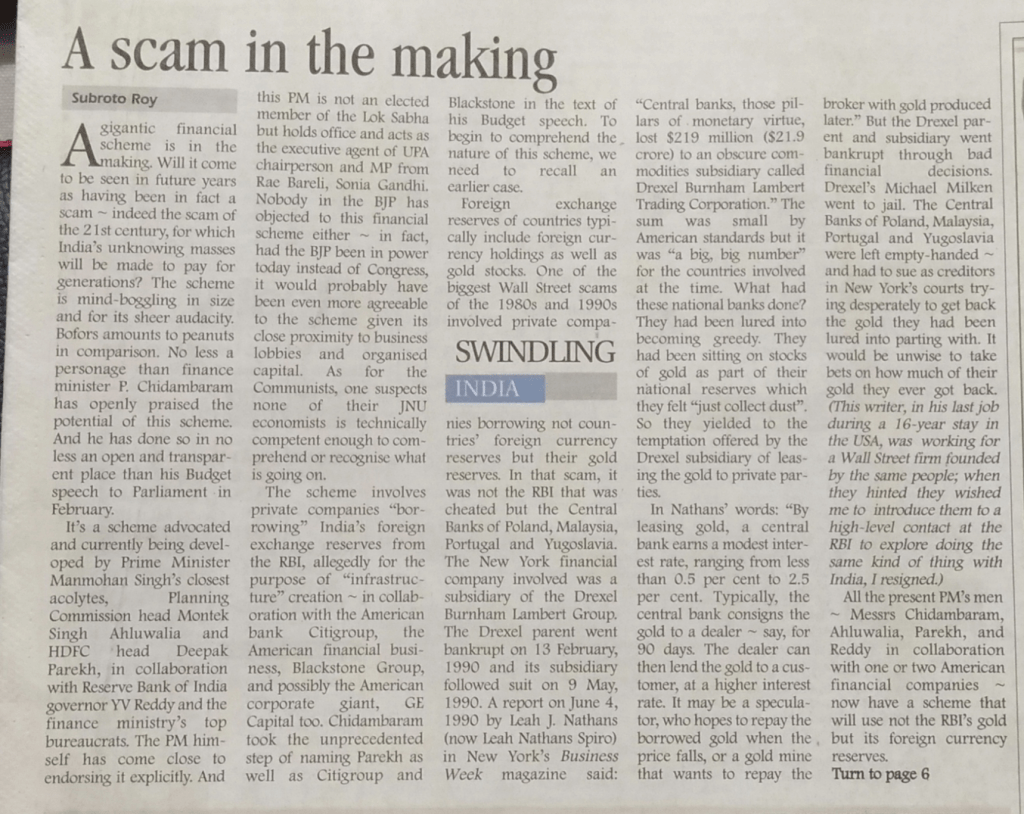

“A gigantic financial scheme is in the making. Will it come to be seen in future years as having been in fact a scam – indeed India’s scam of the 21st Century for which India’s unknowing masses will be made to pay for many generations? The scheme is mind-boggling in size as well as its sheer audacity. Bofors, Quattrochi etc amount to peanuts in comparison.

No less a personage than the Finance Minister of India, P Chidambaram, has openly praised the potential of this financial scheme. And he has done so in no less an open and transparent place than his latest Budget Speech to Parliament last February.

It is a scheme openly advocated and currently being developed by our Prime Minister Dr Manmohan Singh’s closest acolytes, Planning Commission head Mr Montek Singh Ahluwalia and HDFC head Mr Deepak Parekh, in collaboration with Reserve Bank Governor Dr YV Reddy and the Finance Ministry’s top bureaucrats. The PM himself has come close to endorsing it explicitly. And this PM is not an elected member of the Lok Sabha but holds office and acts as the executive agent of the UPA Chairperson and Lok Sabha Member from Rae Bareilly, Sonia Gandhi.

I hasten to add nobody in the BJP has objected to this financial scheme — in fact had the BJP been in power today instead of Congress, they would have been likely even more agreeable to the scheme given their close proximity to business lobbies and organized capital. As for the Communists, none of their JNU economics professors is technically competent enough to comprehend or recognize what is going on.

The scheme involves private companies “borrowing” India’s foreign exchange reserves from the Reserve Bank of India, allegedly for purpose of “infrastructure” creation — in collaboration with the American bank Citigroup, the American financial business, Blackstone Group, and possibly the American giant, GE Capital too. Mr Chidambaram took the unprecedented step of naming Mr Deepak Parekh as well as Citigroup and Blackstone in the text of his Budget Speech.

To begin to comprehend the nature of this scheme, we need to recall an earlier case.

Foreign exchange reserves of countries typically include foreign currency holdings as well as gold stocks. One of the biggest Wall Street scams of the 1980s-1990s involved private companies borrowing not countries’ foreign currency reserves but their gold reserves.

In that scam, it was not the Reserve Bank of India that was cheated but the Central Banks of Poland, Malaysia, Portugal and Yugoslavia. The New York financial company involved was a subsidiary of the Drexel Burnham Lambert Group. The Drexel parent went bankrupt on February 13 1990 and its subsidiary followed on May 9 1990.

A report on June 4 1990 by Leah J. Nathans (now Leah Nathans Spiro) in New York’s highly respected Business Week magazine said: “Central banks, those pillars of monetary virtue, lost $219 million ($21.9 crore) to an obscure commodities subsidiary called Drexel Burnham Lambert Trading Corporation”. The sum was small by American standards but it was “a big, big number” for the countries involved at the time.

What had these national central banks done? They had been lured into becoming greedy. They had been sitting on stocks of gold as part of their national reserves which they felt “just collect dust”. So they yielded to the temptation offered by the Drexel subsidiary of leasing the gold to private parties.

In Ms. Nathans’ words, “By leasing gold, a central bank earns a modest interest rate, ranging from less than 0.5% to 2.5%. Typically, the central bank consigns the gold to a dealer – say, for 90 days. The dealer can then lend the gold to a customer, at a higher interest rate. It may be a speculator, who hopes to repay the borrowed gold when the price falls, or a gold mine that wants to repay the broker with gold produced later.”

But the Drexel parent and subsidiary went bankrupt through bad financial decisions. Drexel’s Michael Milken went to jail. The Central Banks of Poland, Malaysia, Portugal and Yugoslavia were left empty-handed – and had to sue as creditors in New York’s courts trying desperately to get back the gold they had been lured into parting with. It would be unwise to take bets on how much of their gold they ever got back.

All the present PM’s men — Messrs Chidambaram, Ahluwalia, Parekh, Reddy et al in collaboration with one or two American financial companies – now have a scheme that will use not the RBI’s gold but its foreign currency reserves.

Mr Ahluwalia and Mr Parekh have made the outlandish claim that “India needs US$320 billion” (US 32,000 crore) by way of “investment for physical infrastructure” during the so-called “Eleventh Five-Year Plan”. (How many so-called “Five Year Plans” is India going to have incidentally? We had our “First Plan” when Manmohan Singh was a student at Punjab University. Stalin, who invented the “Five Year Plan”, died during that time, and even his old USSR has ceased to exist, let alone its “Five Year Plans”.)

That vast amount of “investment for physical infrastructure” is what Mr Ahluwalia says he knows India needs for his purported “9% growth rate” to be achieved. Where are the macroeconomic models and time-series data sets from him or his friends to back such assertions? There are none. None of the PM’s men, no one in the Finance Ministry or RBI or Planning Commission, nor any of their JNU economics professor friends or anyone else in Delhi, Mumbai, Kolkata etc have any such models or data with which to back such assertions. Nor do the World Bank etc. It is all sheer humbug – all a lie. It is part of the mendacity and self-delusion that our capital city has been floating upon.

In any event, the RBI reportedly has “opposed the idea of deploying forex reserves for infrastructure development on the grounds that it will create monetary expansion”. But Mr Chidambaram’s Finance Ministry owns the RBI, and the Ministry has said “the RBI’s concerns had been taken care of, as the investments would be deployed only through a structured mechanism”. (Business Standard 23 March 2007, p. 3)

What is a “structured mechanism”? Mr Chidambaram, mentioning Citigroup and Blackstone Group specifically, said in his Budget Speech that Mr Deepak Parekh has “suggested the establishment of two wholly-owned overseas subsidiaries of India Infrastructure Finance Company Ltd with the following objectives: (i) to borrow funds from the RBI and lend to Indian companies implementing infrastructure projects in India, or to co-finance their External Commercial Borrowings for such projects, solely for capital expenditure outside India; and (ii) to borrow funds from the RBI, invest such funds in highly rated collateral securities, and provide ‘credit wrap’ insurance to infrastructure projects in India for raising resources in international markets. The loans by RBI to these two subsidiary companies will be guaranteed by the Government of India and the RBI will be assured of a return higher than the average rate of return on its incremental investment.”

You do not understand? Well, no one is supposed to. The most exquisite thievery occurs after all not in darkness but in broad daylight with everyone watching but no one able to see or comprehend anything. So let us return to elementary first principles.

What are foreign exchange reserves and why do countries hold them? It is quite simply answered. Consider the USA and Canada, each with its own dollar. Canadians want to purchase American goods and services, give gifts and make loans to American residents, and make investments in the USA. Americans want to do the same in Canada. Each has to use the domestic money of the other when it does so. If an American wishes to lend money to a Canadian or to purchase something from him, he receives Canadian dollar notes from the Canadian Government to make his Canadian transactions, handing over his American dollar notes instead. The American dollar notes he hands over become part of Canada’s foreign exchange reserves, held by its Central Bank. Roughly speaking, a country’s foreign exchange reserves are the residual foreign currency assets its central bank holds after all these transactions are carried out on both sides of the border.

