The Dream Team: A Critique

by Subroto Roy

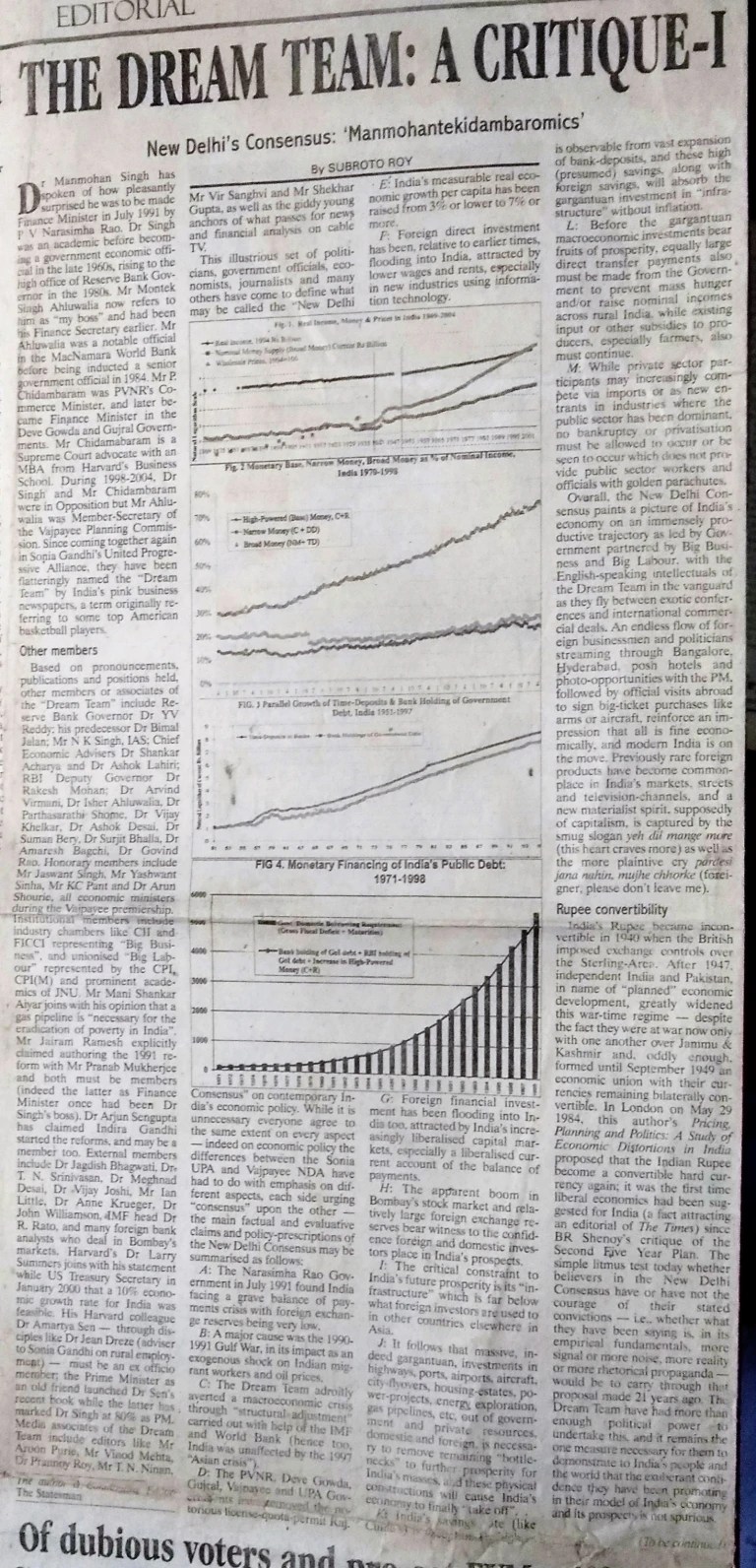

First published in The Statesman and The Sunday Statesman, Editorial Page Special Article, January 6,7,8, 2006

(Author’s Note: Within a few weeks of this article appearing, the Dream Team’s leaders appointed the so-called Tarapore 2 committee to look into convertibility — which ended up recommending what I have since called the “false convertibility” the RBI is presently engaged in. This article may be most profitably read along with other work republished here: “Rajiv Gandhi and the Origins of India’s 1991 Economic Reform”, “Three Memoranda to Rajiv Gandhi”, “”Indian Money & Banking”, “Indian Money & Credit” , “India’s Macroeconomics”, “Fiscal Instability”, “Fallacious Finance”, “India’s Trade and Payments”, “Our Policy Process”, “Against Quackery”, “Indian Inflation”, etc)