In the US-Canada case, neither Government prevents its citizens from exchanging domestic money for foreign money. In India, our rupee has been inconvertible since about 1940. The average Indian cannot freely exchange his/her rupee-denominated assets for foreign exchange denominated ones even if he/she wished to. There has been some import-liberalisation in recent years but only someone with the political access of Mr Tata or Mr Birla can purchase foreign assets and foreign companies using their Indian money – because the rupee is inconvertible, any bad financial decisions they make in using their foreign assets will be implicitly paid for by the Indian public.

Now a country’s central bank, such as our Reserve Bank, is the custodian of its foreign exchange reserves. India’s reserves are supposed to have reached $195.96 Billion ($19,596 Crore) as of March 16 2007. Keep in mind we do not know why they have risen: they can rise merely because foreigners (including NRIs) have lent us more of their money, not because foreigners have bought more of our goods and services. In fact Business Standard yesterday 31 March 2007 said on its front page “external commercial borrowing” was “a major source of accretion” of India’s reserves.

Also keep in mind that the Reserve Bank has the duty to manage these foreign-denominated assets against which it has already issued Indian rupees. It might receive a small conservative income from the cash-management aspect of this but it may not risk them or place them in any jeopardy!

Yet the whole idea behind the Chidambaram-Ahluwalia-Parekh-Reddy scheme under discussion by the Sonia-Manmohan Government is that the RBI will “lend” some of the billions of Americans dollars in its custody to overseas subsidiaries of Indian companies – say, for example, to the Tatas who have now bought foreign “capital assets” of some US$ 12 Billion ($1200 Crore) from Corus without having anything near that kind of foreign income.

Such favoured Indian companies might then use these “borrowed” funds as collateral for other borrowings. In exchange, they will go about undertaking purported “infrastructure” projects in India. So much for the “structured mechanisms” being touted by Messrs Chidambaram, Ahluwalia, Parekh et al.

Before India’s public understands it, the schemers will shout (as they have done with the SEZ Act) that Parliament has passed it. The BJP will applaud with envy. The Communists might uncomprehendingly complain a little, and then be bought off with a sop or two that they do understand, like a little pro-China rhetoric or being let off lightly on Nandigram.

Now international institutions like the International Monetary Fund and the Bank of International Settlements officially exist to advise central banks to stay along the straight and narrow and to avoid all such mischief. Here is what the IMF explicitly warned about such schemes in its Guidelines for Foreign Exchange Reserve Management dated September 20 2001:

“Liquidity risk. The pledging of reserves as collateral with foreign financial institutions as support for loans to either domestic entities, or foreign subsidiaries of the reserve management entity, has rendered reserves illiquid until the loans have been repaid. Liquidity risks have also arisen from the direct lending of reserves to such institutions when shocks to the domestic economy led to the borrowers’ inability to repay their liabilities, and impairment of the liquidity of the reserve assets.

Credit risk. Losses have arisen from the investment of reserves in high-yielding assets that were made without due regard to the credit risk associated with the issuer of the asset. Lending of reserves to domestic banks, and overseas subsidiaries of reserve management entities, has also exposed reserve management entities to credit risk.”

Dostoevsky believed man could have evil intent. Socrates was more generous and said man does not do wrong knowingly. It is not impossible our Indian schemers have innocent intent and do not even realize how close they are to becoming scamsters, or are already in the grip of scamsters. But at least we are now forewarned: India faces a clear risk of being swindled of its foreign exchange reserves. Prevention is better than cure.”

I may add my father, back in 1973 in Paris, had predicted to me that you would become Prime Minister of India one day, and he, now in his 90s, is joined by myself in sending our warm congratulations at the start of your second term in that high office.

The controversy though that you and I had entered that Paris day in 1973 about scientific economics as applied to India, must be renewed afresh!

This is because of your categorical statement on June 9 2009 to the new 15th Lok Sabha:

“I am convinced, since our savings rate is as high as 35%, given the collective will, if all of us work together, we can achieve a growth-rate of 8%-9%, even if the world economy does not do well.” (Statement of Dr Manmohan Singh to the Lok Sabha, June 9 2009)

I am afraid there may be multiple reasons why such a statement is gravely and incorrigibly in error within scientific economics. From your high office as Prime Minister in a second term, faced perhaps with no significant opposition from either within or without your party, it is possible the effects of such an error may spell macroeconomic catastrophe for India.

As it happens, the British Labour Party politician Dr Meghnad Desai made an analogous statement to yours about India when he claimed in 2006 that China

“now has 10.4% growth on a 44 % savings rate… ”

Indeed the idea that China and India have had extremely high economic growth-rates based on purportedly astronomical savings rates has become a commonplace in recent years, repeated endlessly in international and domestic policy circles though perhaps without adequate basis.

Germany & Japan

What, at the outset, is supposed to be measured when we speak of “growth”? Indian businessmen and their media friends seem to think “growth” refers to something like nominal earnings before tax for the organised corporate sector, or any unspecified number that can be sold to visiting foreigners to induce them to park their funds in India: “You will get a 10% return if you invest in India” to which the visitor says “Oh that must mean India has 10% growth going on”. Of such nonsense are expensive international conferences in Davos and Delhi often made.

You will doubtless agree the economist at least must define economic growth properly and with care — what is referred to must be annual growth of per capita inflation-adjusted Gross Domestic Product. (Per capita National Income or Net National Product would be even better if available).

West Germany and Japan had the highest annual per capita real GDP growth-rates in the world economy starting from devastated post-World War II initial conditions. What were their measured rates?

West Germany: 6.6% in 1950-1960, falling to 3.5% by 1960-1970 falling to 2.4% by 1970-1978.

Japan: 6.8 % in 1952-1960 rising to 9.4% in 1960-1970 falling to 3.8 % in 1970-1978.

Thus in recent decades only Japan measured a spike in the 1960s of more than 9% annual growth of real per capita GDP. Now India and China are said to be achieving 8%-10 % and more year after year routinely!

Perhaps we are observing an incredible phenomenon of world economic history. Or perhaps it is just something incredible, something false and misleading, like a mirage in the desert.

You may agree that processes of measurement of real income in India both at federal and provincial levels, still remain well short of the world standards described by the UN’s System of National Accounts 1993. The actuality of our real GDP growth may be better than what is being measured or it may be worse than what is being measured – from the point of view of public decision-making we at present simply do not know which it is, and to overly rely on such numbers in national decisions may be unwise. In any event, India’s population is growing at near 2% so even if your Government’s measured number of 8% or 9% is taken at face-value, we have to subtract 2% population growth to get per capita figures.

Growth of the aam admi’s consumption-basket

The late Professor Milton Friedman had been an invited adviser in 1955 to the Government of India during the Second Five Year Plan’s formulation. The Government of India suppressed what he had to say and I had to publish it 34 years later in May 1989 during the 1986-1992 perestroika-for-India project that I led at the University of Hawaii in the United States. His November 1955 Memorandum to the Government of India is a chapter in the book Foundations of India’s Political Economy: Towards an Agenda for the 1990s that I and WE James created.

At the 1989 project-conference itself, Professor Friedman made the following astute observation about all GNP, GDP etc growth-numbers that speaks for itself:

“I don’t believe the term GNP ought to be used unless it is supplemented by a different statistic: the rate of growth of the average consumption basket consumed by the ordinary individual in the country. I think GNP rates of growth can give very misleading information. For example, you have rapid rates of growth of GNP in the Soviet Union with a declining standard of life for the people. Because GNP includes monuments and includes also other things. I’m not saying that that is the case with India; I’m just saying I would like to see the two figures together.”

You may perhaps agree upon reflection that not only may our national income growth measurements be less robust than we want, it may be better to be measuring something else instead, or as well, as a measure of the economic welfare of India’s people, namely, “the rate of growth of the average consumption basket consumed by the ordinary individual in the country”, i.e., the rate of growth of the average consumption basket consumed by the aam admi.

It would be excellent indeed if you were to instruct your Government’s economists and other spokesmen to do so this as it may be something more reliable as an indicator of our economic realities than all the waffle generated by crude aggregate growth-rates.

Logic of your model

Thirdly, the logic needs to be spelled out of the economic model that underlies such statements as yours or Meghnad Desai’s that seek to operationally relate savings rates to aggregate growth rates in India or China. This seems not to have been done publicly in living memory by the Planning Commission or other Government economists. I have had to refer, therefore, to pages 251-253 of my own Cambridge doctoral thesis under Professor Frank Hahn thirty years ago, titled “On liberty and economic growth: preface to a philosophy for India”, where the logic of such models as yours was spelled out briefly as follows:

Let

Kt be capital stock

Yt be national output

It be the level of real investment

St be the level of real savings

By definition

It = K t+1 – Kt

By assumption

Kt = k Yt 0 < k < 1

St = sYt 0 < s <1

In equilibrium ex ante investment equals ex ante savings

It = St

Hence in equilibrium

sYt = K t+1 – Kt

Or

s/k = g

where g is defined to be the rate of growth (Y t+1-Yt)/Yt .

The left hand side then defines the “warranted rate of growth” which must maintain the famous “knife-edge” with the right hand side “natural rate of growth”.

Your June 9 2009 Lok Sabha statement that a 35% rate of savings in India may lead to an 8%-9% rate of economic growth in India, or Meghnad Desai’s statement that a 44% rate of savings in China led to a 10.4% growth there, can only be made meaningful in the context of a logical economic model like the one I have given above.

[In the open-economy version of the model, let Mt be imports, Et be exports, Ft net capital inflows.

Assume

Mt = aIt + bYt 0 < a, b < 1

Et = E for all t

Balance of payments is

Bt = Mt – Et – Ft

In equilibrium It = St + Bt

Or

Ft = (s+b) Yt – (1-a) It – E is a kind of “warranted” level of net capital inflow.]

You may perhaps agree upon reflection that building the entire macroeconomic policy of the Government of India merely upon a piece of economic logic as simplistic as the

s/k = g

equation above, may spell an unacceptable risk to the future economic well-being of our vast population. An alternative procedural direction for macroeconomic policy, with more obviously positive and profound consequences, may have been that which I sought to persuade Rajiv Gandhi about with some success in 1990-1991. Namely, to systematically seek to improve towards normalcy the budgets, financial positions and decision-making capacities of the Union and all state and local governments as well as all public institutions, organisations, entities, and projects in general, with the aim of making our domestic money a genuine hard currency of the world again after seven decades, so that any ordinary resident of India may hold and trade precious metals and foreign exchange at his/her local bank just like all those glamorous privileged NRIs have been permitted to do. Such an alternative path has been described in “The Indian Revolution”, “Against Quackery”, “The Dream Team: A Critique”, “India’s Macroeconomics”, “Indian Inflation”, etc.

Gross exaggeration of real savings rate by misreading deposit multiplication

Specifically, I am afraid you may have been misled into thinking India’s real savings rate, s, is as high as 35% just as Meghnad Desai may have misled himself into thinking China’s real savings rate is as high as 44%.

Neither of you may have wanted to make such a claim if you had referred to the fact that over the last 25 years, the average savings rate across all OECD countries has been less than 10%. Economic theory always finds claims of discontinuous behaviour to be questionable. If the average OECD citizen has been trying to save 10% of disposable income at best, it appears prima facie odd that India’s PM claims a savings rate as high as 35% for India or a British politician has claimed a savings rate as high as 44% for China. Something may be wrong in the measurement of the allegedly astronomical savings rates of India and China. The late Professor Nicholas Kaldor himself, after all, suggested it was rich people who saved and poor people who did not for the simple reason the former had something left over to save which the latter did not!

And indeed something is wrong in the measurements. What has happened, I believe, is that there has been a misreading of the vast nominal expansion of bank deposits via deposit-multiplication in the Indian banking system, an expansion that has been caused by explosive deficit finance over the last four or five decades. That vast nominal expansion of bank-deposits has been misread as indicating growth of real savings behaviour instead. I have written and spoken about and shown this quite extensively in the last half dozen years since I first discovered it in the case of India. E.g., in a lecture titled “Can India become an economic superpower or will there be a monetary meltdown?” at Cardiff University’s Institute of Applied Macroeconomics and at London’s Institute of Economic Affairs in April 2005, as well as in May 2005 at a monetary economics seminar invited at the RBI by Dr Narendra Jadav. The same may be true of China though I have looked at it much less.

How I described this phenomenon in a 2007 article in The Statesman is this:

“Savings is indeed normally measured by adding financial and non-financial savings. Financial savings include bank-deposits. But India is not a normal country in this. Nor is China. Both have seen massive exponential growth of bank-deposits in the last few decades. Does this mean Indians and Chinese are saving phenomenally high fractions of their incomes by assiduously putting money away into their shaky nationalized banks? Sadly, it does not. What has happened is government deficit-financing has grown explosively in both countries over decades. In a “fractional reserve” banking system (i.e. a system where your bank does not keep the money you deposited there but lends out almost all of it immediately), government expenditure causes bank-lending, and bank-lending causes bank-deposits to expand. Yes there has been massive expansion of bank-deposits in India but it is a nominal paper phenomenon and does not signify superhuman savings behaviour. Indians keep their assets mostly in metals, land, property, cattle, etc., and as cash, not as bank deposits.”

An article of mine in 2008 in Business Standard put it like this:

“India has followed in peacetime over six decades what the US and Britain followed during war. Our vast growth of bank deposits in recent decades has been mostly a paper (or nominal) phenomenon caused by unlimited deficit finance in a fractional reserve banking system. Policy makers have widely misinterpreted it as indicating a real phenomenon of incredibly high savings behaviour. In an inflationary environment, people save their wealth less as paper deposits than as real assets like land, cattle, buildings, machinery, food stocks, jewellery etc.”

If you asked me “What then is India’s real savings rate?” I have little answer to give except to say I know what it is not – it is not what the Government of India says it is. It is certainly unlikely to be anywhere near the 35% you stated it to be in your June 9 2009 Lok Sabha statement. If the OECD’s real savings rate has been something like 10% out of disposable income, I might accept India’s is, say, 15% at a maximum when properly measured – far from the 35% being claimed. What I believe may have been mismeasured by you and Meghnad Desai and many others as indicating high real savings is actually the nominal or paper expansion of bank-deposits in a fractional reserve banking system induced by runaway government deficit-spending in both India and China over the last several decades.

Technological progress and the mainsprings of real economic growth

So much for the g and s variables in the s/k = g equation in your economic model. But the assumed constant k is a big problem too!

During the 1989 perestroika-for-India project-conference, Professor Friedman referred to his 1955 experience in India and said this about the assumption of a constant k:

“I think there was an enormously important point… That was the almost universal acceptance at that time of the view that there was a sort of technologically fixed capital output ratio. That if you wanted to develop, you just had to figure out how much capital you needed, used as a statistical technological capital output ratio, and by God the next day you could immediately tell what output you were going to achieve. That was a large part of the motivation behind some of the measures that were taken then.”

The crucial problem of the sort of growth-model from which your formulation relating savings to growth arises is that, with a constant k, you have necessarily neglected the real source of economic growth, which is technological progress!

I said in the 2007 article referred to above:

“Economic growth in India as elsewhere arises not because of what politicians and bureaucrats do in capital cities, but because of spontaneous technological progress, improved productivity and learning-by-doing on part of the general population. Technological progress is a very general notion, and applies to any and every production activity or commercial transaction that now can be accomplished more easily or using fewer inputs than before.”

In “Growth and Government Delusion” published in The Statesman last year, I described the growth process more fully like this:

“The mainsprings of real growth in the wealth of the individual, and so of the nation, are greater practical learning, increases in capital resources and improvements in technology. Deeper skills and improved dexterity cause output produced with fewer inputs than before, i.e. greater productivity. Adam Smith said there is “invention of a great number of machines which facilitate and abridge labour, and enable one man to do the work of many”. Consider a real life example. A fresh engineering graduate knows dynamometers are needed in testing and performance-certification of diesel engines. He strips open a meter, finds out how it works, asks engine manufacturers what design improvements they want to see, whether they will buy from him if he can make the improvement. He finds out prices and properties of machine tools needed and wages paid currently to skilled labour, calculates expected revenues and costs, and finally tries to persuade a bank of his production plans, promising to repay loans from his returns. Overcoming restrictions of religion or caste, the secular agent is spurred by expectation of future gains to approach various others with offers of contract, and so organize their efforts into one. If all his offers ~ to creditors, labour, suppliers ~ are accepted he is, for the moment, in business. He may not be for long ~ but if he succeeds his actions will have caused an improvement in design of dynamometers and a reduction in the cost of diesel engines, as well as an increase in the economy’s produced means of production (its capital stock) and in the value of contracts made. His creditors are more confident of his ability to repay, his buyers of his product quality, he himself knows more of his workers’ skills, etc. If these people enter a second and then a third and fourth set of contracts, the increase in mutual trust in coming to agreement will quickly decline in relation to the increased output of capital goods. The first source of increasing returns to scale in production, and hence the mainspring of real economic growth, arises from the successful completion of exchange. Transforming inputs into outputs necessarily takes time, and it is for that time the innovator or entrepreneur or “capitalist” or “adventurer” must persuade his creditors to trust him, whether bankers who have lent him capital or workers who have lent him labour. The essence of the enterprise (or “firm”) he tries to get underway consists of no more than the set of contracts he has entered into with the various others, his position being unique because he is the only one to know who all the others happen to be at the same time. In terms introduced by Professor Frank Hahn, the entrepreneur transforms himself from being “anonymous” to being “named” in the eyes of others, while also finding out qualities attaching to the names of those encountered in commerce. Profits earned are partly a measure of the entrepreneur’s success in this simultaneous process of discovery and advertisement. Another potential entrepreneur, fresh from engineering college, may soon pursue the pioneer’s success and start displacing his product in the market ~ eventually chasers become pioneers and then get chased themselves, and a process of dynamic competition would be underway. As it unfolds, anonymous and obscure graduates from engineering colleges become by dint of their efforts and a little luck, named and reputable firms and perhaps founders of industrial families. Multiply this simple story many times, with a few million different entrepreneurs and hundreds of thousands of different goods and services, and we shall be witnessing India’s actual Industrial Revolution, not the fake promise of it from self-seeking politicians and bureaucrats.”

Technological progress in a myriad of ways and discovery of new resources are important factors contributing to India’s growth today. But while India’s “real” economy does well, the “nominal” paper-money economy controlled by Government does not. Continuous deficit financing for half a century has led to exponential growth of public debt and broad money, and, as noted, the vast growth of nominal bank-deposits has been misinterpreted as indicating unusually high real savings behaviour when it in fact may just signal vast amounts of government debt being held by our nationalised banks. These bank assets may be liquid domestically but are illiquid internationally since our government debt is not held by domestic households as voluntary savings nor has it been a liquid asset held worldwide in foreign portfolios.

What politicians of all parties, especially your own and the BJP and CPI-M since they are the three largest, have been presiding over is exponential growth of our paper money supply, which has even reached 22% per annum. Parliament and the Government should be taking honest responsibility for this because it may certainly portend double-digit inflation (i.e., decline in the value of paper-money) perhaps as high as 14%-15% per annum, something that is certain to affect the aam admi’s economic welfare adversely.

Selling Government assets to Big Business is a bad idea in a potentially hyperinflationary economy

Respected PradhanMantriji, the record would show that I, and really I alone, 25 years ago, may have been the first among Indian economists to advocate the privatisation of the public sector. (Viz, “Silver Jubilee of Pricing, Planning and Politics: A Study of Economic Distortions in India”.) In spite of this, I have to say clearly now that in present circumstances of a potentially hyperinflationary economy created by your Government and its predecessors, I believe your Government’s present plans to sell Government assets may be an exceptionally unwise and imprudent idea. The reasoning is very simple from within monetary economics.

Government every year has produced paper rupees and bank deposits in practically unlimited amounts to pay for its practically unlimited deficit financing, and it has behaved thus over decades. Such has been the nature of the macroeconomic process that all Indian political parties have been part of, whether they are aware of it or not.

Indian Big Business has an acute sense of this long-term nominal/paper expansion of India’s economy, and acts towards converting wherever possible its own hoards of paper rupees and rupee-denominated assets into more valuable portfolios for itself of real or durable assets, most conspicuously including hard-currency denominated assets, farm-land and urban real-estate, and, now, the physical assets of the Indian public sector. Such a path of trying to transform local domestic paper assets – produced unlimitedly by Government monetary and fiscal policy and naturally destined to depreciate — into real durable assets, is a privately rational course of action to follow in an inflationary economy. It is not rocket-science to realise the long-term path of rupee-denominated assets is downwards in comparison to the hard-currencies of the world – just compare our money supply growth and inflation rates with those of the rest of the world.

The Statesman of November 16 2006 had a lead editorial titled Government’s land-fraud: Cheating peasants in a hyperinflation-prone economy which said:

“There is something fundamentally dishonourable about the way the Centre, the state of West Bengal and other state governments are treating the issue of expropriating peasants, farm-workers, petty shop-keepers etc of their small plots of land in the interests of promoters, industrialists and other businessmen. Singur may be but one example of a phenomenon being seen all over the country: Hyderabad, Karnataka, Kerala, Haryana, everywhere. So-called “Special Economic Zones” will merely exacerbate the problem many times over. India and its governments do not belong only to business and industrial lobbies, and what is good for private industrialists may or may not be good for India’s people as a whole. Economic development does not necessarily come to be defined by a few factories or high-rise housing complexes being built here or there on land that has been taken over by the Government, paying paper-money compensation to existing stakeholders, and then resold to promoters or industrialists backed by powerful political interest-groups on a promise that a few thousand new jobs will be created. One fundamental problem has to do with inadequate systems of land-description and definition, implementation and recording of property rights. An equally fundamental problem has to do with fair valuation of land owned by peasants etc. in terms of an inconvertible paper-money. Every serious economist knows that “land” is defined as that specific factor of production and real asset whose supply is fixed and does not increase in response to its price. Every serious economist also knows that paper-money is that nominal asset whose price can be made to catastrophically decline by a massive increase in its supply, i.e. by Government printing more of the paper it holds a monopoly to print. For Government to compensate people with paper-money it prints itself by valuing their land on the basis of an average of the price of the last few years, is for Government to cheat them of the fair present-value of the land. That present-value of land must be calculated in the way the present-value of any asset comes to be calculated, namely, by summing the likely discounted cash-flows of future values. And those future values should account for the likelihood of a massive future inflation causing decline in the value of paper-money in view of the fact we in India have a domestic public debt of some Rs. 30 trillion (Rs. 30 lakh crore) and counting, and money supply growth rates averaging 16-17% per annum. In fact, a responsible Government would, given the inconvertible nature of the rupee, have used foreign exchange or gold as the unit of account in calculating future-values of the land. India’s peasants are probably being cheated by their Government of real assets whose value is expected to rise, receiving nominal paper assets in compensation whose value is expected to fall.”

Shortly afterwards the Hon’ble MP for Kolkata Dakshin, Km Mamata Banerjee, started her protest fast, riveting the nation’s attention in the winter of 2006-2007. What goes for government buying land on behalf of its businessman friends also goes, mutatis mutandis, for the public sector’s real assets being bought up by the private sector using domestic paper money in a potentially hyperinflationary economy. If your new Government wishes to see real assets of the public sector being sold for paper money, let it seek to value these assets not in inconvertible rupees that Government itself has been producing in unlimited quantities but perhaps in forex or gold-units instead!

In the 2004-2005 volume Margaret Thatcher’s Revolution: How it Happened and What it Meant, edited by myself and Professor John Clarke, there is a chapter by Professor Patrick Minford on Margaret Thatcher’s fiscal and monetary policy (macroeconomics) that was placed ahead of the chapter by Professor Martin Ricketts on Margaret Thatcher’s privatisation (microeconomics). India’s fiscal and monetary or macroeconomic problems are far worse today than Britain’s were when Margaret Thatcher came to power. We need to get our macroeconomic problems sorted before we attempt the microeconomic privatisation of public assets.

It is wonderful that your young party colleague, the Hon’ble MP from Amethi, Shri Rahul Gandhi, has declined to join the present Government and instead wishes to reflect further on the “common man” and “common woman” about whom I had described his late father talking to me on September 18 1990. Certainly the aam admi is not someone to be found among India’s lobbyists of organised Big Business or organised Big Labour who have tended to control government agendas from the big cities.

Now coming to current times, I remain appalled by the large errors and extremely low quality of economic thought that has emerged from RBI and Gov’t economists and pretenders in Delhi and Mumbai in recent years.

As a general rule, I do not critique people younger than myself. Raghuram Rajan (who I think reviewed my 1984 work when he was still doing electrical engineering at IIT Delhi) fell in that category, and I was gentle and encouraging when he first became RBI Governor. Even later when his waffle became especially tedious I merely poked fun at it. Then in December 2018 he gave a much hyped NDTV interview where he made cardinal errors one does not expect from a former RBI Governor or IMF Chief Economist! He had to be taken to task for revealing essentially an ignorance of what foreign exchange reserves in fact are by the IMF’s own definition and acknowledged as such worldwide!

it is utterly appalling that a former Chief Economist of the IMF, also a former @RBI head, seems unfamiliar w the IMF’s own standard definitions of the balance of payments & forex reserves… #RajanToNDTV

how to see a Central Bank is as a *gateway* for fx denom transactions… its fx balance sheet is like the book-keeping of the gatekeeper: a domestic resident may purchase a foreign good/service (=fx outflow) or a foreign resident may purchase a domestic good/service (=fx inflow)

plus there are *loans* & gifts too… a foreign loan or repayment or gift to a domestic resident (=fx inflow), a domestic loan or repayment or gift abroad (=fx outflow).. fx reserves are the *residual* of what’s left on both current and capital accounts taken together! #tellRajan

“fx reserves are the *residual* of what’s left on both current & capital accounts taken together!” #tellRajan

What does Rajan say at 41:43 @PrannoyRoyNDTV @nidhi

#RajanToNDTV ? He says @RBI has “assets” in fx, liabilities in INR… No Dumbo 🐘 RBI has a balance sheet in either!

RBI has a balance sheet in either USD or INR!

Better to have it in USD so neither Manmohan nor Modi start to lust after it… #tellRajan

suppose an Indian techie in Calif *lends* his uncle USD 50,000 to start a factory in Coimbatore… fx reserves ⬆️; next year Uncle repays the loan, fx reserves ⬇️… @RBI s sole function is to convert USD to INR & back! Balance sheet in either!

when Calif sends USD50k as a loan to Coimbatore @rbi fx reserves⬆; when it’s returned ⬇.Initially RBI incurs a *liability* in USD, acquires an *asset* in INR (money to Uncle), both extinguished/reversed when Coimbatore Uncle repays the California techie #tellRajan #RajanToNDTV

a friend is puzzled so I am happy to clarify: Nephew sends a USD loan, he has an asset; @RBI is fx gatekeeper; RBI has a liab w Nephew and an asset in INR paid to Uncle; India’s fx reserves ⬆️; when Uncle repays INR to RBI, RBI repays USD to Nephew; India’s fx reserves ⬇️…

Suppose Calif Nephew forgives the debt, ie transforms loan to Coimbatore Uncle into a gift instead.. India’s fx reserves stay ⬆️.

@RBI holds that amount in USD against which it has issued INR. A different family may have a gift the other way of the same amount, fx reserves ⬇️…

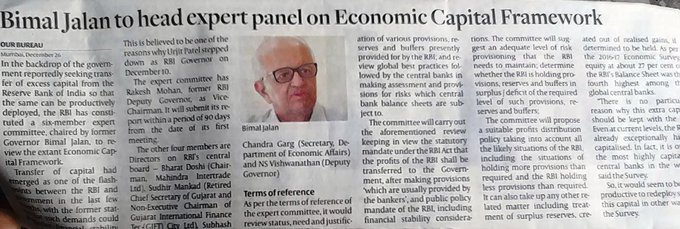

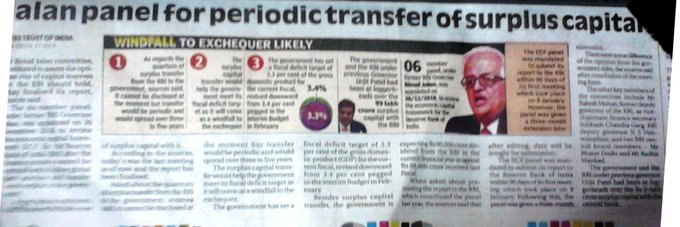

Now has come the appalling idea represented by the so-called Jalan “panel” (it pretends to be of experts but has none, just bureaucrats and a Big Business honcho).

I’ve said it for months and say it again: what the #Jalan “panel” is doing, under pressure from @PMOIndia – following the Manmohan Montek @PChidambaram_IN model of 2007 – is profoundly misguided… https://twitter.com/subyroy/status/1152433290097221633?s=20

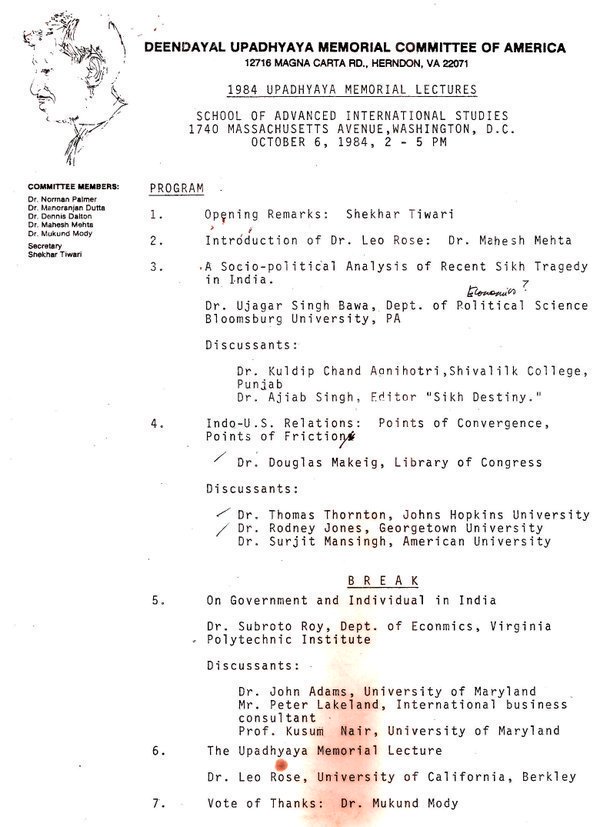

(4) Chapter 4 Mr Modi Goes to Washington Oct 1984

As for Mr Narendra Modi, in October 1984 in Washington DC at SAIS Hopkins, I was invited to give a Deendayal Upadhyaya lecture and did so. From India Mr Narendra Modi led a group of Young Leaders of the RSS for that conference and I recall well him being introduced to me before the talk. I have written about that experience https://twitter.com/subyroy/status/1105722176399908865?s=20

(5) Chapter 5 Rajiv, SS Ray, Milton Friedman & Myself

Mr Modi’s dictat now to somehow get India to some magical “5trilliondollar” economy has seemed to me silly and groundless.

It is similar to Manmohan’s idea of “400 skyscrapers” (or was it 4000?).

Such grandiose notions have behind them some kind of idea of the Government of India somehow getting their hands on “3trillionRupees” worth of foreign exchange reserves, of which the RBI is custodian, and then spending their way on unknown and probably totally wasteful expenditure (eg paying for foreign weapons India does not need but on which payments have come due, as had happened in the 1990/91 bop crisis, Amaresh Bagchi told me in 1992).

(7) Chapter 7 Brunner & Meltzer’s Balance Sheet

What is the best interpretation that can be put to the Modi idea? That was the question I have asked myself,and the problem started to be cracked when I came across Karl Brunner & Allan Meltzer’s Table 9.1 in the Benjamin Friedman & Frank Hahn (eds) Handbook of Monetary Economics Vol 1…

It still takes several steps to apply to India! And I realised Dilliwallas/Bombaywallas will still fail to see the connections or get the logic under their belts. So I have had to explain it all myself … Hence the Roy Model of what RBI & GoI are (unknowingly) up to…

The Brunner Meltzer balance sheet Table 9.1 is where RBI & GoI have to start to comprehend what they are themselves trying to do using the #Jalan “panel”and all those trillions… starting by constructing from there…

Start with what Brunner Meltzer call “Real Capital” held by the Public, K… Without loss of generality let’s include Human Capital too along with Real Capital as K, so Output or National Income or GDP is

Y = f (K) f’>0 which means as K⬆️ Y⬆️…

Now what is it Messrs Modi Shah Gurumurthy etc want to do? They want to go from today’s Y 2019 to some larger future Y 2024 where the latter is valued at “USD5trillion”

Ie Y has to grow by 🔼 Y…

How can Y2019 grow by 🔼 Y to Y2024?

Plainly given Y=f(K) f’>0 only by K growing adequately too,

Ie by some 🔼 K…

So what it is Messrs Modi Shah Gurumurthy etc want to see is growth of Real & Human Capital K….

OK. Fair enough.

Returning to Brunner Meltzer as the basis of explaining to the Bimal Jalan “panel” what it is they are (unknowingly) up to…

It will be seen a P multiplies the K… that is “Price” giving nominal values…

Let’s change that to r for real return on our combination Real & Human Capital…

Now Brunner Meltzer have the Public on one hand, the Central Bank & Government on the other…

the Central Bank has, let’s call it “gold”, Au, as an asset, against which it issues Base Money B…

I am going to say the Central Bank is owned by the Public… so the Au is also owned by the Public…

In an economy without imports exports or other fx flows, the Public as a whole has no Liabilities…

its Assets here are then rK (the nominal value of all Real and Human Capital) + Au = W its total Wealth or Equity,

Ie, the Public’s Wealth is W = rK + Au

Brunner Meltzer also have S for securities or Public Debt issued by the Government to pay for its expenditures… at a rate of return v…

Hence their Table 9.1. has vS held by the Public (usually by Banks) as an Asset against which Government has Liabilities vS…

Ignore that too, so… we have only W=rK+Au…

We’ve reached the end of Stage 1… time to leave Brunner Meltzer ‘s Table 9.1 behind…

For now we have W=rK + Au and the #ModiSarkar2 PMOIndia’s wish to somehow get K to increase by 🔼 K (or rK to increase by r🔼K in nominal terms) to get to Mr Modi’s magical #USD5trillion economy.

The idea — in fact the perpetual temptation — motivating the #Jalan panel under Mr Modi et al now as it did Manmohan Montek Chidambaram is to somehow use Au to cause 🔼K…

This idea, this perpetual temptation, to somehow use Au to cause 🔼K that is motivating #Jalan panel now as it did Manmohan et al earlier may well be fallacious…

tho let’s assume for now it’s not…

Return to W = rK + Au which is the Public’s Wealth..

W = rK + Au showing no liabilities for the Public as a whole is so if there are no foreign exchange flows in either direction.

But obviously there are such flows in fact…

fx inflows from exports and inward remittances and interest received,

fx outflows due to imports and outward remittances and interest paid…

that’s the Current Account.

If fx inflows > fx outflows on the Current Account (and there is no Capital Account) then

W = rK + Au may show 🔼Au > 0

while

if fx inflows < fx outflows on the Current Acc 🔼Au < 0…

let us suppose the latter prevails (as it does in India), call it the CAD or Current Account Deficit.

the CAD has to be matched or “financed by” net positive fx inflows on the Capital Account,

eg by Indian loans abroad (assets tho implying fx outflows)

being lower than

loans to India from abroad (fx inflows tho implying liabilities)… |

Net Capital Inflows have to match or exceed CAD

If Net Capital Inflows > CAD in absolute size, the fx “reserves” held by the RBI will be rising, and vice versa…

Now can you see why I have denounced the whole #Jalan panel idea including the “it belongs to the Govt” fallacy of Dr @IlaPatnaik as well…?

(8) Chapter 8 THERE IS NO EXCESS, NO “WINDFALL”, NO “SURPLUS”! IT’S AN ILLUSION, A MIRAGE! 27.8.2019

“How is that RBI has Excess/Surplus Funds while Other Banks struggle?” @prao_d

“Ques arises, From where RBI get this income?” @idesibanda

My answer: there is no excess, it is an illusion, a mirage… to repeat THERE IS NO EXCESS, IT IS AN ILLUSION, A MIRAGE!

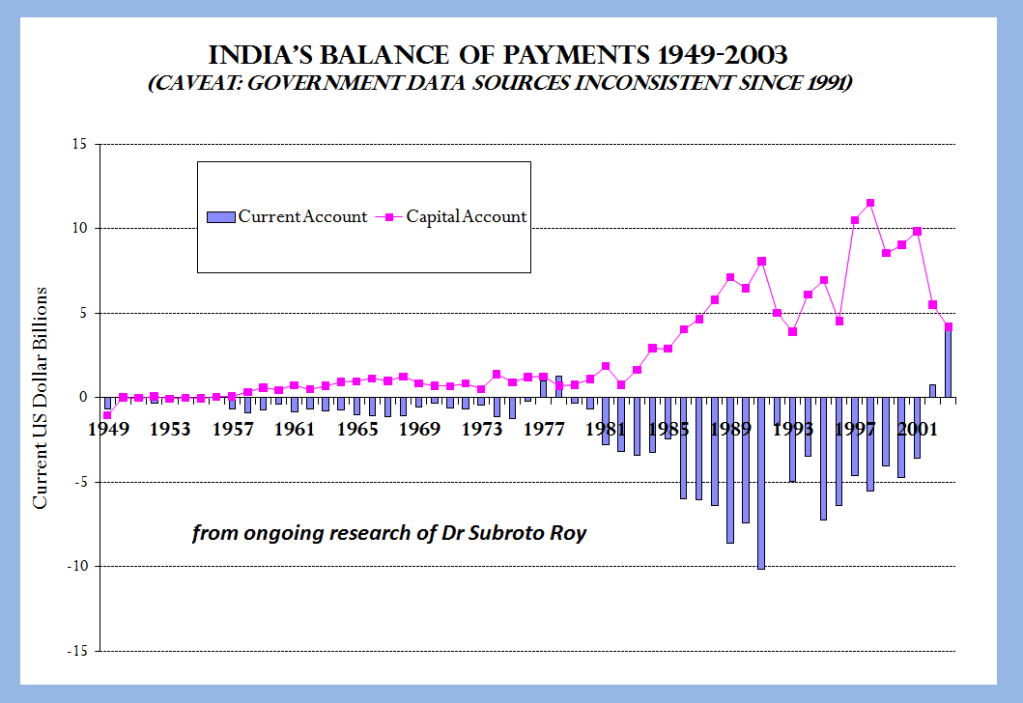

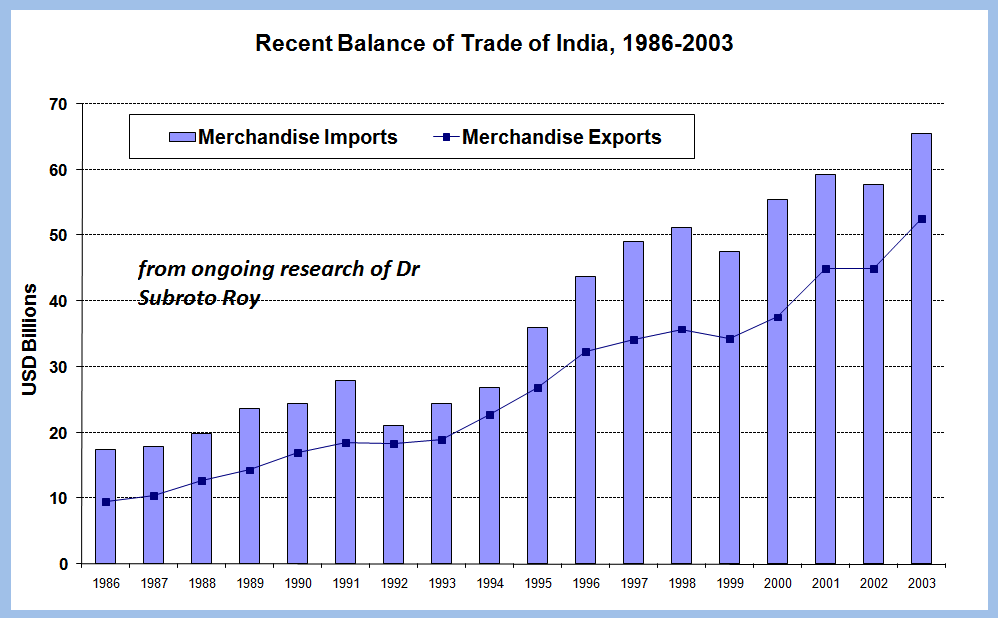

Start with merchandise trade of India… over decades and decades….

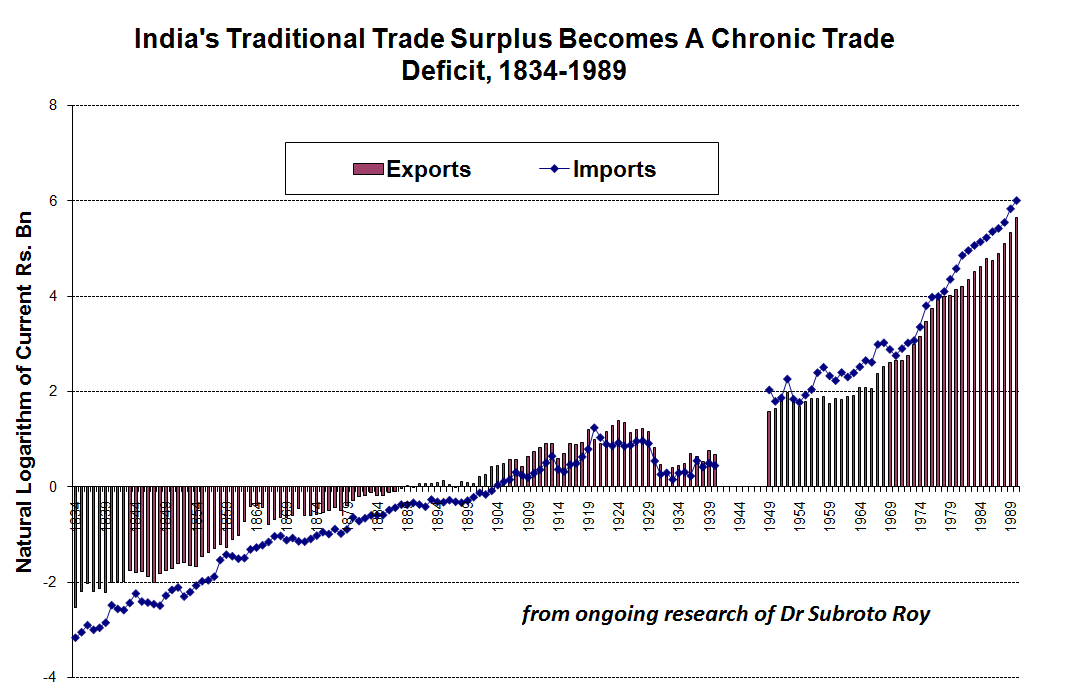

post Independence, India’s traditional surplus of merchandise trade is gone… more merchandise imports than merchandise exports… (balance of trade….)

Government merchandise imports as a percentage of total 1949-1989 (a lot maybe military)… (and the negligible Government merchandise exports as a percentage of total)…

India weapons imports by origin… in constant 1970 USD millions

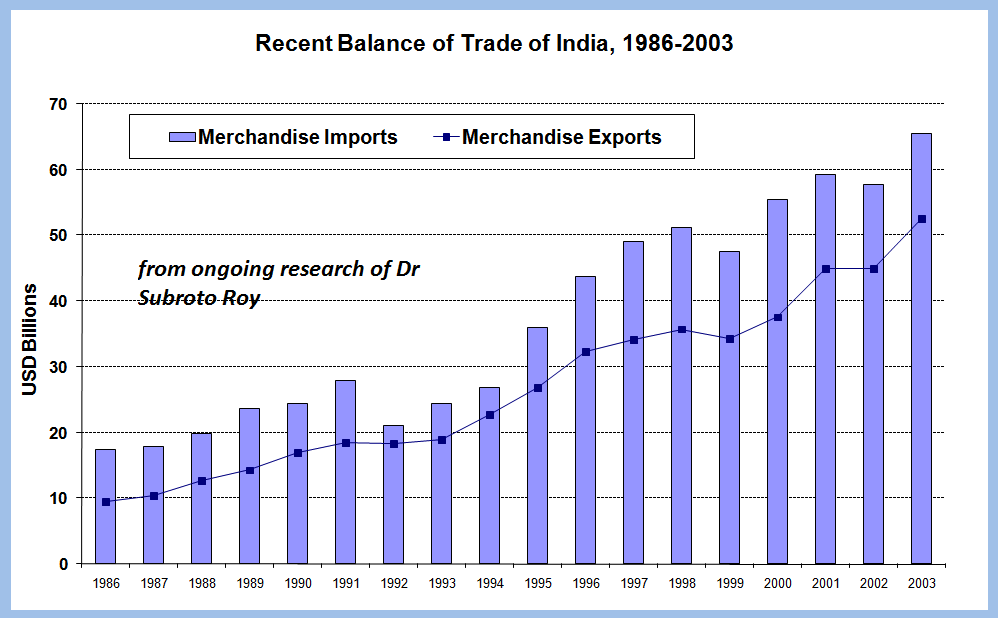

“Recent” India Balance of Merchandise Trade 1986:2003 …. NB still no sign of any “surplus” fx arising sua sponte in @RBI from merchandise trade! (and it likely gets worse 2003 to 2019…)

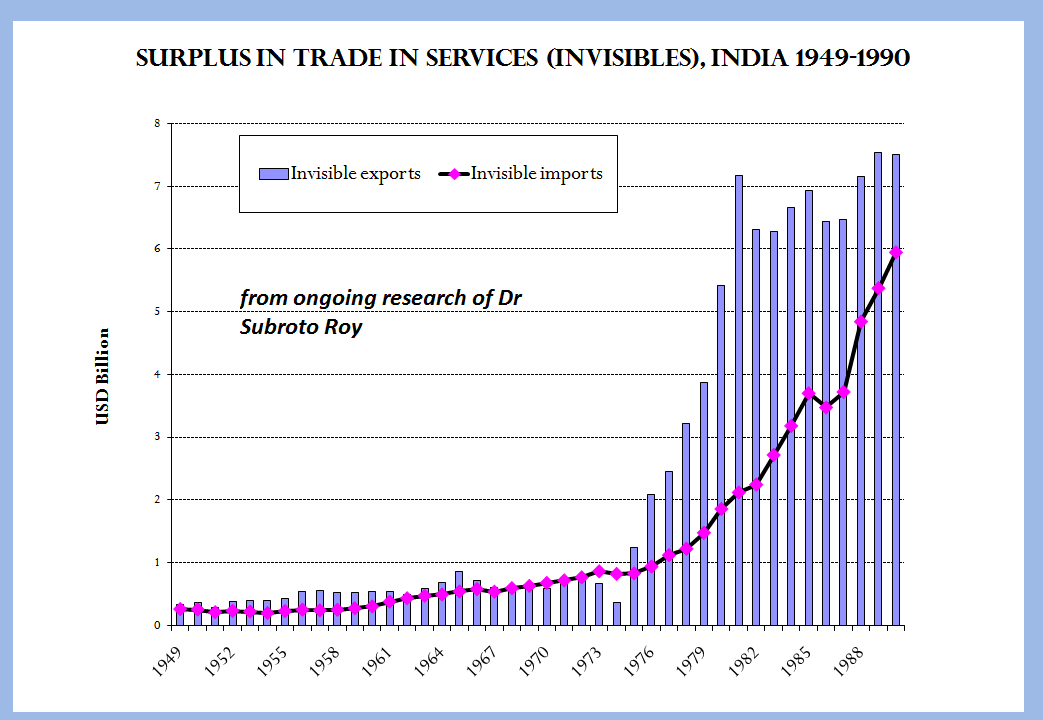

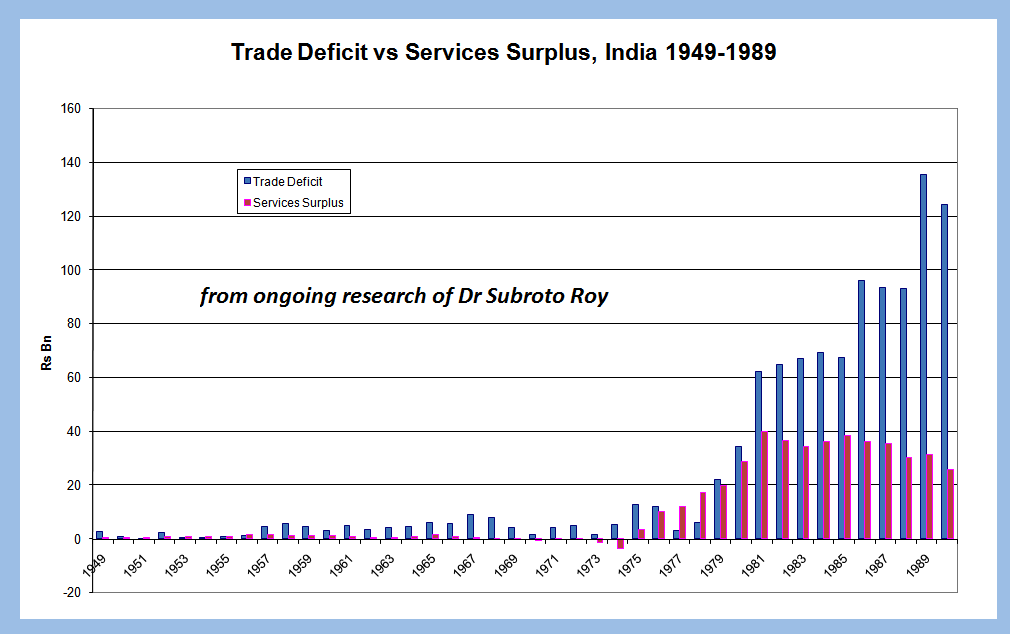

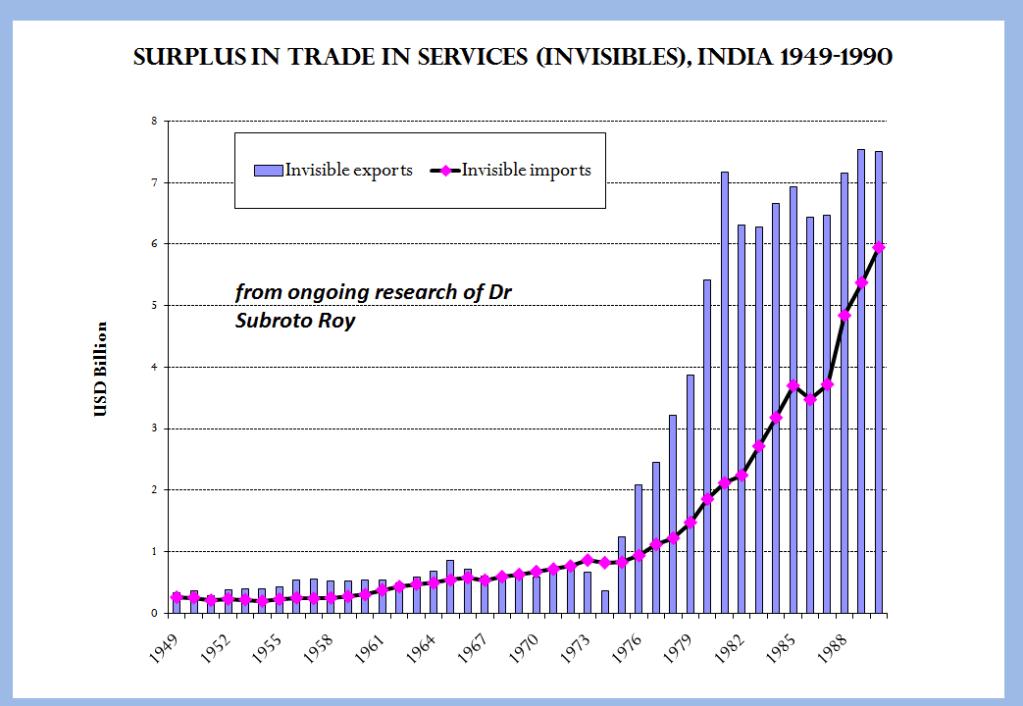

Yes the (little) good news has been a +ve trade balance in “Services” (ie “invisibles”)… labour migration to the Gulf from the late 1970s helped… (tho I expect now elite Indian tourism abroad may have wiped that out… Hey those celebrity weddings abroad cost fx!)

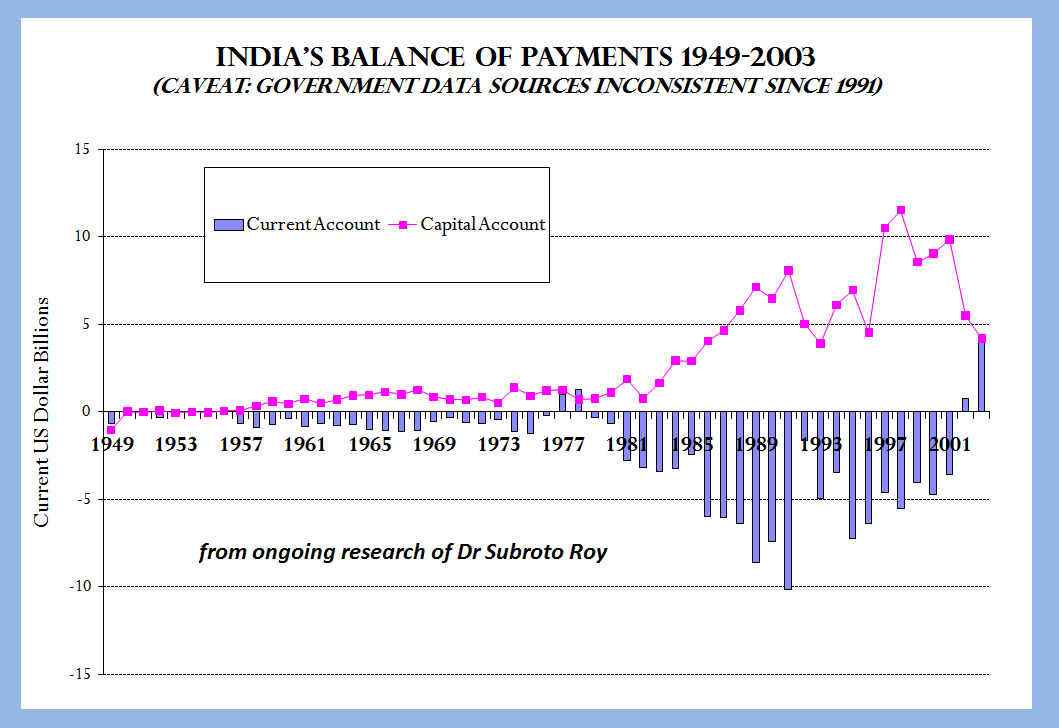

what is the BoP “Current Account”? mostly Balance of Merchandise Trade + on Services… India has a *Deficit* CAD, and it’s systematic, even endemic.. So still no sign of any RBI “surplus” fx!

So where is this @RBI fx “surplus” arising from? IT’S **BORROWED**! Capiche?! #thinkPonzi

What did I say at the start? I said:

“The RBI like any central bank is charged with managing a country’s “foreign exchange reserves”; fx reserves are *not* what they sound like: they are a residual in a country’s balance of payments and are *not* akin to tax revenues, hence are *not* open to be purloined by a Government to spend.”

Manmohan, Montek, Chidambaram et al tried… and got a earful from me in 2007… Now a dozen years later Sitharaman, Gurumurthy, Shaktikanta Das, Rajiv Kumar, Amit Shah, and the PM too deserve the same for their attempt to transfer to GoI mostly borrowed fx…

(9) Chapter 9 India’s Balance of Payments 28.8.2019

India’s Balance of Payments (by the Kindleberger definition):

B =Manufactured (Exports-Imports)

+ Services (Exports-Imports)

+ Private Transfers (remittances)

+ Public Transfers (aid)

+ Net Publicly guaranteed loans (New Disbursements – Amortization of Existing Loans)

+ Private Direct Foreign Investment

+ Net Short Term Capital Flow

Now where e = Errors and Omissions

B + e =

– delta R (Change of Reserves, -ve = increase in level)

+ delta F (Change in Net Liabilities with the IMF)

So for example in 1986 USD mn: B = 337,

delta R = -548

delta F = -264

– delta R + delta F = 284;

so e = -53

Ie 337 – 53 = 284 = -(-548) – 264 = 284

#TellRajan

[I wrote “Mfg (Exports-Imports)” a little hastily… meaning Manufactured goods trade… Traditionally it is “Merchandise exports and imports”… including “raw materials”, agriculture, and “manufactured goods”… But come to think of it, my error seems fine… mining and agriculture are also manufacturing in the theory of production…]

In September 2014 I first said Nirmala Sitharaman should head to the Finance Ministry.

Sep 3, 2014 Memo to @PMOIndia: Sir, given @arunjaitley’s ailments, perhaps he himself wd recommend e.g. @rammadhavbjp as DefMin, @nsitharaman as FinMin

… On 31.5. 2019 I cheered her appointment. Now she has it… Well done @PMOIndia #ModiCabinet #ModiSarkar2

Today 27.8.2019 I can see she’s tried hard to comprehend the dimensions of the job, then either given up or stopped learning believing she knows the questions let aside answers…

Finance Minister @nsitharaman w #RBIReserves #RBILooted is now well & truly out of her depth. It is sad. It is not for want of good intent & effort on her part. She has denounced as “outlandish” criticisms eg by myself (I don’t know any other) of the integrity, autonomy, competence of @RBI.

(10) Chapter 10 RBI’s Monetary Base 28.8.2019

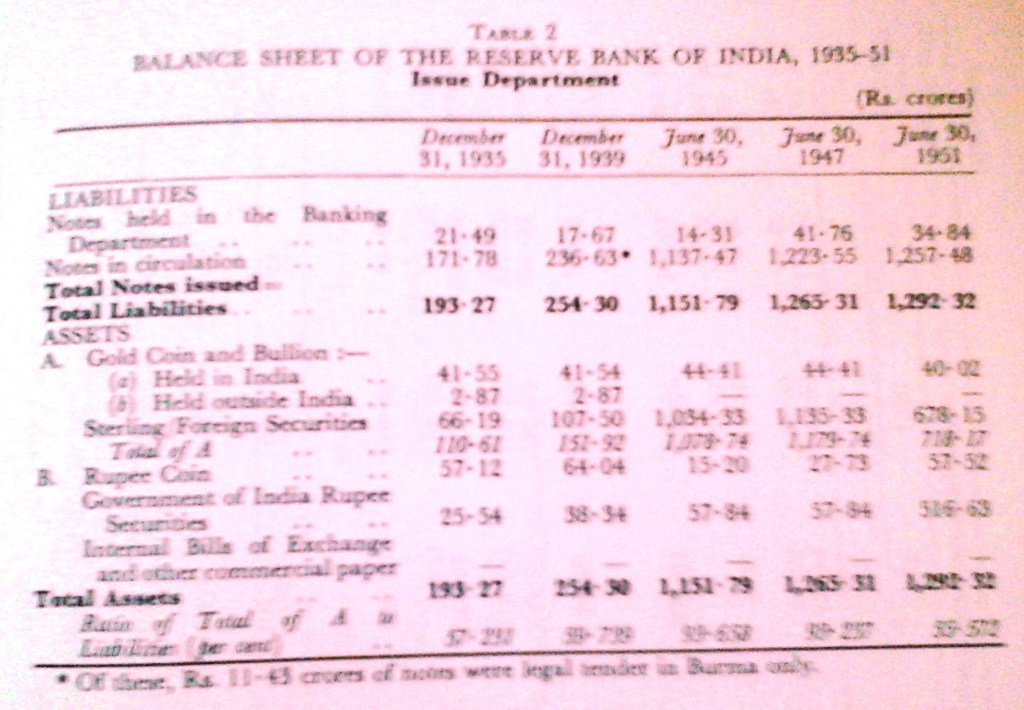

Looking at the original @RBI history (Vol 1 is excellent, the remaining Vols, not so much)… I see there is a monetary interpretation to what Nirmala Sitharaman, Shaktikanta Das, S Gurumurthy, Bimal Jalan et al have been up to…. **Go after “High Powered Money” or the “Monetary Base” (“A” in Issue Dept)**!

What is “A” in the Issue Department (in those old original @RBI balance sheets when the accounting had integrity)? “A” is Gold and Foreign Exchange Securities… That is the same as Au in the Brunner Meltzer table earlier

Now @nsitharaman @dasshaktikanta have their hands on not merely the Money Supply but the Monetary Base itself! “High Powered Money” in the American terminology!

(Neither knows enough to know it…Nor does the #BimalJalan “panel” with or without Rakesh Mohan.)

I said 16.12.16 during #ModiJaitleyChaos #Demonetization

“The risk created needlessly by #QuackEconomics is of a massive contraction followed by massive overshooting”.

First cause contraction, now ruination of the Monetary Base ie High Powered Money!

First you cause Contraction then you cause Inflation…

India’s macroeconomics, India’s monetary and fiscal and balance of payments policy, is effectively out of control… as of late August 2019…

11) Chapter 11 Explaining the Govt’s Mirage 30.8.2019

As of 29 August, it was a mystery to me by what sleight of hand and when did RBI start conflating Base Money and borrowed foreign capital…? Manmohan and friends had wanted to merely “borrow” @rbi fx reserves, then backed off, PM Modi wants to take them and spend them too, so that’s worse!

24 hours later I think it’s solved!

What creates the illusion… the mirage… that @RBIhas a “surplus”/”excess” that, according to Bimal Jalan, can be and is going to be and has started to be transferred to GoI for @PMOIndia to spend?

Every mirage has to be explained!…

I’ve shown that no such “surplus” has arisen in foreign exchange from India’s’ Current Account… It hasn’t come from net export earnings and remittances being positive overall

(Contrast China ! they’ve been making and selling things abroad for mass markets! ).

So I’ve said rudely and bluntly

“So where is this @RBI fx “surplus” arising from? IT’S **BORROWED**! Capiche?! #thinkPonzi“

How the illusion or mirage arises was already implicit in my earlier proof in Dec 2018 of Raghuram Rajan s fallacious statements #RajantoNDTV about India’s reserves…

viz suppose an Indian techie in Calif *lends* his uncle USD 50k to start a factory in Coimbatore… India’s fx reserves rise. Next year Uncle repays the loan, fx reserves fall back. @RBI s sole function has been to convert USD to INR & back, be a gatekeeper! Its balance sheet is in either USD or INR!

Now Nephew sends a USD loan, he has a USD *asset*; @RBI is fx gatekeeper; RBI has a *liability* with Nephew in USD. But RBI in INR has an *asset* (paid to the Uncle)! (Uncle has a liability in INR matching Nephew’s asset in USD with RBI merely having allowed the transaction to occur internationally.)

Suppose there are many lenders like this to Indian borrowers and there is no “crisis in confidence” so no one is demanding repayment except on schedule… RBI assets in INR will zoom up matched exactly by RBI liabilities in USD zooming up!

Now back in 2007 the Sonia Manmohan Chidambaram Montek regime looked at those massively rising INR assets of @RBI (since the equivalent USD liabilities are not being mentioned!) and said “I want some”… promising even to repay it…

What Messrs Modi Jaitley Shah Gurumurthy Sitharaman Das have now done, with a wink and a nod from Bimal Jalan and his “panel”, is demand straight up Gimme Gimme Gimme… Of course for “small business” “poverty alleviation”, “recapitalising PSBs” #RBIReserves

How does the #RBIReserves mirage get exposed/explained? Ask to see how the balance sheet looks, at least in its external aspects, in USD not INR! Obviously the vast zooming up of *assets* denominated in INR are matched by a zooming up of *liabilities* denominated in fx like USD!

Finance Minister @nsitharaman is naturally outraged critics, eg myself, have questioned the @RBIs competence & credibility re the Bimal Jalan panel. I’d have liked to agree with her but can’t. The panel had 0 expertise in the Monetary Econ needed, 0. #RBIMirage

What you’ve done Respected Minister is count #rbireserves swollen by Capital Account borrowing as INR **assets** when they’re equally matched by USD **liabilities**!! Hence #RBIMirage

Where’s the “surplus”? Whence does it arise?

Twitter 17 September 2019

Rutherford said no scientific discovery was worth anything unless it could be explained simply (eg to a barmaid)… my explanation of what’s wrong with #5trillioneconomy#rbireserves#RBI#rbiMirage

Suppose a family has x=12 from earnings and y=305 from borrowings and puts it all in the bank z=317. Can it spend the 317 as freely as it can the 12? That in the plainest language explains the #RBIMirage I have pointed to

The search engine above should locate any article by its title; the Index and Archives may be used as well.

Readers are welcome to quote from my work under the normal “fair use” rule, but please try to quote me by name and indicate the place of original publication in case of work being republished here. I am at Twitter @subyroy, see my latest tweets above